Is the state pension triple lock on borrowed time?

As fresh forecasts show the cost of the state pension will continue to spiral in the absence of reform, the prime minister-elect is being urged to break a key manifesto promise.

9th July 2026 13:44

by Craig Rickman from interactive investor

Andy Burnham hasn’t even got the keys to 10 Downing Street but is already under pressure to address a divisive mechanism within the state pension framework: the triple lock.

According to the Office for Budget Responsibility’s (OBR) latest Fiscal Risks and Sustainability report – its assessment of current pressures on the public finances - state pension spending is expected to soar from 5% of GDP to around 9% by 2075-76. The OBR cites an ageing population and, notably, the cost of the triple lock mechanism as key drivers, with the latter “estimated to account for around a third of this rise by the end of the projection period”.

It added that keeping the policy will cost around £15.5 billion more by the end of the decade compared to linking the state pension to earnings alone.

- Invest with ii: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

Focus and debate on the triple lock’s sustainability is far from a novel theme. Launched by the Conservative and Liberal Democrat Coalition government in 2011, the policy increases the state pension annually by the highest of inflation, average wage growth and 2.5%. This generous uprating system has been the subject of intense scrutiny for more than a decade, with calls from various quarters to either scrap the policy or water it down.

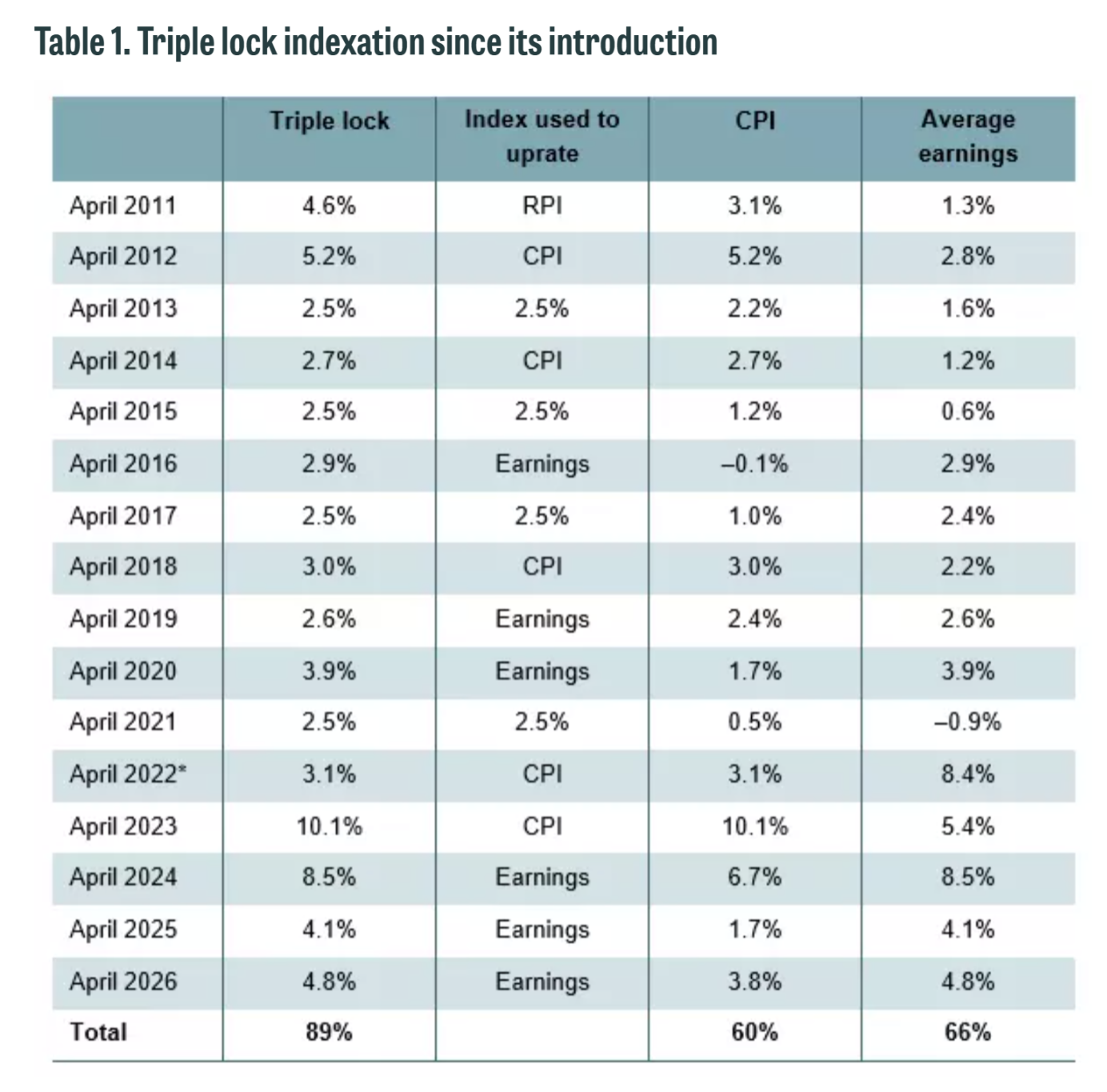

Between April 2011 and April 2026, the triple lock shunted the state pension 89% higher. If it had been anchored to the consumer prices index (CPI) or average earnings, the increases would have been 60% and 66%, respectively. This is essentially what the policy was designed to achieve: capture the best outcome for pensioners every year based on the three metrics. Striking increases can be seen over the past four years, as red-hot inflation during the cost-of-living crisis was followed by wages playing catch up to protect consumer finances.

Source: Institute for Fiscal Studies.

Think tanks have been particularly vocal on the matter. The Institute for Fiscal Studies (IFS) argued last year that the triple lock increases “the value of the state pension in an unpredictable way and it could reasonably be expected to push up state pension spending by anywhere between £5 billion and £40 billion a year in 2050 in today’s terms.”

Meanwhile, in a new report, Intergenerational Foundation (IF) calculates that in 2025–26 the state pension is projected to cost £146 billion, a sharp rise from the £86 billion figure from 20 years ago. “Over this period, the cost of the state pension has increased by almost 70% in real terms,” the IF said.

Even before the OBR’s new data and forecasts emerged, Burnham, the Makerfield MP, was quizzed about his plans for the triple lock should his bid to lead the country prove successful, which now seems inevitable after Al Carns ruled out a leadership bid.

Burham offered assurance to those in favour of the policy, replying that while he recognises the discourse on the topic, “it is important that the commitment in the manifesto stands”. Pledging to retain the triple lock for the current parliament was a key pillar of Labour’s election campaign back in 2024.

Short-term future looks secure

This means the triple lock should be safe for the rest of the decade – good news for those already receiving the state pension or who are edging towards this milestone, which is in the process of rising from 66 to 67 between now and April 2028.

The longer-term outlook offers less clarity. Concerns over the cost of operating the mechanism aren’t going to abate any time soon.Critics have warned the ratcheting effect places unfair onus on younger people, given today’s state pensions are paid by today’s workers.

Interestingly, Labour’s major rivals aren’t attacking its commitment to the triple lock. Quite the contrary. Various political parties are united on the issue, acutely aware of the damage that a shake-up could prompt on their election aspirations given the significance of the grey vote.

Conservative leader Kemi Badenoch was once reportedly in favour of reforming the policy but has pivoted her stance, committing to its future last year. “We created the triple lock; we’ve always protected it and we stand by it,” she said.

Elsewhere, Reform claimed earlier this year that cutting billions from the welfare bill would enable the policy to be maintained, while the Liberal Democrats have also vowed to keep it, taking aim at those who want reform.

Politicians and political parties can and do change tack, of course, but an about-face occurring between now and the next election seems highly improbable.

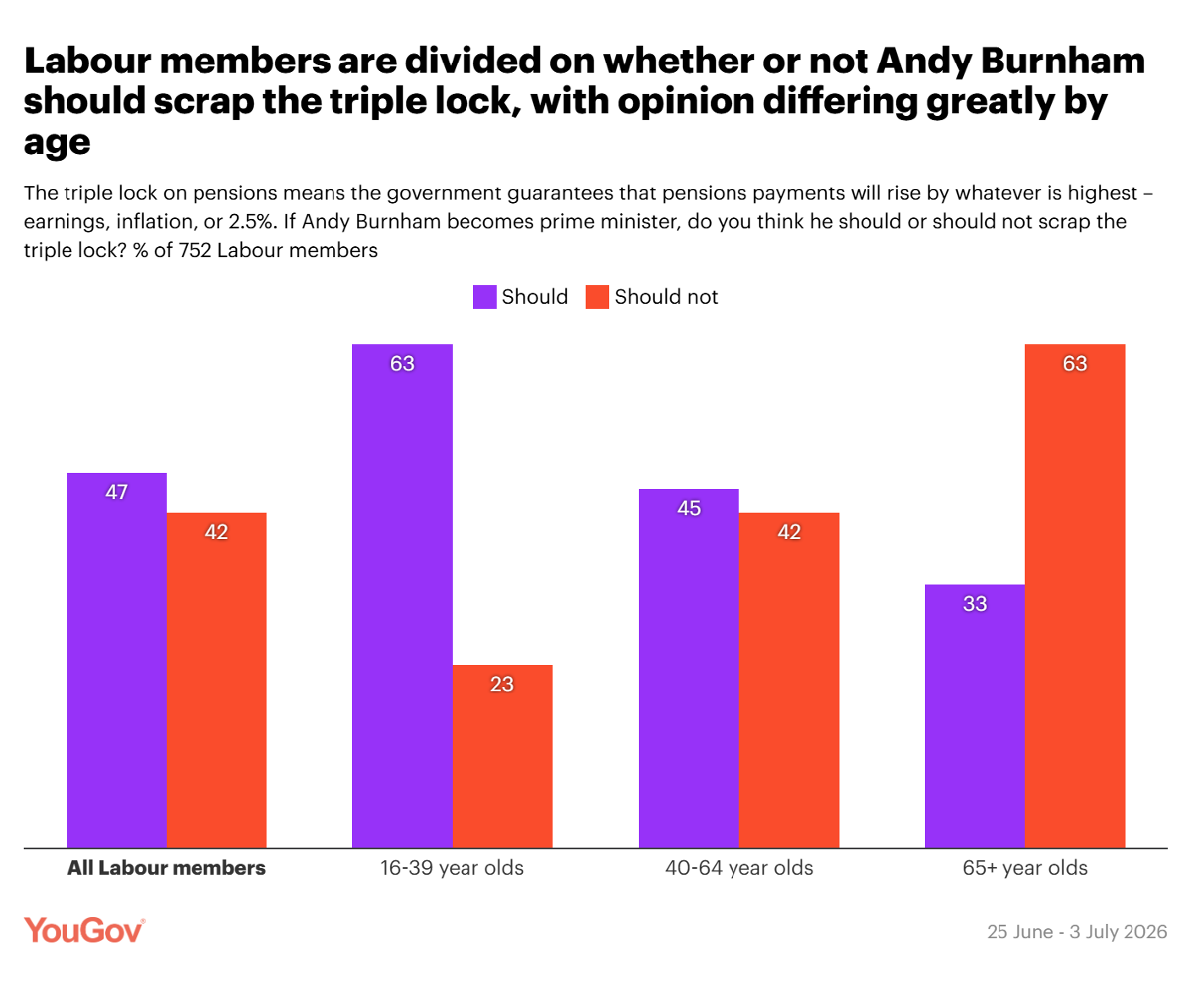

Labour member poll reveals generational divide

YouGov recently ran a poll, asking 752 Labour members whether Burnham should scrap the triple lock. The results, which identify a clear divide across age groups, can be found on the image below.

Source: YouGov.

Across all Labour members it’s a tight call, tilting marginally in favour of the lock getting the boot. Slim discord can also be found among those aged 40 to 64, with only three percentage points separating the results.

When you examine the results from older and younger members, a starker split occurs. Almost two-thirds of 16 to 39-year-olds want to abolish the triple lock, while the same percentage of those aged 65 and over want it to stay.

These results raise few eyebrows. interactive investor’s Great British Retirement Survey 2025 found that 62% of retirees aged 66 and over receive most of their retirement income from the state pension, with one respondent saying: “I wish the state pension was higher. It is a juggling act trying to manage financially.”

The full state pension is currently worth £12,547 a year; a truly valuable source of guaranteed income for retirees. To duplicate this level income through a lifetime annuity would require savings north of £200,000 given current rates. And even then, it’s impossible to draw truly accurate comparisons, as while you can choose an annuity that increases every year, these rises are typically either fixed or linked solely to inflation. You can’t choose a three-pronged uprating mechanism equivalent to or as generous as the triple lock.

- New state pension proposal highlights challenges for younger workers

- Tony Blair Institute’s radical proposal to overhaul state pension

We should note that not everyone above state pension age enjoys the full £12,547 figure. Data from the Department for Work and Pensions (DWP) in 2023 found that only around half of state pension recipients get the full amount, while 150,000 were getting less than £100 a week, under half the full state pension at the time.

Most people need 35 years’ qualifying NI contributions or credits to receive the maximum amount, and some reach state pension age with gaps in their record. Furthermore, if you hit state pension age before 6 April 2016, you’ll likely be on the basic state pension, which is paid at the lower amount of £9,615.

Averting a retirement disaster

In May, former pensions minister Sir Steve Webb, who held the position when the triple lock was introduced, shared his support for the policy, saying that even though it cannot last forever, kiboshing it now could spark a “retirement disaster”. He also said the lock was designed to reverse 30 years of decline in the value of the state pension as between 1980 and 2011 increases were linked to price rises alone.

The question that any sitting government may need to confront before taking any steps to address the matter, is whether the full state pension is sufficient to provide a foundational income in retirement. Pensions UK’s Retirement Living Standards calculate that a minimum lifestyle costs £13,900 a year. The full annual state pension sits some £1,400 below this figure, meaning those who solely rely on it, are struggling to get by.

So, to Sir Steve’s point, abolishing the triple lock now would pose the greatest strain to retirees on the lower incomes, who could plunge deeper into poverty.

What are the alternatives?

The Covid pandemic seems a distant memory now and will be remembered for things other than its short-term effect on state pension hikes. But it did prompt a one-year period where the triple lock was suspended.

In 2021, the end of the furlough scheme, a government grant that covered some of the costs of employers putting workers on temporary leave, distorted the wages data relevant to the triple lock, which rose 8.4%. To avoid an artificially inflated rise to the state pension, the earnings element was ditched temporarily, switching to a double lock of the highest of either inflation or 2.5%, meaning a tamer 3.1% hike was implemented in April 2022.

Some believe that a kind of double-lock system could permanently replace the current regime but feel that deeper and more nuanced reforms are necessary.

The IF suggested what it described as “a more stable and sustainable uprating mechanism”, capping increases at inflation until 2030-31, then switching to the average of inflation and earnings.

The think tank went further with its recommendations, keen to ensure that lower-paid retirees are catered for. It suggested that some of the savings of shifting to a double lock should be channelled to poorer pensioners through a new “Low-Income Pension Supplement” for those in receipt of Pension Credit. The IF claims this would be worth £30 a week, or £1,560 a year, in 2026–27.

- What a Burnham premiership could mean for your long-term wealth

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

Meanwhile, the IFS in July 2025 proposed a “smoothed earnings link”, maintaining the relationship “between the state pension and average earnings, while also making sure that the state pension rises in line with inflation in every period”.

This system means that when average earnings growth is below the rate of inflation, the state pension should increase in line with inflation until the target level of the state pension is reached again – a framework adopted by Australia.

The IFS also suggested that the state pension should never be means-tested as it may disincentivise saving for many people and undermine the various efforts and initiatives to nudge people towards a better financial future.

In the eyes of many, it’s a matter of when rather than if the triple lock will be reformed. Interestingly, it’s not on the agenda for the ongoing third review of the state pension age, so shouldn’t form part of the recommendations.

In any case, given Labour’s manifesto pledge, it seems inevitable that any decision about the mechanism’s future will be parked for the next parliament. And whoever’s in charge may face even sterner pressure to conduct a thorough evaluation of whether the triple lock remains financially viable.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.