Stockwatch: take profits or risk going hungry in AI moving feast?

Analyst Edmond Jackson considers a small-cap investment manager and a top-performing technology trust backing SpaceX.

23rd June 2026 11:56

by Edmond Jackson from interactive investor

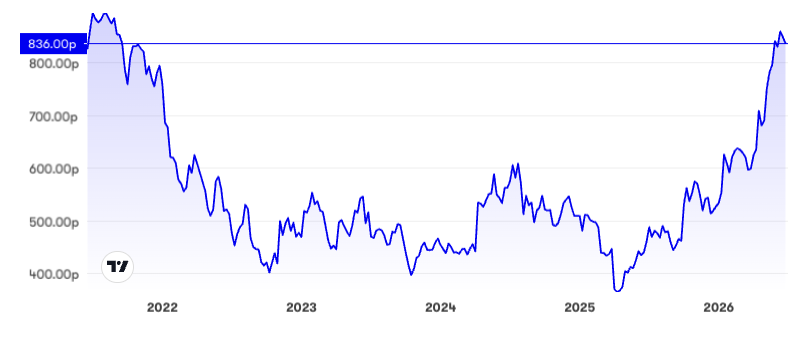

It is interesting to consider the re-rating of the AIM-listed shares of fund manager Polar Capital Holdings (LSE:POLR) from early April to June, up a serious 34% to 872p, and currently 836p.

As if triggered by a 13 April quarterly release showing assets under management (AuM) up 8% in the first quarter of 2026 driven by net inflows of £1,443 million, also £816 million by positive market performance.

- Our Services: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

The five-year chart for POLR looks like quite a “bowl”. Quite what implication (if any) for where tech valuations and Polar go next remains to be seen.

Source: interactive investor. Past performance is not a guide to future performance.

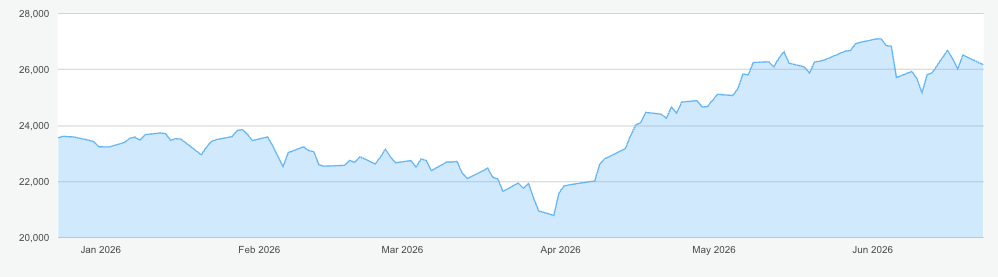

Its latest re-rate does, however, track the Nasdaq 100 index, which re-rated exactly the same from April, with early June profit-taking apparently absorbed:

Source: interactive investor. Past performance is not a guide to future performance.

Technology strategies nowadays account for 51% of Polar’s AuM, hence sentiment towards this asset class is influential for funds’ demand and underlying performance. This compares with 42% in November 2024 when I drew attention to the shares as a “buy” at 535p given an 8.7% yield that looked supported by the interims showing a jump in net cash flow from operations to £15 million.

Polar was also rare at the time for achieving net inflows of client funds relative to chronic outflows in the industry – that had led to shares pricing for high yields due to perceived risk.

- Bill Ackman talks IPOs, SpaceX and favourite tech stocks

- The AIM companies involved in new space race

Showing how tricky judging near-term sentiment can be, alongside fundamentals, the price fell 33% to 360p by April 2025 – an extent that would have triggered stop-loss selling if adhering to this approach. Yet the price is currently up 58% on November 2024 even before consideration of a near 9% yield that buyers could have locked in. Stop losses can be futile where volatile tech is concerned.

I also respected Polar’s success with emerging market and Asian funds (as part of a “growth with diversification” strategy) but its shares seem to remain tied to US tech.

Still looking modestly rated according to fundamentals

After a volatile few years – net profit ranging from around £36 million up to £63 million with sluggish earnings per share (EPS) performance (see table) – consensus expects a 26% advance in normalised EPS in respect of the March 2026 financial year (prelims due 1 July) and 20% to March 2027.

This partly reflects fund managers’ operational gearing when fees are on an improving trend versus relatively fixed costs (unless managers’ bonuses rocket).

Polar Capital Holdings - financial summary

Year-end 31 Mar

| 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| Turnover (£ million) | 179 | 153 | 210 | 226 | 185 | 198 | 226 |

| Operating margin (%) | 35.9 | 33.3 | 36.2 | 27.5 | 24.4 | 27.7 | 22.8 |

| Operating profit (£m) | 64.1 | 50.9 | 75.9 | 62.1 | 45.2 | 54.7 | 51.6 |

| Net profit (£m) | 52.4 | 40.2 | 62.7 | 48.9 | 35.6 | 40.8 | 35.3 |

| EPS - reported (p) | 53.6 | 41.3 | 64.0 | 48.7 | 36.1 | 41.8 | 36.1 |

| EPS - normalised (p) | 53.6 | 41.3 | 64.0 | 55.7 | 40.1 | 41.8 | 45.6 |

| Operating cashflow/share (p) | 76.4 | 43.3 | 78.8 | 74.3 | 45.7 | 42.9 | 65.4 |

| Capital expenditure/share (p) | 0.2 | 0.2 | 0.2 | 0.5 | 0.5 | 0.2 | 0.2 |

| Free cashflow/share (p) | 76.2 | 43.1 | 78.6 | 73.8 | 45.2 | 42.7 | 65.2 |

| Dividends per share (p) | 33.0 | 33.0 | 40.0 | 46.0 | 46.0 | 46.0 | 46.0 |

| Covered by earnings (x) | 1.6 | 1.3 | 1.6 | 1.1 | 0.8 | 0.9 | 0.8 |

| Return on total capital (%) | 57.4 | 41.7 | 46.3 | 38.9 | 29.6 | 38.1 | 37.0 |

| Cash (£m) | 147 | 149 | 194 | 202 | 195 | 160 | 182 |

| Net debt (£m) | -144 | -148 | -190 | -198 | -186 | -153 | -176 |

| Net assets (£m) | 110 | 116 | 151 | 156 | 143 | 136 | 134 |

| Net assets per share (p) | 116 | 120 | 153 | 156 | 142 | 134 | 132 |

Source: company accounts.

At 836p, the 12 months’ forward price/earnings (PE) looks modest at around 12x and there is also a 5.6% prospective yield covered up to 1.5x. Polar qualifies for a Jim Slater Zulu Principle investment screen given a PEG ratio (comparing PE to the expected earnings growth rate) of 0.8 and high returns on capital employed trending over 40% based on interims.

The shares thus continue to look attractive with the caveat that positive bias towards US tech shares is maintained. Enthusiasm for artificial intelligence (AI) continues and huge investment in data centres meant upgrades for big tech earnings.

Yet a surprisingly strong US jobs report triggered fears that interest rates would stay higher for longer to quell inflation; hence the Nasdaq 100 fell 4.2% on 5 June. Growth-type shares tend to be sensitive to interest rates.

The Nasdaq’s swift rebound from 10 June can, however, be seen as a test of support having been met.

Conflicting views on what counts for valuation

Both the £15.7 billion Polar Capital Global Tech I Inc GBP (B42W4J8) fund and £8.0 billion Polar Capital Technology Ord (LSE:PCT) have bought shares in Space Exploration Technologies Corp Class A (NASDAQ:SPCX) and the fund manager is bullish about the forthcoming listings of Anthropic and OpenAI.

Opinions divide powerfully on SpaceX. Analysts at Peel Hunt insist that “it’s all about valuation” whereas Polar’s technology fund manager Ben Rogoff contends that traditional metrics are redundant: “Companies coming to market value themselves based on what they endeavour to become rather than their modest current circumstances.”

It is reflected in the way SpaceX fell over 16% yesterday to $155, valuing it at exactly $2 trillion (£1.5 trillion) versus a $4.9 billion loss in 2025 and with revenues up 15% to $4.7 billion in the first quarter of 2026; possibly near 70x annual sales.

However, there have been countless overpriced (in hindsight) flotations across a variety of sectors, convincing investors initially to pay for potential, so if heeding “what they endeavour to become”, a stock-picker has to be right.

Polar defends this on the basis that some of the most important tech companies came to market on a promise, and you would not touch if guided by PE and cash flow. For example, Alphabet Inc Class C (NASDAQ:GOOG) in 2004, which Polar bought into, making a near 13,500% return. Alphabet’s high valuation at float was criticised by some due to limited use of online services back then.

In parallel, Polar contends that Starlink – the main profit driver within SpaceX – has an addressable market of as much as $1.6 trillion versus $11.4 billion revenue in 2025. The brand could become as recognised as Apple Inc (NASDAQ:AAPL), both having started out with niche appeal, and given that millions of households don’t have decent internet, Starlink has good potential to become mainstream.

More conservative pundits such as Ray Dalio in the US and Jeremy Grantham, the 87-year-old founder of asset manager GMO LLC, argue that AI is a bubble, and for Grantham the brushing aside of regular valuation criteria is a sign that one is under way.

Having specialised in bubbles and profiting from mean-reversion throughout his career, he argues that the AI one will take the entire market down when it bursts, quite like 2000.

I am somewhere in-between. I recall Grantham opining bearishly on equities since his assertion that monetary stimulus following the 2008 crisis persisted far longer than necessary; likewise in reaction to Covid. I would agree in the sense that this contributed to a 2022 bear market when interest rates had to rise versus sticky inflation. Yet such a conservative view would have kept investors low-weighted in equity for nearly two decades with little by way of a trigger to buy, if heeding this macro view.

Similarly in response to the US/Iran war, some analysts warned two months ago that June would herald the real economic crisis, with oil heading over $150 a barrel, yet Brent is $77.5 and the Nasdaq Composite is at a record high. The S&P 500 has also absorbed the Covid and monetary tightening shocks with ease, in a long-term bull market:

Source: TradingView. Past performance is not a guide to future performance.

When might an inflection point arise?

There is now a well-rehearsed argument for how the extent of AI infrastructure investment cannot follow through into profit to match. More likely, hardware orders will fall and boom will lead to bust given the high levels of debt involved. Yet it has been around for a good while and shares continue to rise.

A crowded AI trade does, however, imply a sharp response to any negativity, hence there is a case to preserve some extent of gains amid uncertainty. Earnings releases of “hyperscalers” such as Amazon.com Inc (NASDAQ:AMZN), Alphabet and Meta Platforms Inc Class A (NASDAQ:META) need scrutinising for any reduction in infrastructure spending.

I recall from the 1999-2000 tech boom that locking in gains was very frustrating, with much profit-taking swiftly absorbed and fresh highs soon following. Being lulled into a false sense of security did, however, mean getting caught at the top and feeling the initial drop would rebound, yet it took quality tech shares years and various ones fell away.

- Insider: directors back recovery at two FTSE 250 stocks

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

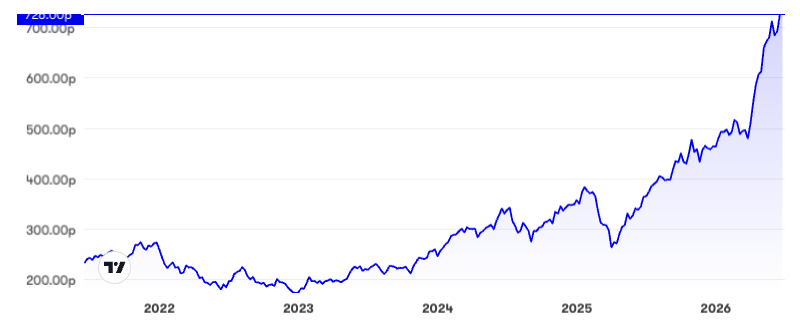

Using Polar Capital Technology Trust as a reference point, its shares have nearly trebled from 263p in April 2025 to around 730p currently, but there is at least a 6% discount to underlying net asset value (NAV) around 780p.

I wouldn’t rely on that for any “margin of safety” given that it is based on market prices unlike a corporate balance sheet’s producing assets.

The five-year chart of Polar Capital Technology Trust does look extended near-term:

Source: interactive investor. Past performance is not a guide to future performance.

Selling an extent into this rise has justification

It significantly depends on your risk preference and whether you are exposed to capital gains. If you locked in a near 9% yield in a tax-free wrapper, that could be material reason to hold.

Yet total return and capital protection are vital. If there is any justice in hedging then I think care should be taken towards US tech valuations; certainly not to be chased and more likely ensure some profit-taking.

I compromise with a “hold” stance if warily, both towards Polar Capital as a manager and its flagship technology trust. They appear still to offer value but the AI feast is a moving one.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.