How retirees can manage inflation and interest rate uncertainty

Making wise decisions with your retirement savings can be trickier when the outlook is murky.

18th June 2026 14:03

by Craig Rickman from interactive investor

Investors have received encouraging news this week on several fronts.

A peace deal has reportedly been agreed between the US and Iran and is set to be signed tomorrow; UK inflation confounded expectations to remain at 2.8% in May when most experts predicted prices to rise; and the Bank of England kept interest rates on hold, providing some light relief for borrowers with a hike deemed a possibility, albeit a slim one.

- Our Services: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

The Bank’s decision today, and the vote split, was largely as anticipated. The nine-person strong Monetary Policy Committee (MPC) voted by a majority of 7 to 2 to maintain the Bank Rate at 3.75% for the fourth meeting on the bounce. The dissenters preferred a 0.25 percentage point increase to 4%.

Inflation outlook improves

As the MPC flagged in its meeting notes, the inflation outlook has improved since its previous meeting on 30 April, reflecting both lower energy and non-energy prices. “CPI (consumer prices index) inflation was now expected to be a little under 3% in Q3 and pick up to a little over 3.25% in Q4,” it said.

Other developments this morning, specifically the jobs’ market, paint a more mixed picture. UK unemployment was expected to stay at 5% but eased to 4.9%, while job vacancies dropped to 707,000 between March and May, its lowest level in five years.

This means that while there are renewed reasons to be hopeful, plenty of uncertainty persists. The MPC takes all this data into account, as well as economic growth, when making rate decisions. The two MPC members favouring higher interest rates are wary about second round inflationary effects triggered by the Iran war, but tightening fiscal policy could also stifle the UK economic fortunes.

- How to build a World Cup-winning portfolio

- Top 10 funds for SIPP accumulation and drawdown pension savers

- How the experts would invest a SIPP at every life stage

While May’s inflation data was favourable, there were some things to take note of. The jump in 12-month services inflation from 3.2% to 3.7% in May shouldn’t be overlooked, according to George Lagarias, chief economist at Forvis Mazars.“This sort of inflation, while still attributed to transport costs, can be stickier and it could require effort to bring down,” he said.

As has been starkly illustrated over the past half a decade, the trajectory of inflation and interest rates really does matter for investors, especially those who have left the workforce and are living off their accumulated wealth.

Why retirees need to manage price rises

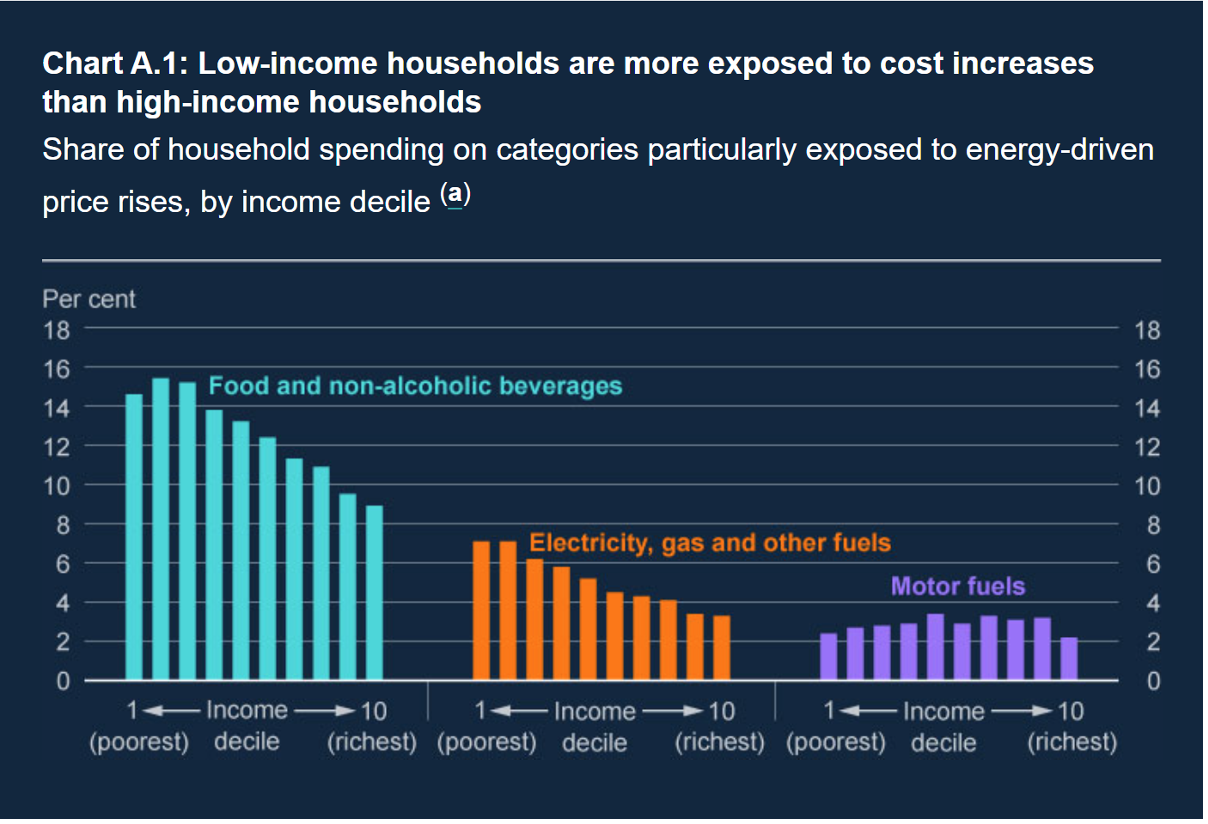

The graphic below is another from the Bank of England’s Monetary Report – April 2026. It reminds us that rising inflation is not felt equally across all sections of society. Lower-income households are more exposed than those with larger incomes, particularly in essential costs such as food and utility bills; when these costs go up it eats up a bigger percentage of the money coming in.

This is relevant right now with the energy price cap rising next month. Given gas and electricity bills are tamer during the summer months as there’s less need to heat our homes, a tight pinch could arrive later this year when colder temperatures draw in.

Investors in retirement face their own set of challenges when tackling inflation. If you’ve stopped worked completely, your ability to generate additional income might be little to none. The investments, savings and other assets that you’ve accrued, must sustain you.

People who’ve traded some or all their pension savings to buy an annuity – a guaranteed income for life or a set period – can be vulnerable to rising prices. Unless you chose an escalating income at outset, inflation will chip into its buying power over time.

But Financial Conduct Authority (FCA) data from last year showed that that only 19% of annuities bought in 2024-25 had escalating payments, and that was high compared to previous years. In the 2019-20 tax year, the figure was only 13%, with incomes from the 87% heavily eroded over the past six or seven years; a period where inflation hit double digits at one point.

The alternative option for investors seeking to generate income from their pensions is drawdown.

This is the more flexible but riskier approach. Your money remains invested, with outcomes based on portfolio performance and withdrawals size. Prolonged periods of sticky inflation mean you may have to jack up income to maintain your existing lifestyle, putting more pressure on your underlying investments.

- New state pension proposal highlights challenges for younger workers

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

- Tony Blair Institute’s radical proposal to overhaul state pension

That said, the flexibility with drawdown means there more options to counteract price rises as they evolve. There’s no guarantee that stock markets will outpace inflation over long periods, but history tells us they do.

In addition, drawdown allows you to keep your option on the table. If at some point guaranteed income becomes a suitable and attractive proposition, you have the option to turn your drawdown pot into an annuity.

There is one pillar of the retirement income framework that can actually benefit from higher inflation: the state pension. Under the triple lock mechanism, the annual amount uprates annually by the higher of average earnings, 2.5%, and inflation. And it’s the 12-month figure to September that’s taken into account, so if CPI does indeed rise over the summer, pensioners could be set for a more generous increase next April.

We should note that wages are still rising faster than inflation, and the deciding period for that metric is the three months from May to July.

Three steps to navigate inflation and interest rates in retirement

Protecting your retirement wealth from inflation and taking stock of interest rate expectations and movements.

1) Monitor your cash holdings

The returns you get on any cash and cash-like investments tend to rise and fall with interest rate movements and expectations. Savings deals have ticked up recently in response to markets pricing in rate hikes but may ease again over the coming months with the odds shortening.

While other assets in your portfolio have better growth potential, cash plays an important role, helping to support any emergencies and meet short-term expenditure. It can also act as a buffer to avoid selling more units of shares when markets slump, which can harm how long your portfolio lasts.

It’s still, however, important to get the best return on your savings, to protect that part of your portfolio from inflation. You should also review your holdings regularly to make sure you’re holding a suitable amount. Too much can cause cash drag, and too little can force you to sell other assets during a period which may or may be favourable.

2) Keep investing for growth

The temptation to hunker down and opt for caution can be strong when uncertainty rises. Stock markets rose off the back of the reported peace deal, but pessimism about the future trajectory of stocks continues to linger.

Ups and downs are very much par for the course when investing, but that doesn’t necessarily make the rocky periods any easier to bear. The difficult thing is there’s no way sure-fire way to chart which way stocks will move. And trying to time the market can work against you, potentially causing you to miss out on any upswing.

With most people opting to keep least some of their pension invested in retirement, leaving growth on the table is essential. A bucket strategy can be helpful and prudent. For example, stashing the next few years’ spending in more secure assets, like cash or bonds, while keeping future income in the stock market, increasing risk for longer periods, giving you time to ride out any bumps should they emerge.

3) Weigh up and review your retirement income options

When it comes to income drawdown versus annuities, the decision isn’t binary; you can pick a bit of both. But even once you’ve decided your optimal blend of flexible and guaranteed income, there are still big decisions to make, especially right now given the cloudy future of interest rates and inflation.

- Tax burden on pensioners surges: how to cut your bill

- Eight vital things to know about passing on income drawdown

With any drawdown pot, it’s sensible to review income withdrawals frequently. At least once a year is a good marker, plus in response to changes in circumstance and sharp shifts in economic conditions, such as changes to inflation and interest rates.

With annuities, the rates attached are sensitive to interest rate movements and expectations. The benchmark are typically 15-year gilt yields, which have risen sharply in recent years with rates following suit.

If you’re thinking about an escalating annuity to protect your income from inflation, there’s something to bear in mind. The starting rates are much lower; you might have to survive a couple of decades to breakeven, so life expectancy is important.

There’s no universal right answer when choosing between a level or guaranteed annuity. Some may prefer consistent payments to support higher spending in early retirement years, whereas others will be happy to take an initial hit to help protect the income’s real value.

We should note there are other options to weigh up here. Others include guaranteed periods, joint life options, and if you’re nervous about committing indefinitely (the terms you choose at outset are fixed), annuities are available for set terms.

The message is think carefully before taking the guaranteed income plunge, making sure you shop around. And it’s crucial to disclose your health, lifestyle and any medical conditions, as this could deliver a notable boost to the income providers will offer, a powerful tool to combat rising costs.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.