Top 10 funds for SIPP accumulation and drawdown pension savers

Our data reveals how Britain’s pension savers are adapting their strategies across different life stages.

27th April 2026 10:26

interactive investor,the UK’s leading flat-fee investment platform, today reveals new data showing how pension investors are adapting their strategies across different life stages, showcasing why choice in a Self-Invested Personal Pension (SIPP) is increasingly central to long-term retirement confidence.

- Funds are the most held instrument type, representing almost 40% of all holdings among SIPP customers on interactive investor*

- Pension savers are using funds strategically, depending on their stage of life: those in accumulation demonstrate more appetite for risk as they look to grow their money over a longer time frame, favouring global equity index funds. However, those in drawdown are focusing on income generation and capital preservation.

Camilla Esmund, senior manager, interactive investor, says: “Our data reflects one of the most fundamental truths in retirement planning: pension investing is not a single decision, especially as we move through different stages of life. Our Great British Retirement Survey shows people are working for longer, are uncertain about when they can afford to retire, and facing increasingly complex decisions about how to fund later life. This is not the time to compromise on your pension. When choosing a Self-Invested Personal Pension (SIPP), the headline fee only tells part of the story. Investment choice is important, whether you’re accumulating in your mid 30s-40s and can take on more risk, or whether you’re nearer retirement. Your SIPP needs to be able to keep up and offer you what you need at each stage.”

- Invest with ii: Open a SIPP | Best SIPP Investments | SIPP Cashback Offers

Kyle Caldwell,funds and investment education editor at interactive investor, explains: “How investors choose to invest is a personal choice and as a firm we are agnostic over how investors build portfolios. Ultimately, though, choice is best served when you facilitate it by offering the full suite of available options: funds, investment trusts, ETFs (exchange-traded funds), equities and gilts.”

Top 10 funds for SIPP accumulation customers (by total value)

Top 10 funds for SIPP drawdown customers (by total value)

Choice helps to diversify – a key pillar of long-term investing

Kyle Caldwell adds: “When it comes to the world of investing, there are some golden rules that can greatly increase the chances of investment success, with one of the key ones being diversification.

“The benefits of diversification, spreading your investments far and wide, is achieved through investing in a range of different investment types and avoiding being overexposed to one country, sector, investment style, or theme.

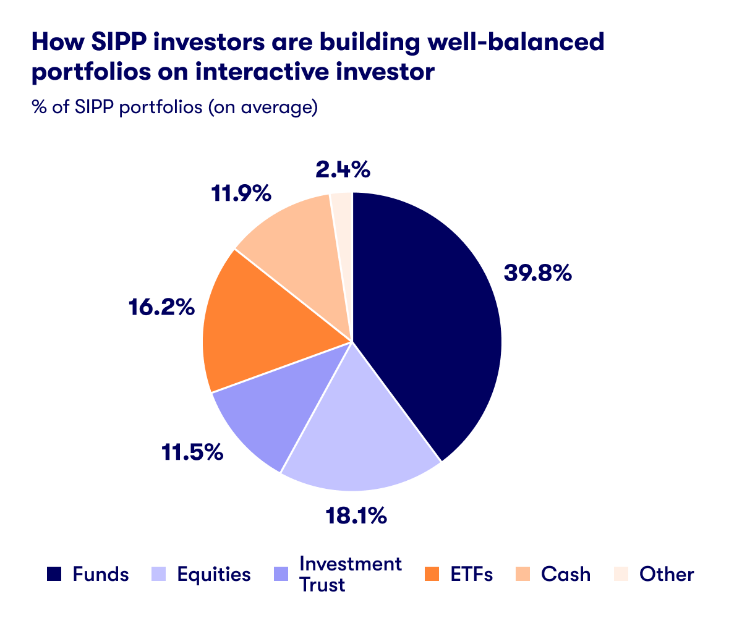

“In order to achieve diversification, we see plenty of evidence of customers mixing and matching, with funds accounting for 39.8% of SIPPs, followed by 18.1% for equities, 16.2% for ETFs, and 11.5% for investment trusts.”

Pension saving across different life stages

Caldwell adds: “When looking under the bonnet, we see that customers at different life stages take different approaches. Those near the start of their investment journey have a greater propensity to own ETFs, with those that offer exposure to the return of the global stock market particularly popular.

“But at the mid-point to latter stages of building pension wealth, the net is cast wider with funds and investment trusts featuring more prominently, with income-producing strategies among those being favoured. Such funds, while still subject to market gyrations, can help to provide a growing income stream, which can help to reduce risk both ahead of and during retirement.

“However, it is prudent to avoid betting the house on income strategies. Given that average life expectancies are in the mid-80s, a pension portfolio also needs exposure to growth-producing assets to strike an appropriate balance.

“Irrespective of where you are on your investment journey it is prudent to consider all the options available. While some people may prefer to go down one route, in having a full menu to choose from, investors can adapt their strategies accordingly and most importantly can make an informed choice in having all fund types available to them.”

*All data to 31 March 2026.

Important information – SIPPs are aimed at people happy to make their own investment decisions. Investment value can go up or down and you could get back less than you invest. You can normally only access the money from age 55 (57 from 2028). We recommend seeking advice from a suitably qualified financial adviser before making any decisions. Pension and tax rules depend on your circumstances and may change in future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.