A trio of trusts packed with bargains

In a shop sale, we fight for items we don’t even need, argues Kepler’s David Brenchley. So why are investors shunning an area with 50% off and running to the most expensive?

26th June 2026 14:05

This content is provided by Kepler Trust Intelligence, an investment trust focused website for private and professional investors. Kepler Trust Intelligence is a third-party supplier and not part of interactive investor. It is provided for information only and does not constitute a personal recommendation.

Material produced by Kepler Trust Intelligence should be considered a marketing communication, and is not independent research.

We recently bought a pizza oven, as the first item that will eventually make up part of the outdoor kitchen in the garden of our new house. The choice was between Gozney and Ooni, two British brands that are popular worldwide; the research painstaking (for me, at least). Most reviews suggested Ooni’s Karu 12 Pro had the edge performance-wise, but wasn’t quite as aesthetically pleasing.

We decided that while the Gozney was £100 more expensive, we preferred the look, so had agreed that we’d buy it as soon as we got back from our holiday in Italy. While there (where we, surprisingly, ate no pizza at all), I noticed that Ooni was having a sale and suddenly the Gozney had become £300 more expensive. We pivoted and bought the Ooni. The bottom line was that getting 30% off the RRP was too good to pass up.

When shopping, I’d argue that most of us would walk past a shop offering wares at full price when the outlet next door was offering a 30% sale on similar products. Yet, when it comes to the stock market, animal spirits often lure us to the overpriced stock markets and those companies that are on sale are shunned.

On the surface, it makes sense. Take our own domestic, mid-cap stock market as an example. In the five years to 11 June 2026, the Vanguard FTSE 250 ETF GBP Acc (LSE:VMIG) has returned a paltry 17.8%, trailing the US, Japan, Germany and global emerging markets.

It’s only just outperformed the Vanguard LifeStrategy 40% Equity A Acc (B3ZHN96) fund, which has returned 16.1% despite having both a structural overweight to the UK as well as 60% of its assets in bonds at a time when that particular asset class performed historically poorly. In fact, given the FTSE 250’s five-year price return has been just over 1%, most of VMIG’s returns have come from dividends.

When set against its large-cap counterpart, the Vanguard FTSE 100 ETF GBP Acc (LSE:VUKG), performance of the UK mid-cap index is uninspiring, with five-year returns from the blue-chip bourse at c. 72.7% - underperformance of c. 55 percentage points.

Storm clouds have gathered

This isn’t all that surprising, of course. The FTSE 250 is more geared into the UK economy than the FTSE 100 and, as we mentioned in a recent article, the outlook for the UK economy is cloudy.

The UK will, for instance, be one of the hardest hit from the closure of the Strait of Hormuz, which has shut off c. 20% of global oil supply. Renewed political instability has seen gilt yields rise, while the roaring artificial intelligence (AI) trade has stymied returns thanks to our lack of chipmaking capabilities.

Despite all this, there is undoubtedly good news out there that would suggest to us that UK mid-caps should bounce back before too long (how long is anyone’s guess, of course). The economy isn’t in as bad nick as many suspect. The UK’s GDP growth of 0.6% in the first quarter of 2026 was higher than all other G7 nations. Overall growth in 2026 of 0.8% isn’t great, but it remains on par with other major economies such as France, Germany and Japan.

Don’t forget, despite the FTSE 250 being more domestically oriented than the FTSE 100, UK mid-caps still derive more than half of their revenues from abroad, so the UK economy remains only part of the story when it comes to the stock market.

Interestingly, while public market investors seem to have given up on UK plc, private buyers have not. Quite the opposite, in fact. Indeed, even though UK investors have pulled a net c. £74 billion out of UK equity funds, according to the Investment Association (IA), UK firms are being snapped up at an alarming rate.

Should they all complete as planned, the total value of UK takeovers so far in 2026 is £39.3 billion. That’s 33% more than the total value of deals for the whole of 2025, which clocked in at £29 billion. Considering we’re not yet even halfway through the year, that’s impressive. There have been 28 announced deals so far, which is a run-rate of more than one per week.

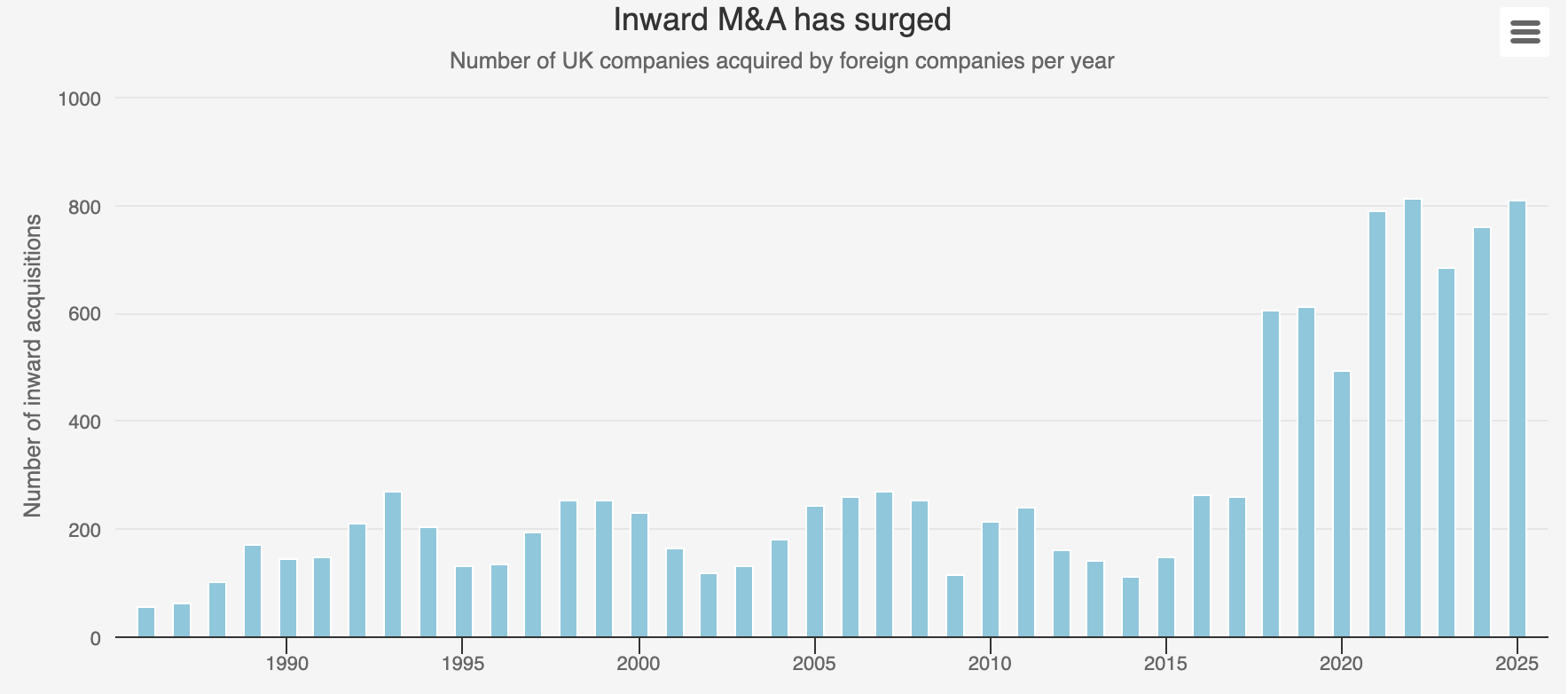

That shows up, too, in deals for all UK companies – not just those listed on the stock market. Between 1986 and 2017, the average number of inward acquisitions (foreign companies acquiring UK companies) was 180 per year; since 2018, that number has risen to 693, according to the Office for National Statistics (ONS). The post-pandemic average is 769.

Coming over here, buying all our companies

Source: Office for National Statistics.

Half-price sale – now on

We think that there are two reasons why foreigners are interested in snapping up UK firms: because we are still the home to world-class, market leading companies, and because they are trading at extremely cheap valuations.

It is the final point that I want to hammer home today. According to Vanguard’s website, on 30 April 2026, the companies held within VMIG (which, don’t forget, includes some investment companies) had an average price-to-earnings (PE) ratio of 10.4x and a price-to-book (PB) ratio of 1.2x. On a PB basis, the FTSE 100 (2.2x PB) was almost twice as expensive as the FTSE 250, while the S&P 500 was almost four and a half times more expensive.

In one investment platform’s analysis of the 22 deals to take UK public stocks private where the terms have been announced publicly, the average premium offered relative to the undisturbed share price is 45%. In simplistic terms, this suggests that there are many UK companies that are, essentially, on a 50% discount.

Normally, when we see a half-price sale, we throw ourselves into the bargain bin and look for the best deals on items we don’t even need. When it comes to the stock market, we seem to be fleeing an area with said 50% off and running flocking to the areas that are most expensive.

Yet, for the reasons discussed, we think this is the worst possible time to be abandoning UK mid (and small) caps. Indeed, it’s possible that we are in the middle of what could be a generational opportunity to build wealth and help turn the tide for UK capital markets.

We would certainly urge shareholders in Schroder UK Mid Cap Ord (LSE:SCP), which recently agreed to propose a tender offer to try to draw a line under a campaign by Saba Capital, to stay the course. It makes complete sense for Saba to tender its shares, but, in our view, for ordinary investors tempted to participate, it would be akin to throwing the baby out with the bathwater.

SCP is well placed to capture what we see as an inevitable re-rating of UK mid-caps. Managers Jean Roche and Andy Brough have constructed a portfolio of c. 50 names focused purely on the FTSE 250, which they believe offers a mixture of leaders from niche or growing industries.

So, too, is Mercantile Ord (LSE:MRC), where managers Guy Anderson and Anthony Lynch invest predominantly in mid-caps, with historically around three quarters of the portfolio in FTSE 250 companies. Guy and Anthony’s bottom-up process focuses on company fundamentals to identify high-quality businesses, generating positive momentum and that are available at attractive valuations.

One option that scours the whole of the market is Fidelity Special Values Ord (LSE:FSV). Managers Alex Wright and Jonathan Winton take an unashamedly contrarian and value-focused approach. Recently, that has seen them take profits from the big tobacco brands, gold miners and defence-related names and recycled into GDP-sensitive stocks such as industrials names, recruitment firms and building materials suppliers, playing into the mid-cap theme somewhat.

Sure, just as the first three pizzas we tried to make with our new Ooni ended up on fire, a calzone and disintegrated in the middle respectively, there are risks to investing in UK mid-caps. Yet, the failure of our pizzas were user error and nothing to do with the oven. Likewise, the cheapness of the FTSE 250 is not the fault of UK plc, but because it’s been shunned by public market investors.

The Ooni was a bargain and as soon as we get used to cooking with it, we’ll be churning out delicious pizzas on a weekly basis. It’s surely only a matter of time, too, before investors see it was a mistake to sell down their UK stocks and start to pivot.

Kepler Partners is a third-party supplier and not part of interactive investor. Neither Kepler Partners or interactive investor will be responsible for any losses that may be incurred as a result of a trading idea.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Important Information

Kepler Partners is not authorised to make recommendations to Retail Clients. This report is based on factual information only, and is solely for information purposes only and any views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment.

This report has been issued by Kepler Partners LLP solely for information purposes only and the views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment. If you are unclear about any of the information on this website or its suitability for you, please contact your financial or tax adviser, or an independent financial or tax adviser before making any investment or financial decisions.

The information provided on this website is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject Kepler Partners LLP to any registration requirement within such jurisdiction or country. Persons who access this information are required to inform themselves and to comply with any such restrictions. In particular, this website is exclusively for non-US Persons. The information in this website is not for distribution to and does not constitute an offer to sell or the solicitation of any offer to buy any securities in the United States of America to or for the benefit of US Persons.

This is a marketing document, should be considered non-independent research and is subject to the rules in COBS 12.3 relating to such research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research.

No representation or warranty, express or implied, is given by any person as to the accuracy or completeness of the information and no responsibility or liability is accepted for the accuracy or sufficiency of any of the information, for any errors, omissions or misstatements, negligent or otherwise. Any views and opinions, whilst given in good faith, are subject to change without notice.

This is not an official confirmation of terms and is not to be taken as advice to take any action in relation to any investment mentioned herein. Any prices or quotations contained herein are indicative only.

Kepler Partners LLP (including its partners, employees and representatives) or a connected person may have positions in or options on the securities detailed in this report, and may buy, sell or offer to purchase or sell such securities from time to time, but will at all times be subject to restrictions imposed by the firm's internal rules. A copy of the firm's conflict of interest policy is available on request.

Past performance is not necessarily a guide to the future. The value of investments can fall as well as rise and you may get back less than you invested when you decide to sell your investments. It is strongly recommended that Independent financial advice should be taken before entering into any financial transaction.

PLEASE SEE ALSO OUR TERMS AND CONDITIONS

Kepler Partners LLP is a limited liability partnership registered in England and Wales at 9/10 Savile Row, London W1S 3PF with registered number OC334771.

Kepler Partners LLP is authorised and regulated by the Financial Conduct Authority.