Is this shrinking trust sector still worth a look?

A Kepler analyst busts some myths surrounding mergers in a region where the sector’s five investment trusts are soon to be four.

3rd July 2026 14:01

by Alan Ray from Kepler Trust Intelligence

This content is provided by Kepler Trust Intelligence, an investment trust focused website for private and professional investors. Kepler Trust Intelligence is a third-party supplier and not part of interactive investor. It is provided for information only and does not constitute a personal recommendation.

Material produced by Kepler Trust Intelligence should be considered a marketing communication, and is not independent research.

There’s a long-standing urban myth in the medical profession that full moons lead to a rush of expectant mothers going into labour. Having a couple of close family members in the profession, this analyst knows that it’s still not uncommon for a full moon to be remarked upon as a likely precursor to a busy shift.

And being born as the full moon rises is quite a beguiling thought, isn’t it? But sadly, unlike spring tides, the moon has no effect on going into labour or not, and the most likely explanation for the myth persisting is that people tend to remark upon the correlation when a full moon coincides with a busy shift, but don’t when it has been quieter. Not that there’s really such a thing as a quiet shift in the NHS anymore.

There’s also a persistent urban myth in the investment trust sector that M&A tends to occur closer to the bottom than the top of markets. The theory is that investment trusts provide a window on wider investor behaviour, and so when investment trusts start to wind up, it’s a sign that investors have given up on an asset class.

It’s certainly the case that, at a very fundamental level, investment trust discounts are driven by the performance of underlying assets, and persistent wide discounts can be the precursor to M&A activity. However, the other piece of the puzzle is that investment trusts have shareholders who can often be sellers, or indeed buyers, for reasons not associated with markets.

Thus, the whole investment trust sector has been through a well-documented technical discount downturn for a few years as key shareholders from the wealth and multi-asset worlds sell their investment trusts. Consolidation of wealth managers is one of the explanations: a giant organisation managing tens of billions of pounds finds it increasingly hard to own anything other than the largest investment trusts. There’s not much the investment trust sector can do about that other than merge to create larger vehicles, and that’s exactly what has been happening.

The other explanation is the debacle over cost disclosures, which tilted the playing field firmly against investment trusts for a time. This is now largely resolved, but the damage will likely take some time to be undone. Now, it’s certainly true that some M&A has coincided with downturns in various asset classes, but we think it’s important to see that as a contributory factor rather than the main cause. An organisation wishing to sell its holdings in investment trusts is quite logically going to focus on performance in deciding where to start, but that doesn’t quite pass the threshold to be considered an indicator of a market capitulation.

The same pattern has repeated across many sectors of the investment trust universe, but the European and European Smaller Companies have certainly seen their fair share, with the loss of several trusts since the pandemic in what are studiously referred to as ‘combinations’ rather than ‘mergers’. For regulatory purposes, the difference between the two words is important. For conversational purposes, though, ‘merger’ is just fine. The result is a Europe peer group where it won’t be too long before there are just four members.

One of the interesting nuances is that while it’s true that European equities have performed well recently, the dispersion in returns across active fund managers has been very striking. The investment trust Europe peer group’s five-soon-to-be-four remaining members have an NAV total return dispersion of approximately -30% to +100% over the last five years, and there’s a similar pattern in the wider world of actively managed funds.

At an index level, it has been striking too, with the MSCI Europe ex UK Value Index producing a total return of over 80%, and the equivalent growth index a bit less than 30%. We sometimes talk about ‘tailwinds’ and ‘headwinds’ when discussing performance. At this level of dispersion, we should probably be talking about crosswinds. If investment trust managers were sailors, then the last five years would be a bit like an extended version of Cowes Week, where racing in the notoriously changeable winds of the Solent requires huge skill and concentration.

Ironically, this has occurred in a period when the outlook for European economies finally looks more positive than negative. European equity managers have become accustomed to operating without the assistance of a constructive local economy. But various things have happened to change that. The most well-known of those is Germany’s decision to borrow to invest in infrastructure. First, because Germany’s infrastructure is, well, a bit crumbly around the edges, but second, to stimulate Germany’s economy.

Other things are changing too. Some of these are themes across the Continent; others are more localised. For example, there is a well-established determination to shift away from Europe’s dependency on fossil fuels; companies that make grid infrastructure, switching and control systems, undersea cables, sensors, renewable energy equipment, LNG safety equipment – the list goes on.

Europe is also going through a process of reshoring and shows signs of taking its productivity gap with the US very seriously. We have also seen consolidation and improvements in the banking sector, which entered the financial crisis in 2008 in a fragmented, inefficient, and over-leveraged state but today looks a lot healthier and, say it quietly, fund managers are even starting to attach the ‘quality’ label to some of them.

Speaking of the financial crisis, some of the worst-affected countries have been on a long road to recovery. Several southern European countries are experiencing much more encouraging economic performance. Spain is a great example, and this has been boosted further by its long-term investment in renewable energy, highlighted recently by the energy price spikes which Spain sailed through in a much more relaxed manner than many other countries. This may also help explain Spain’s relatively robust political reaction to the same war.

The list of positives goes on, but the most important thing is that markets like change. No, Europe is not going to eliminate its productivity gap with the US any time soon. No, it’s not going to grow its own Magnificent Seven or create a European Silicon Valley. But it is home to many dynamic companies, often trading at a discount to US equivalents, and after an extended period of little to cheer about economically, things look better.

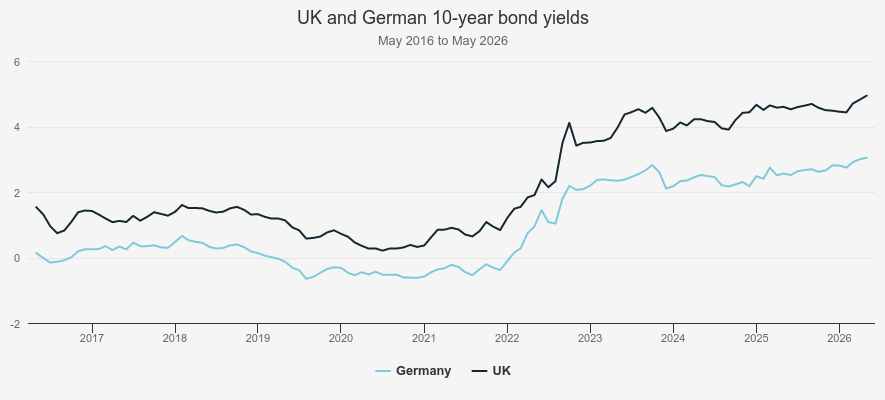

With one of the central positives being the German stimulus plan, it’s always good to keep an eye on the bond markets. The chart below plots UK and German 10-year government bond yields over the last decade. Germany has consistently maintained a lower cost of borrowing than the UK, a recognition of much tighter constraints on running a budget deficit. Readers will be familiar with the hard choices that any UK government faces when considering raising more money from the bond market right now. Germany is in a different position, and the bond market is taking its stimulus package in its stride.

But as the chart below shows, there is still some upward pressure. Germany is coming from a much lower base, though, and the expected stimulus to the economy should justify the extra borrowings. Nevertheless, this is something to keep an eye on, as Germany is expected to run a higher deficit over the next few years. Of course, the ECB recently increased interest rates, recognising that inflation was a risk once again. So, we could say that bond investors are supportive but keeping a close eye on Germany.

BOND YIELDS

Source: Federal Reserve Bank of St Louis.

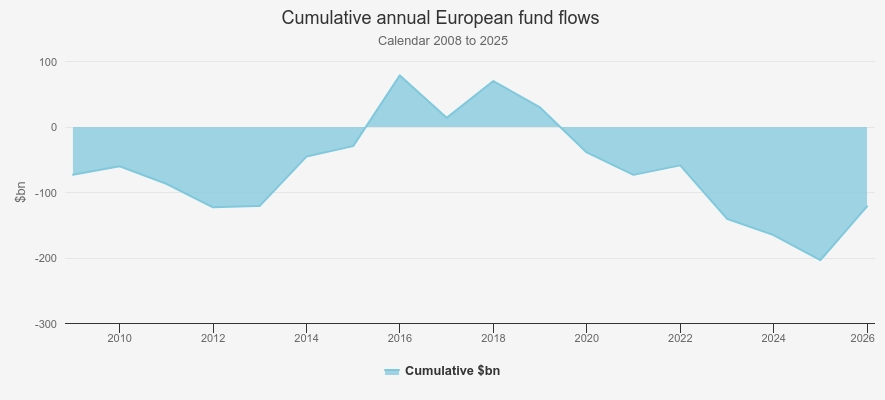

Next, let’s take a look at another measure of investor sentiment. Equity fund flows are the ‘actions not words’ evidence of how investors feel. The chart below measures long-term cumulative fund flows in and out of European equity funds. This is a vast dataset, and so while it doesn’t capture every last dollar of money flowing in and out of Europe, it is a statistically significant sample of global investor sentiment. We find showing this as a cumulative total, rather than as discrete annual figures, quite informative, as it helps to give context.

In this case, the context is that 2025 saw a big inflow into European equities, but as we can see, this hasn’t yet compensated for a long period where investors showed quite a bit of resistance to the attractions of Europe. So, the investment trust M&A mentioned above has come at the tail end of a period of low enthusiasm; European markets have performed pretty well over the last few years of this chart. Again, the read across from what investment trust investors are doing to wider markets isn’t particularly informative.

ANNUAL FLOWS

Source: Morningstar

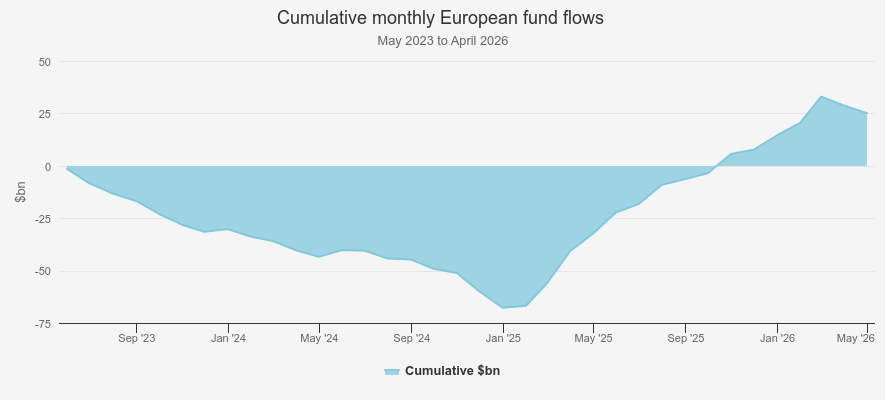

Zooming in on fund flows on a monthly basis below, covering the last three years, we can again clearly see that recently investors have turned positive, but the cumulative total has been below zero until only the last few months. We can also see the ‘risk-off’ phase caused by the US-Iran war recently, which is a pattern repeated in other global markets.

MONTHLY FLOWS

Source: Morningstar

To us, all of this adds up to a picture of improving investor sentiment toward Europe. That improvement is because of several factors – European equity indices have performed pretty well, more optimism about European economics, and investors are still very worried about concentration and valuation risk in portfolios. As the long-term fund flows above show, Europe has been overlooked for so long that it has persistently traded at a lower valuation than the US. It is understandable then that investors might, finally, start paying more attention to a less highly valued market going through positive changes.

One of the most successful navigators of European markets over the last few years is JPMorgan European Growth & Income Ord (LSE:JEGI), which has built an impressively consistent record in a period when growth has led then trailed, value has recovered, and the very nature of what a ‘quality’ business is has come under scrutiny.

This trust has a consistent, repeatable process that looks at value, earnings momentum, and quality factors with an unbiased eye, harnessing both the vast human capital of JPMorgan Asset Management’s global equities professionals as well as its impressive ability to use data scientists to accelerate screening processes. Consequently, it’s no surprise that JEGI is the default rollover option in the most recent M&A transaction, with European Opportunities Trust (LSE:EOT) recently proposing a variety of options for investors, including both JEGI, an open-ended alternative, and a cash exit. You can read a bit more about this in a news article we published recently.

Of course, listed equity isn’t the only way to play things in Europe. In a recent piece, we noted the trend across infrastructure trusts to take on a little more risk in exchange for potentially higher returns. In so doing, more of the sector has moved from its origins in the UK to a more geographically diverse position. Two very good examples are 3i Infrastructure Ord (LSE:3IN) and Cordiant Digital Infrastructure Ord (LSE:CORD).

Equity investors might find either or both of these an interesting diversifier in a European equity portfolio as they share a similar business model of owning and operating businesses associated with infrastructure assets. This means that many of their holdings generate long-term predictable cash flows, which is normally what we think of when discussing infrastructure, but on top of that, ownership of the operating business gives scope to improve efficiency, roll out new assets, and optimise financing and contracts. Strictly speaking, neither is mandated to invest only in Europe, but both are predominantly European (including the UK), and CORD also offers the opportunity to get some exposure to countries like Poland, one of the EU’s up-and-coming economic powerhouses, but which is underrepresented in equity benchmarks.

Investors shouldn’t overlook opportunities in small- and mid-cap companies either. One of the challenges investors face in getting exposure to, for example, the defence sector is that Europe’s largest defence companies are well-known and, in market parlance, ‘well bid’, i.e. share prices seem to be fully up to speed with their growth prospects. Readers will likely know that in Ukraine and, more recently, the Persian Gulf, there has been a shift to low-cost technology that is ‘good enough’ to compete with more expensive technology engineered for perfection. Innovation in defence is therefore occurring both in listed smaller companies, with trusts like The European Smaller Companies Trust PLC (LSE:ESCT)and JPMorgan European Discovery Ord (LSE:JEDT)) both finding opportunities at the more innovative end of the industry.

Baillie Gifford European Growth Ord (LSE:BGEU), which has had a tough time performance-wise, has recently had a portfolio refresh, which we will look at in a forthcoming note, but it retains two very important unlisted holdings. Tekever is a Portuguese drone company which is seeing strong growth and, as military history buffs may already know, is establishing an industrial presence in the UK close to one of the manufacturing hubs for the Supermarine Spitfire in the Second World War, now repurposed as a hub for innovative defence businesses. Separately from the defence sector, BGEU’s largest holding is an Italian software business that has recently filed for IPO on Nasdaq, Bending Spoons. If reports are correct, it could be one of the largest IPOs this year for a European company.

Then there is property. In a recent Kepler webinar, the manager of TR Property Ord (LSE:TRY) discussed a variety of positive factors across Europe. Strictly speaking, TRY is pan-European, with the UK its largest single country exposure, but it provides a great alternative way to get exposure to some long-term growth trends as the European economy reconfigures itself around a more digital business model, driving demand for property assets such as logistics, retail warehouses, and data centres.

Conclusion

In our view, M&A in European trusts is not, despite urban myths to the contrary, a signal of capitulation in markets. For the value-hunting contrarian investor, that might be disappointing news, but the wide dispersion of returns among active managers, some of whom have now exited the investment trust peer group, shows that the more positive market backdrop has been in very specific areas.

We might say the biggest change is that investors see a more positive story for European economies, causing a mindset shift away from some of the stalwart ‘global champions’ and towards more domestic sectors. That is a simplification for sure, but a helpful one to understand what has occurred. This helps answer a more important question than the one about capitulation. After a strong run for (some) European equities, does it still make sense to add to Europe?

We think that the main trends identified above are real and will persist. Evidence suggests investors have increased their exposure to Europe, but the wide dispersion of returns across stocks and sectors is strongly suggestive that this has been a cautious reappraisal, and not speculative. This leaves many successful European businesses, both large and small, that have yet to benefit from this reappraisal of attractive valuations. There is, in our view, still a lot to play for in this revival.

Kepler Partners is a third-party supplier and not part of interactive investor. Neither Kepler Partners or interactive investor will be responsible for any losses that may be incurred as a result of a trading idea.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Important Information

Kepler Partners is not authorised to make recommendations to Retail Clients. This report is based on factual information only, and is solely for information purposes only and any views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment.

This report has been issued by Kepler Partners LLP solely for information purposes only and the views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment. If you are unclear about any of the information on this website or its suitability for you, please contact your financial or tax adviser, or an independent financial or tax adviser before making any investment or financial decisions.

The information provided on this website is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject Kepler Partners LLP to any registration requirement within such jurisdiction or country. Persons who access this information are required to inform themselves and to comply with any such restrictions. In particular, this website is exclusively for non-US Persons. The information in this website is not for distribution to and does not constitute an offer to sell or the solicitation of any offer to buy any securities in the United States of America to or for the benefit of US Persons.

This is a marketing document, should be considered non-independent research and is subject to the rules in COBS 12.3 relating to such research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research.

No representation or warranty, express or implied, is given by any person as to the accuracy or completeness of the information and no responsibility or liability is accepted for the accuracy or sufficiency of any of the information, for any errors, omissions or misstatements, negligent or otherwise. Any views and opinions, whilst given in good faith, are subject to change without notice.

This is not an official confirmation of terms and is not to be taken as advice to take any action in relation to any investment mentioned herein. Any prices or quotations contained herein are indicative only.

Kepler Partners LLP (including its partners, employees and representatives) or a connected person may have positions in or options on the securities detailed in this report, and may buy, sell or offer to purchase or sell such securities from time to time, but will at all times be subject to restrictions imposed by the firm's internal rules. A copy of the firm's conflict of interest policy is available on request.

Past performance is not necessarily a guide to the future. The value of investments can fall as well as rise and you may get back less than you invested when you decide to sell your investments. It is strongly recommended that Independent financial advice should be taken before entering into any financial transaction.

PLEASE SEE ALSO OUR TERMS AND CONDITIONS

Kepler Partners LLP is a limited liability partnership registered in England and Wales at 9/10 Savile Row, London W1S 3PF with registered number OC334771.

Kepler Partners LLP is authorised and regulated by the Financial Conduct Authority.