Are higher rates a red herring for the tech rally?

A Kepler investment trust analyst considers the outlook for investors as we exit the era of the Magnificent Seven.

29th May 2026 14:18

This content is provided by Kepler Trust Intelligence, an investment trust focused website for private and professional investors. Kepler Trust Intelligence is a third-party supplier and not part of interactive investor. It is provided for information only and does not constitute a personal recommendation.

Material produced by Kepler Trust Intelligence should be considered a marketing communication, and is not independent research.

I always found the expression “moving feast” to be a puzzling analogy – what is the significance of eating a meal in different places? Is this one meal being nibbled at, or the same meal being made each time but served in different places? Why would you even bother following the meal around?

It turns out, as no doubt readers already know, that it is not an analogy at all, but a reference to events in the Church calendar that fall on different dates each year, such as Easter. I have to admit that it’s slightly more embarrassing to discover this in middle age than it was to discover the lyrics to the hymn are “the Lord of the dance, said he”, not “the Lord of the darned settee”, as I no longer have the excuse of being eight years old.

Anyway, after a bit of research I am no longer sure it makes sense to describe markets as a “moving feast”, but what I want to find an expression to say is that the drivers of markets are constantly changing, and relying on correlations to continue to work in the same way they have recently is a surefire way to underperform. So it is with the tech industry, the most important in stock markets today.

Technology’s latest surge

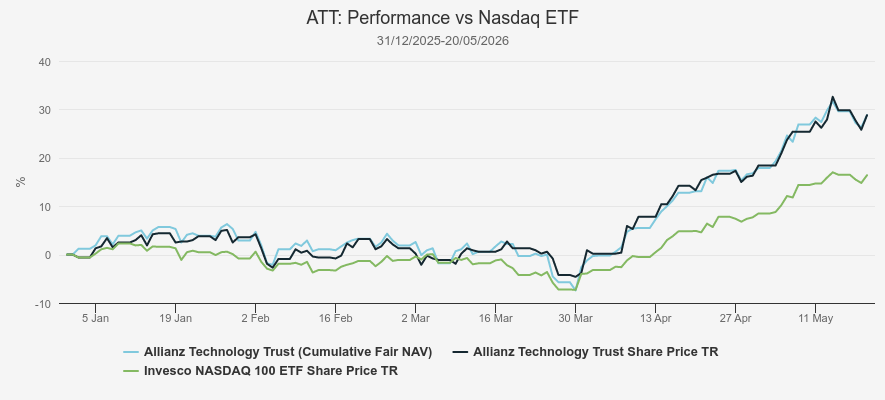

Tech has surged once again this year, with Allianz Technology Trust Ord up 29% in 2026, to 19 May 2026. The dangers in such a meteoric rally were illustrated last week with a one-day drop of 4% on Thursday, since largely recovered. These returns are far ahead of those of the MSCI ACWI/Information Technology Index, which is up 8% over the same period.

YEAR-TO-DATE PERFORMANCE

Source: Morningstar. Past performance is not a reliable indicator of future results

ATT’s manager, Mike Seidenberg, has achieved this outperformance while having about half the index weight in NVIDIA Corp, with Nvidia making a sedate 18% so far, after reporting results last week. This is not last year’s tech market, but unfortunately for the bears, it is still where the action is. ATT’s holdings in memory have helped it generate alpha, while the mid-cap focus has also been highly beneficial. Mid-cap tech stocks have outperformed after years of lagging their large and mega-cap peers.

Last week’s sell-off was reported as a response to rallying US yields, and linked to the US 30-year yield hitting highs since 2007. But this doesn’t make much sense given that US bond yields were already significantly up on the year before the sell-off, and indeed tech did best in March when yields rose too. This was also true of the five and 10-year bond yields which are probably more likely to be used in DCF models than a 30-year bond yield anyway.

I suggest high bond yields reflected a weakening macro environment with a resumption of war on the cards and fears of this sparking inflation and potentially recession. And I think it more likely that is what is responsible for a short, sharp sell-off – a reflexive reaction to a looming negative event of unknown proportion.

Can high rates derail the rally?

High rates do increase the opportunity cost of investing, and they do have an impact on the attractiveness of other return streams. But I think it is missing the point to reduce this to analysts plugging numbers into discount rates (which is just a way to try to mathematically capture the more basic point made above) and I think it is over-simplistic to expect rates to feed through so directly to valuations. In other words, I think investors would be wrong to expect rate hikes, if they come, to stop tech’s rise.

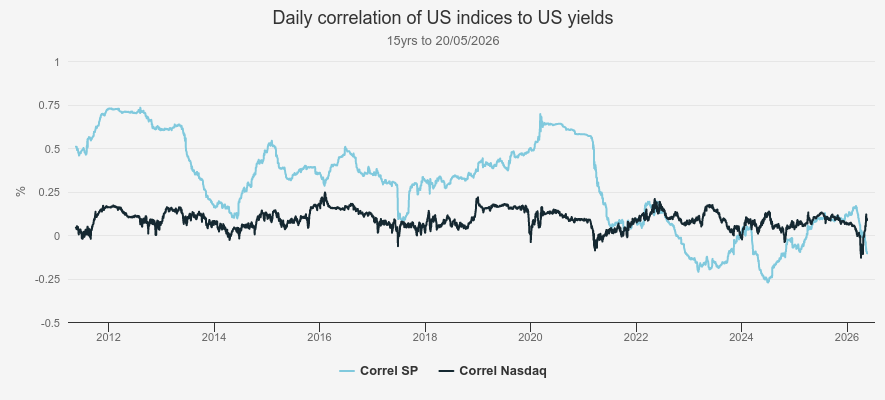

The chart below shows the correlation between US 10-year yields and two US stock indices, the S&P 500 and the Nasdaq, going back over 15 years. If you ever wanted to illustrate the concept of “regime change”, this would do it.

The broader S&P 500 index was positively correlated to rising bond yields for most of the period. When rates were at rock-bottom levels, it was largely a case of higher yields reflecting higher expected GDP growth, meaning investors were more optimistic on the outlook for equities. After the pandemic, this relationship changed as we entered a high interest rate regime, and the S&P 500 has tended to be negatively correlated to bond yields, albeit weakly and inconsistently.

However, the most interesting point for our discussion is that the correlation with the tech-focused Nasdaq Composite hasn’t really changed at all: it has been effectively 0 for the whole 15 years. So tech, the supposed “long duration” industry, doesn’t seem to have been driven by bond yields and therefore rate expectations.

CORRELATION

Source: Bloomberg, Kepler calculations. Past performance is not a reliable indicator of future results

Is this surprising? Well, surely not? Over a 10-year period, Microsoft Corp has compounded EPS by 25% a year, Meta Platforms Inc Class A by 33%, Amazon.com Inc by 48%, and Nvidia by 68%. Plug 68% a year growth into your DCF and tell me how much difference a 25bps boost to the terminal discount rate makes to your valuation.

Sarcasm aside, the maths of compounding at a high rate means that if you could grow EPS by 68% a year for five years, EPS would be 13 times higher than it is today. The valuation of companies that can achieve this sort of growth shouldn’t really be dependent on the rates outlook.

What is going to drive tech in the near future?

Strong earnings from Nvidia last week saw a decent pop in the stock, but a far greater impact on other AI beneficiaries in the hardware space, notably in Asia. Nvidia is now priced for exceptional growth, and the better money has been made in recent months looking for the winners further down the chain. Critically, it is hardware that is seeing the action.

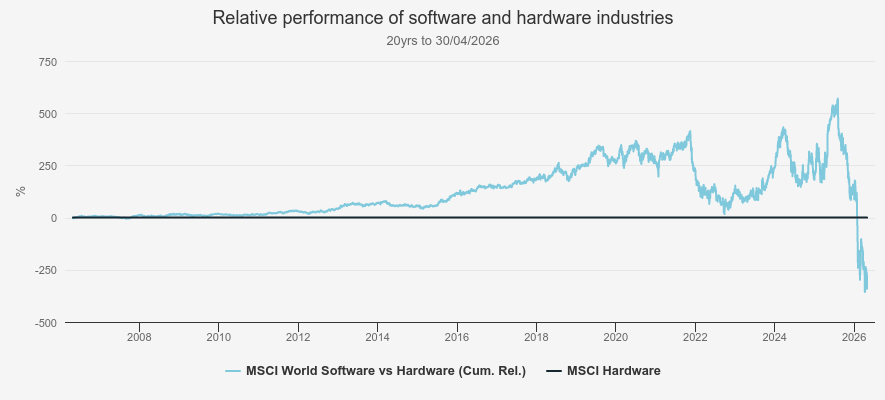

The below chart is truly extraordinary and shows the relative performance of software versus hardware over 20 years. Software had grown capital 15 times compared to hardware’s 10 times as of July 2025, just 10 months ago, but has now underperformed over the whole period.

RELATIVE PERFORMANCE OF SOFTWARE VERSUS HARDWARE

Source: Morningstar, Kepler calculations. Past performance is not a reliable indicator of future results

The basic reason for this is well-rehearsed: AI threatens the business models of many software companies while also massively increasing their need for capital expenditure. It’s not simply the possibility of new AI-driven software, or companies developing their own in-house alternatives, but a change to the economics of the industry, to shorter contracts and to fewer ‘seats’ per company which reduce the stickiness of revenues and the visibility of earnings.

If it is hardware that is going to make the running in the new regime, this must have some implications for market behaviour. In the pre-ChatGPT environment, software and the mega-caps reigned supreme, offering huge cash generation from capital-light business models, with intellectual property the key to their success.

Hardware is a much more capital intensive industry, where having control of the means of production is critical to achieving the revolution: do you have the physical capacity to ramp up production and to invest in the next generation of products? As such, the economic cycle could be much more important for tech in the coming years than it has been, as revenues are likely to be linked to capex cycles rather than perpetual subscriptions or licences for services. This might mean that rates end up being more important than they have been.

If higher rates are implemented to slow an overheating economy, we might see a slowing of investment, and vice versa. But as long as tech companies can continue to deliver absurdly high earnings growth, the impact from rising rates is going to be limited, and as long as the mega-caps gear up their businesses for the new era, and deploy the cash mountains they acquired over the previous decade and a half, there looks likely to be a strong non-cyclical impulse behind AI-related tech.

Conclusion

Those of us who remember the first appearance of Facebook know that its toxicity was obvious from the start, but that didn’t stop Meta from becoming one of the 10 largest companies in the world in about 20 years, with a market cap of over $1.5 trillion. Similarly, the downsides of AI are more than clear already, from seemingly random errors to a destruction of trust in media and images. But that doesn’t mean it isn’t going to revolutionise every single workplace in time. Investors need to vote with their heads, not with their hearts, and the tech story is far from over. Reporters and analysts need to spin short-term narratives, but the rates story is a red herring in my view. The AI rally will only be derailed when companies slow their capex investment, which is more likely to be due to a recession than a few rate hikes.

As we leave the era of Mag7 and latterly Nvidia supremacy, the mid-cap factor and stock selection should become more important, but the opportunity remains. Whether it be in the US mid-cap space, or in the early stage venture space whereMolten Ventures Ordoperates, AI is going to continue to generate huge growth potential for companies with leverage or a niche. Diversification is good, but let’s not get too cool to invest in the obvious driver of earnings growth and cash flow for at least the next decade.

Kepler Partners is a third-party supplier and not part of interactive investor. Neither Kepler Partners or interactive investor will be responsible for any losses that may be incurred as a result of a trading idea.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Important Information

Kepler Partners is not authorised to make recommendations to Retail Clients. This report is based on factual information only, and is solely for information purposes only and any views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment.

This report has been issued by Kepler Partners LLP solely for information purposes only and the views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment. If you are unclear about any of the information on this website or its suitability for you, please contact your financial or tax adviser, or an independent financial or tax adviser before making any investment or financial decisions.

The information provided on this website is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject Kepler Partners LLP to any registration requirement within such jurisdiction or country. Persons who access this information are required to inform themselves and to comply with any such restrictions. In particular, this website is exclusively for non-US Persons. The information in this website is not for distribution to and does not constitute an offer to sell or the solicitation of any offer to buy any securities in the United States of America to or for the benefit of US Persons.

This is a marketing document, should be considered non-independent research and is subject to the rules in COBS 12.3 relating to such research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research.

No representation or warranty, express or implied, is given by any person as to the accuracy or completeness of the information and no responsibility or liability is accepted for the accuracy or sufficiency of any of the information, for any errors, omissions or misstatements, negligent or otherwise. Any views and opinions, whilst given in good faith, are subject to change without notice.

This is not an official confirmation of terms and is not to be taken as advice to take any action in relation to any investment mentioned herein. Any prices or quotations contained herein are indicative only.

Kepler Partners LLP (including its partners, employees and representatives) or a connected person may have positions in or options on the securities detailed in this report, and may buy, sell or offer to purchase or sell such securities from time to time, but will at all times be subject to restrictions imposed by the firm's internal rules. A copy of the firm's conflict of interest policy is available on request.

Past performance is not necessarily a guide to the future. The value of investments can fall as well as rise and you may get back less than you invested when you decide to sell your investments. It is strongly recommended that Independent financial advice should be taken before entering into any financial transaction.

PLEASE SEE ALSO OUR TERMS AND CONDITIONS

Kepler Partners LLP is a limited liability partnership registered in England and Wales at 9/10 Savile Row, London W1S 3PF with registered number OC334771.

Kepler Partners LLP is authorised and regulated by the Financial Conduct Authority.