Transfer your pension to the ii SIPP

Switch and save with the ii SIPP

Lower costs, more control and better support. That's why, each year, thousands of people transfer their pensions to our five-time Which? Recommended Self-Invested Personal Pension (SIPP).

Important information: The ii SIPP is for people who want to make their own decisions when investing for retirement. As investment values can go down as well as up, you may end up with a retirement fund that’s worth less than what you invested. Usually, you won’t be able to withdraw your money until age 55 (57 from 2028). Before transferring your pension, check if you’ll be charged any exit fees and make sure you don't lose any valuable benefits such as guaranteed annuity rates, lower protected pension age or matching employer contributions. If you’re unsure about opening a SIPP or transferring your pension(s), please speak to an authorised financial adviser.

Join the thousands of people switching to the ii SIPP

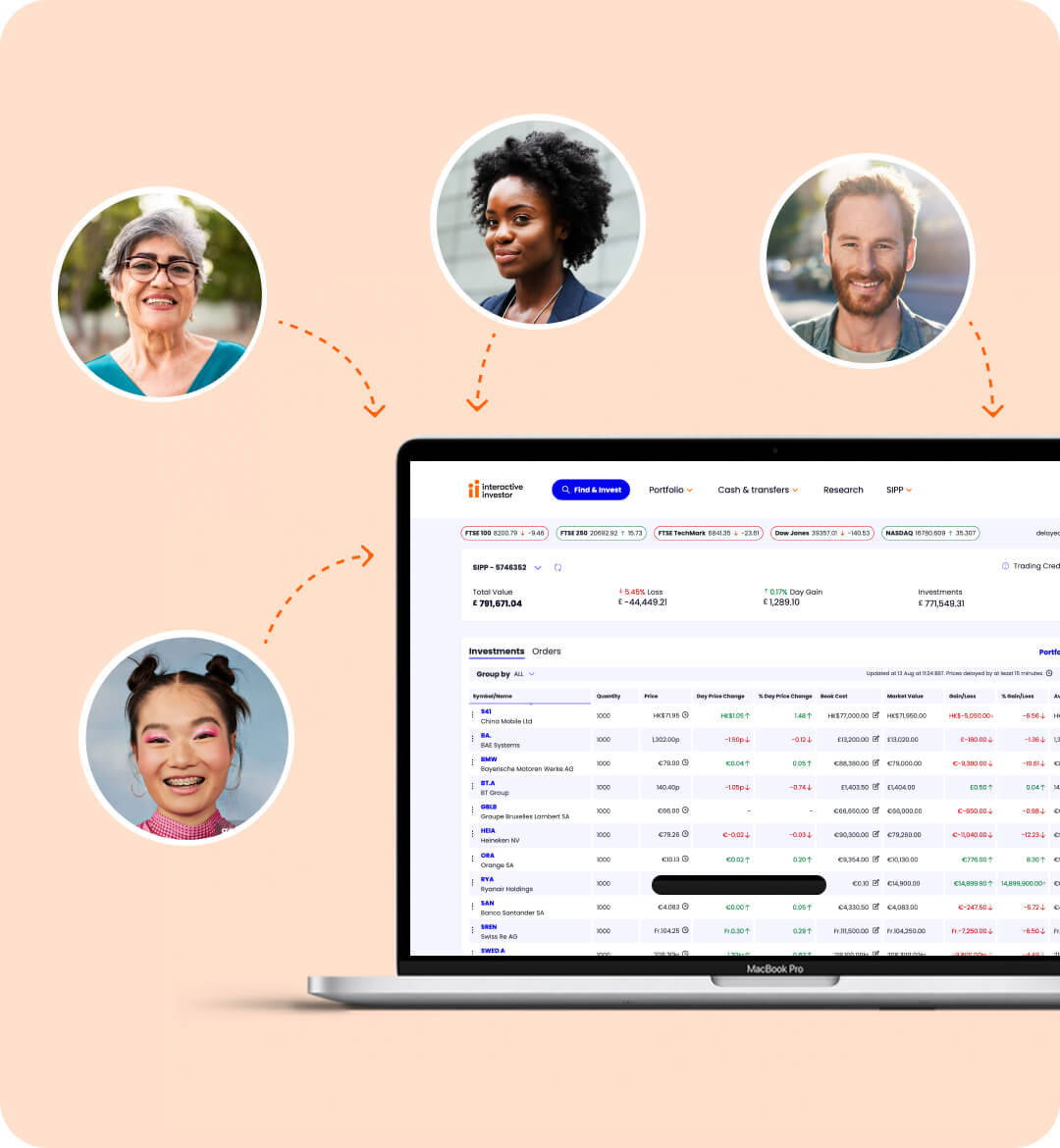

Join over 500,000 ii investors and start taking control of your pension with our award-winning, low-cost SIPP.

We accept all shapes and sizes of UK pension. Many of those transferred to us come from traditional life companies, such as Aviva and Standard Life, and investment platforms like Hargreaves Lansdown.

So whether you’re just starting to build your pension pot or already taking your retirement income, you could save by making the switch to ii.

Keep more of what you make

Other providers usually charge a percentage of your pot. That means you’ll be charged more as your pension grows in value. The ii SIPP is different. With our simple flat fee, from just £5.99 a month, you can keep more of what’s rightfully yours.

Enjoy more choice and flexibility

The ii SIPP offers a wide range of investments and flexible retirement options to suit most people’s needs. More choice doesn’t have to mean more complexity. Let our expert picks and SIPP investment ideas do the legwork for you.

Trust in our top-rated support

It’s easy to keep track of your pension by logging into our website or secure mobile app. But if you ever need some SIPP support, you can count on us. We’re happy to report that ii has more 5-star Trustpilot reviews than any other UK SIPP provider.

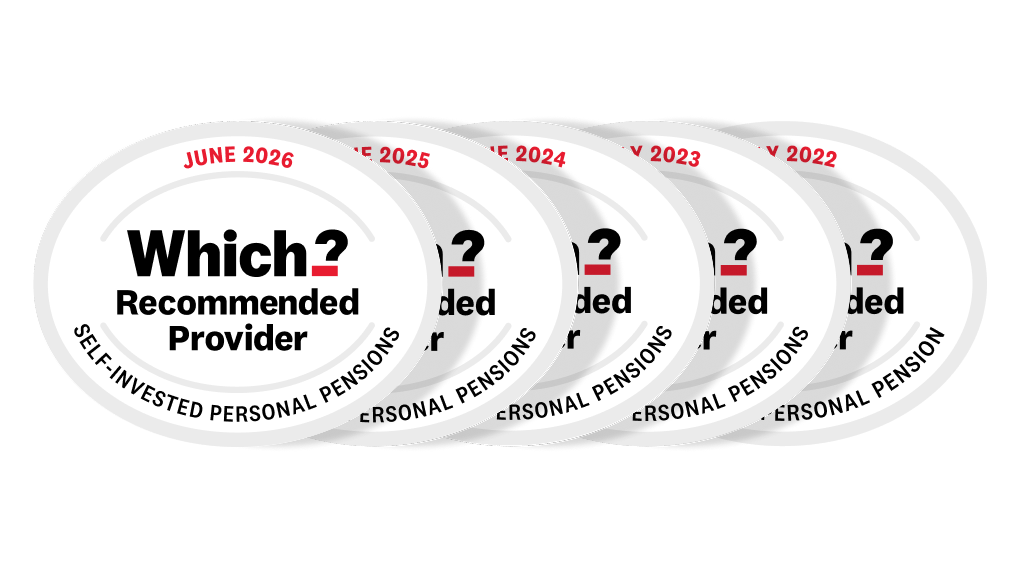

It’s official: five-time Which? Recommended SIPP

For the fifth year in a row, independent analysts at Which? have recognised the ii Self-Invested Personal Pension for its industry-leading choice, support and value.

Join over 500,000 ii investors and start prioritising your pension, with our award-winning, low-cost SIPP.

Open your SIPP to transfer today.

Before you transfer your pension

Transferring a pension to a SIPP can be a great choice for many reasons. It can save you money, improve your investment options and give you greater flexibility at retirement. But there are some important things to check and consider before you make your move.

Check 1: Will it cost you anything to transfer?

It’s always free to transfer with ii from our side. But be sure to check if your current provider charges any exit fees or penalties.

Check 2: Will you lose any benefits if you transfer?

Some pensions have special guarantees and benefits. Before transferring, make sure you won't lose any of the following:

- Guaranteed annuity rates

- Lower protected pension age

- Matching employer contributions

Check 3: Should you take pension advice before transferring?

If you’re unsure about transferring your pension(s), please speak to an authorised financial adviser who specialises in pensions.

How can Pension Wise help?

If you’re thinking about retiring soon and want to understand your options, make sure you speak to someone at Pension Wise.

Pension Wise is part of the government’s Money Helper service, offering free and impartial pension guidance to the over-50s. They can also help you decide if transferring your pension is the right choice for you.

Investing should feel rewarding

Start investing with ii and give your savings more time to grow this summer.

Open an ii Personal Pension (SIPP) and enjoy £200 cashback when you deposit or transfer a minimum of £20,000. See more details on this offer.

Offer ends 31 July 2026. New customers only. Terms and fees apply.

Important information: It’s important to take your time before transferring your pension. Make sure to consider what the best option is for you. Don’t transfer just to qualify for the offer, and don't rush any decision to meet the offer deadline. We periodically run offers, and there will likely be other opportunities in the future.

Before transferring your pension, check if you’ll be charged any exit fees and make sure you don't lose any valuable benefits such as, guaranteed annuity rates, lower protected pension age or matching employer contributions.

How to transfer your pension to the ii SIPP

Once you've decided a transfer is right for you, you can apply online for your ii SIPP and get set up in less than 15 minutes. If you need any support with your application, our team is here to help.

You can start your transfer while opening your SIPP. If you want to transfer later, that works too – just log in via the website.

When completing your transfer request, you’ll need to tell us a few important details, including:

- Your pension provider’s name and your pension account number

- The value of your transfer and whether you’re transferring as cash or investments

- Whether you’ve accessed your pension already (is it in drawdown?)

Depending on what you’re transferring, you may need to send us forms after you’ve submitted your request. If so, the forms will be available on the confirmation page for you to print, complete, sign and return to us.

Once your transfer details are in, it’s time for you to sit back and relax. We’ll work with your current provider to move your pension to ii.

If we need any more information from you, we’ll be in touch. And your case handler will bring you regular updates as the transfer progresses.

Why Bobby transferred his pension to ii

“From onboarding to transferring, all the steps were easier with ii. The transfer process was simple and I now have full control over what I do with my money. That’s why I’m with ii.”

Bobby discovered that ii’s flat fee was better for him in the long run. Hear why he’s joined over 500,000 investors taking greater control of their money with ii.

Have a question about the ii SIPP? We can help.

Call our award-winning UK-based support team on 0345 646 2390.

You can reach one of our friendly SIPP specialists between 8am-4.30pm, Monday to Friday.

Your SIPP investment options

Investment choice is a key benefit of the ii SIPP. Transfer for access to one of the widest ranges of investments on the market, with something for everyone. From our low-cost Quick-start Funds to individual UK and international shares.

Shares

With direct access to the UK, US and several other global markets, you’ll have the world of investing at your fingertips. Search our shares and find tips and ideas to help you build your portfolio.

Funds

Passive, active, income and accumulation - the full spectrum of fund types are here. Explore the range, see our expert picks and learn more about this type of investment.

ETFs

With over 1,000 Exchange Traded-Funds (ETFs) to explore, you can access one of the widest ranges around. Find out more about investing this way and find the ETFs for you.

Investment trusts

Our selection of investment trusts includes many of the most popular and top-traded choices by investors. Get insights from our experts to help you choose the right trusts for your portfolio.

Bonds and gilts

Balance your risk and get regular income, with a wide range of corporate and government bonds from the UK and beyond. Browse our bonds and learn why many choose to include them in their portfolio.

Not sure how to invest in your SIPP?

No worries. Our SIPP Selected Growth Option is an optional low-cost investment that our experts have carefully selected to match common goals when investing for retirement.

SIPP transfer FAQs

You can transfer most types of pension to the ii SIPP, including:

- Personal Pension Plans

- Pensions in drawdown

- Other SIPPs

- Executive Pension Plans

- Defined Benefit Occupational Pension Schemes

- Free Standing Additional Voluntary Contributions (FSAVCs)

- Small Self-Administered Schemes (SASS)

- Stakeholder pension plans

- Occupational Money Purchase Schemes

- Retirement Annuity Plans

If you're not sure whether you can transfer your pension to a SIPP, check with your current provider.

It is usually possible to transfer your workplace pension to the ii SIPP.

If you’re still paying into the workplace pension you want to transfer, you should check that your employer can make contributions to a SIPP instead.

Read our guide on workplace pension transfers.

Yes, you can easily transfer other SIPPs to the ii SIPP.

You have the option to make a full transfer or a partial one, provided your current provider allows partial transfers.

In many cases, you can also transfer existing investments directly to the ii SIPP - so rather than having to sell investments, transfer as cash and then buy them back, we can often transfer your investments directly from your existing SIPP into the ii SIPP. This is known as an ‘in specie’ transfer and you can choose it when you complete your transfer request.

To start, you will need to open an ii SIPP account. You can either start your SIPP transfer while opening an account, or you can do it later by logging in to your online account.

Once the transfer process has started, we will keep you up-to-date with progress.

Yes, as long as your current provider allows it and you haven't yet taken any retirement income, you can usually transfer part of your pension to the ii SIPP.

If you have accessed your pension, and it’s in drawdown, you will only be able to transfer it in full to the ii SIPP.

There are several reasons why you might want to transfer your pension(s) to a SIPP:

- Having one SIPP, instead of multiple pensions in different places, can make it easier to keep track of your retirement savings.

- Our SIPP gives you a much wider investment choice than a typical pension - and we provide free tools and expert insights to help you choose.

- Most pensions charge a percentage of your pot each year, meaning your fees grow over time. Our SIPP charges a flat fee, which could save you thousands in the long run.

On the other hand, there are reasons you might not want to transfer your pension(s):

- If your employer is currently contributing to your workplace pension, you might not want to transfer it until you change employers.

- If you have pensions with safeguarded benefits (such as a final salary pension), you could lose these benefits by transferring to a SIPP.

- If your pension charges high exit fees, you should consider whether it is worth paying these.

If you're not sure whether a SIPP is right for you, we recommend you speak with a suitably qualified financial adviser.

With ii, it’s completely free to transfer your pension. But always remember to check whether you’ll pay any exit fees or penalties to transfer away from your current provider.

Transferring your pension as cash

A pension which is transferred to us entirely as cash usually takes 2 to 6 weeks to complete. You will need to sell any investments before you transfer your pension as cash.

Transferring your pension’s investments

If you are transferring another SIPP to us, you may be able to transfer your investments as they are. Transferring investments typically takes 8 to 12 weeks, depending on the investments.

Not all investments can be transferred to our SIPP. If we offer the investments you hold, you should be able to transfer them.

Transferring a Defined Benefit or SSAS pension

If you’re transferring a Defined Benefit pension or a Small Self-Administered Scheme (SSAS), there are additional steps to complete. This means that the transfer process can take longer than for other types of pensions.

General timings information

All timings depend on how quickly your current provider works with us to arrange your transfer, and whether they use the electronic transfer service, Origo.

During the transfer process, your ii case handler will keep you updated with regular progress emails. If you ever need to contact us about the progress of your transfer, the easiest way to do this is to log in to your account and send us a secure message.

Learn more about transferring to a SIPP

Thinking about a Self-Invested Personal Pension?

Our free Essential Guide to SIPPs has everything you need to know to help you get started. It covers what a SIPP is, how it works and whether it’s right for you.