Stockwatch: why I’m upgrading this small-cap share to buy

If it achieves its targets, this company would be ‘outstandingly good earnings value’, believes analyst Edmond Jackson. This might be a window to invest before various initiatives deliver.

3rd July 2026 11:28

by Edmond Jackson from interactive investor

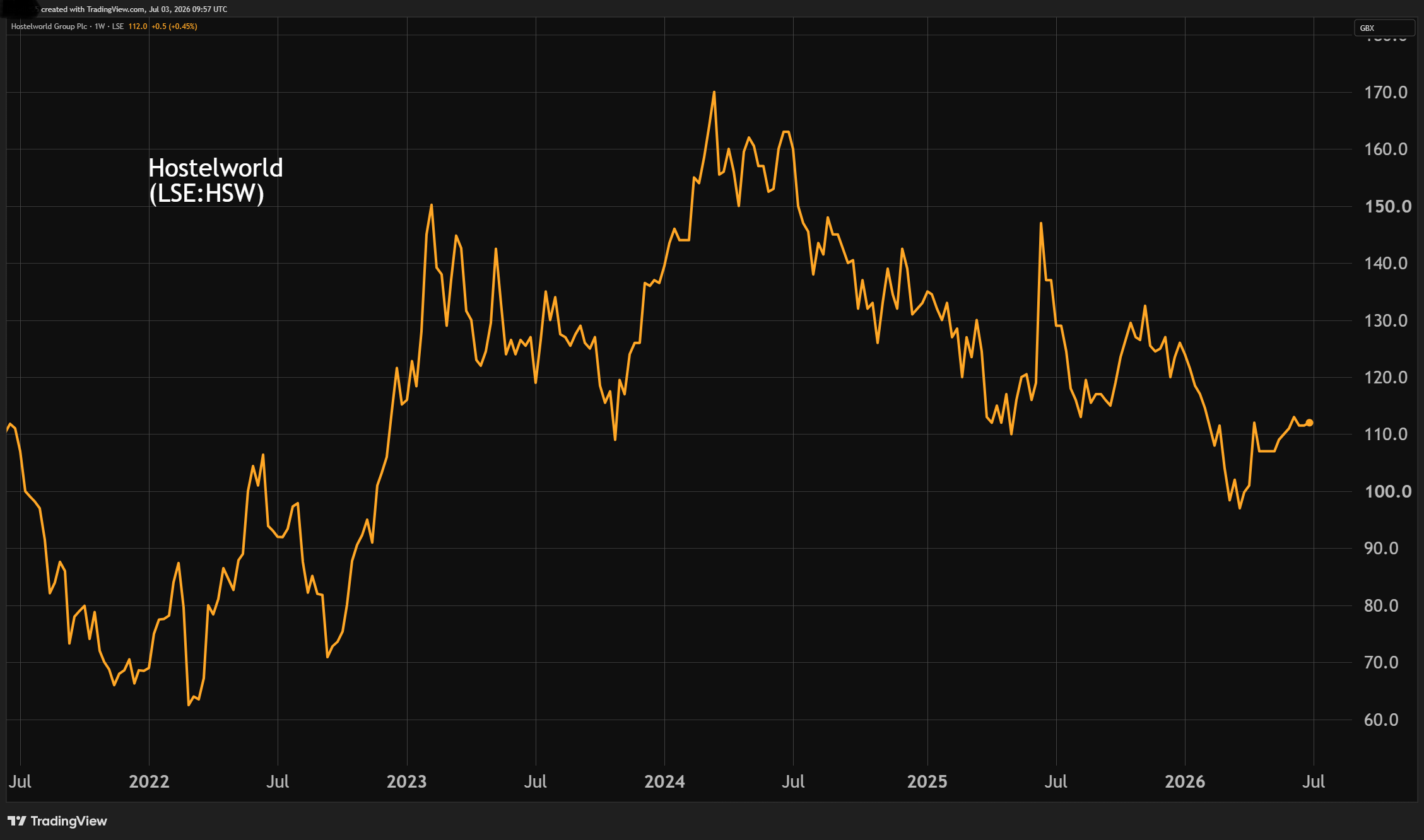

It is interesting to note a modest uptrend in the small-cap shares of online travel agent Hostelworld Group (LSE:HSW) from a 100p low last March.

In a longer-term context this is within an uptrend from a 50p Covid low in March 2020 and a 75p chart low in September 2022.

Previously, the shares had traded above 400p in 2018 and, if consensus forecasts are fair, then at 109p currently Hostelworld trades on a 12-month forward price/earnings (PE) ratio of just 7x and PEG ratio (PE relative to the underlying earnings per share (EPS) growth rate) of 0.2. If achievable, that would be outstandingly good earnings value albeit just a snapshot rather than a multi-year view, and possibly the PEG is compressed near-term into looking very attractive.

- Our Services: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

Revenue growth is also expected to recover, helped by various initiatives, from barely matching inflation in 2025 to 11% this year and 13% next. So, an essential view would see the shares in a recovery trend, potentially with growth characteristics.

Despite the cost-of-living crisis many people want to travel – especially the younger cohort that Hostelworld is presently oriented towards.

Source: TradingView. Past performance is not a guide to future performance.

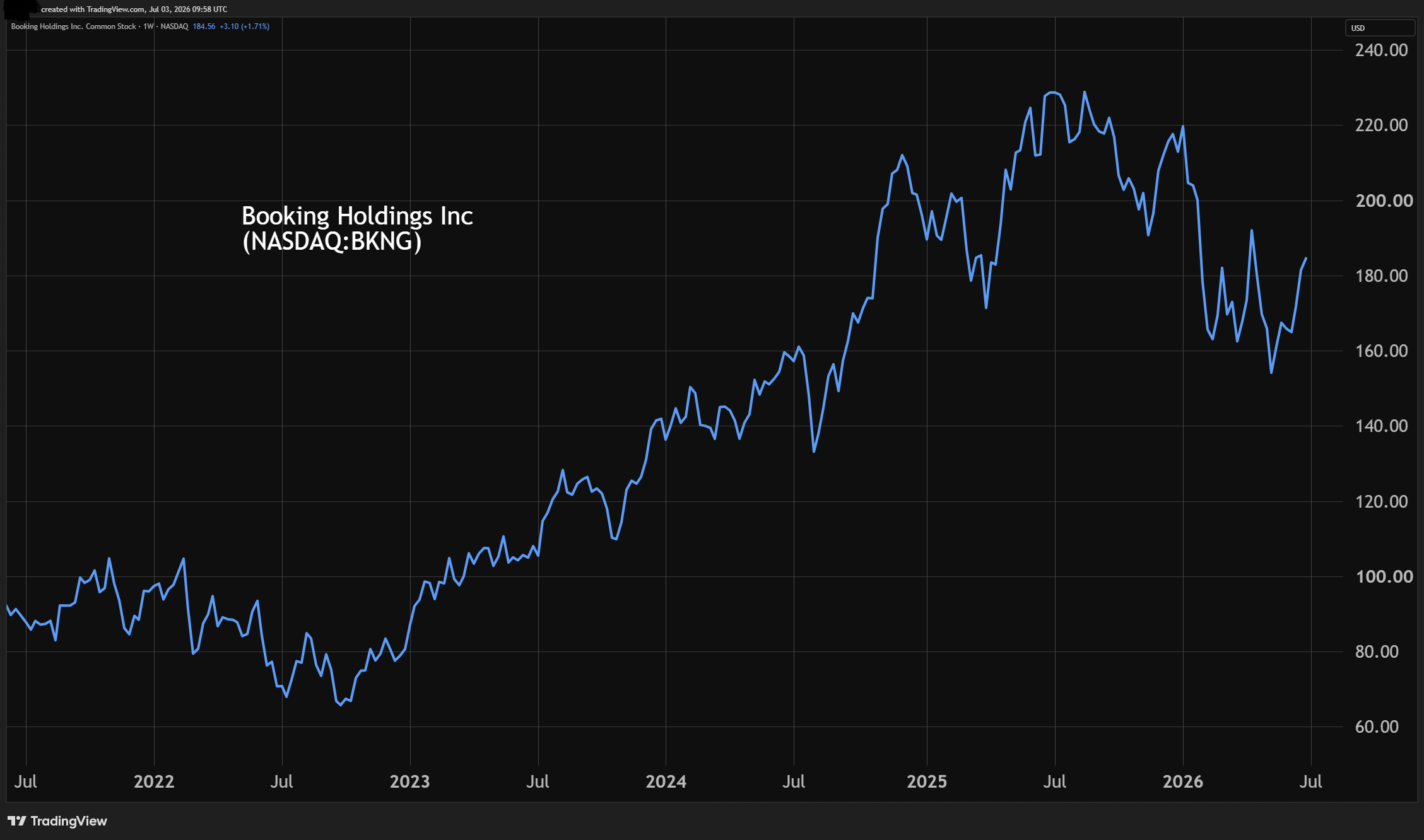

The rating compares with a forward PE of around 17x and PEG of 1.1 for Booking Holdings Inc (NASDAQ:BKNG) , the owner of Booking.com at around $185, although it achieved $26.9 billion (£20.3 billion) revenue last year with an annual growth rate of 16% versus just £81 million equivalent for Hostelworld, up 2% net.

Source: TradingView. Past performance is not a guide to future performance

Founded in 1999 with a focus on budget accommodation, Hostelworld’s chief competitor does seem to be Booking.com, or people simply using Google AI searches in particular locations. Airbnb Inc Ordinary Shares - Class A (NASDAQ:ABNB) has a different emphasis of domestic-type accommodation (whether entire homes or a space within), although Hostelworld is currently expanding its range of accommodation offerings.

Specifically in terms of hostels, the UK’s Youth Hostel Association (YHA) is no encouraging comparator given its contracting estate, partly to cut debt taken on during Covid, although this does limit hostel supply in the UK where those ex-YHAs are converted for alternative use.

- Top stocks and markets in 2026 so far

- Insider Interview: where we are shopping for UK dividends

Versus a current market value of just £135 million, Hostelworld was bought by private equity for around £200 million equivalent in 2009, listed in October 2015 at 185p and saw its revenues impacted by Covid, taking until 2023 to more than fully recover.

After losses of €49 million (£42 million) in 2020, Hostelworld made €9 million net profit in 2024, although this eased to €7 million in 2025. Over €16 million is anticipated this year and €19 million in 2027, comfortably beating €8 million in 2019 pre-Covid.

While the operating margin fell from 12% to 9% in 2025, forecasts imply net profit margins of 15.5% this year and 16.5% in 2027 which, if realisable, now is an interesting time to invest.

Hostelworld - financial summary

year-end 31 Dec

euros

| 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| Turnover (€m) | 80.7 | 15.4 | 16.9 | 69.7 | 93.3 | 92.0 | 94 |

| Operating margin (%) | 4.1 | -325 | -194 | -19.2 | 1.4 | 12.2 | 9.0 |

| Operating profit (€m) | 3.3 | -49.9 | -32.9 | -13.4 | 1.3 | 11.2 | 8.4 |

| Net profit (€m) | 8.4 | -48.9 | -36.0 | -17.3 | 5.1 | 7.4 | 7.0 |

| EPS - reported (€ cents) | 8.7 | -45.7 | -31.0 | -14.7 | 4.1 | 7.0 | 5.4 |

| EPS - normalised (€ cents) | 10.7 | -34.1 | -29.6 | -14.0 | 6.0 | 7.7 | 6.2 |

| Op cash flow/share (€ cents) | 11.7 | -10.3 | -11.8 | -0.6 | 13.8 | 16.7 | 14.3 |

| Capex/share (€ cents) | 3.2 | 3.6 | 3.8 | 4.1 | 3.2 | 4.3 | 6.0 |

| Free cash flow/share (€ cents) | 8.5 | -13.9 | -15.7 | -4.7 | 10.6 | 12.4 | 8.3 |

| Dividends/share (€ cents) | 4.1 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 2.4 |

| Covered by earnings (x) | 2.1 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 2.3 |

| Return on total capital (%) | 2.4 | -49.7 | -31.8 | -14.5 | 1.9 | 15.2 | 9.9 |

| Cash (€m) | 19.4 | 18.2 | 24.5 | 18.2 | 6.7 | 8.2 | 12.2 |

| Net debt (€m) | -15.1 | -12.7 | 3.8 | 13.4 | 4.0 | -7.9 | -1.0 |

| Net assets (€m) | 132 | 97.9 | 67.1 | 52.2 | 59.2 | 70.1 | 73.1 |

| Net assets/share (€ cents) | 136 | 84.1 | 57.7 | 44.5 | 47.9 | 56.1 | 58.8 |

Source: company accounts.

Another US/UK valuation arbitrage?

On 26 June, I noted the progression of offers by FirstCash Holdings Inc (NASDAQ:FCFS) for two UK pawnbrokers, and also Prologis Inc (NYSE:PLD) for property group Segro (LSE:SGRO). These appeared driven significantly by the inherent advantage of higher-rated US businesses buying lower-rated ones in the UK, thereby enhancing earnings even before possible synergies.

Not to base an investment case on takeover speculation, but in the long run it is possible a similar motivation applies for US operators to gain international market share cheaply. Hostelworld is taking various initiatives able to pay off in the medium term.

An Elevate strategy was launched in March 2025 where hostels pay higher commission rates - up from 15.4% to 16.7% - to secure better positioning on the Hostelworld website and app when users search for accommodation. The offering is also being strengthened well beyond hostels, using a third-party inventory supplier initially in 50 destinations and subsequently across 18,000 destinations, which sounds like a substantial re-rate. Offering budget private rooms takes it into competition potentially with Airbnb but it is to include guesthouses and other affordable accommodation.

Evolving from a booking site, Hostelworld is rebranding itself as a comprehensive “social travel platform” involving shared experiences, for example enabling solo travellers to connect with others irrespective of what budget property they book. Messaging leapt over 80% last year where 3.4 million social members book twice as frequently as non-members; and is said to benefit from “a structured, global dataset of events across 750 cities, updated daily, deepening our data advantage”.

- Stockwatch: is this major event a trigger to buy the shares?

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

- Why Glencore shares are tipped to rally over 50%

Social-based recommendations, assisted by AI, allegedly helped marketing efficiency in the second half albeit only at a reduction in such costs to 45% of revenue from 48% in the second half of 2024. They are integral to Hostelworld becoming a “data-led social travel platform” involving “AI-powered travel discovery”. Second-half marketing costs eased to 45% from 48% like-for-like, reflecting the growing benefit of this 3.4 million social member network which books twice as frequently as non-members.

A new “social passes” subscription revenue stream was also launched last November, opening the platform to travellers who do not book accommodation.

At the annual results three months ago, it was said these initiatives had conflated for 3% bookings growth and 12% like-for-like revenue growth in the first quarter, supported by a commission rate of 17.7% and direct marketing costs of less than 50%, which appears to support full-year guidance if sustained. With confidence also in free cash flow conversion of around 70%, this at least supports the prospect that a recent £5 million buyback programme (completed 31 March) can be renewed. At end-2025, balance sheet cash had risen 49% to £12.2 million.

Not surprisingly for an agency-type business, intangibles constitute 98% of £73.1 million net assets, but there was only £14.5 million debt including leases, hence only £2.3 million on a net basis. With £6.7 million accruals (money earned but not yet paid) current assets of £16.5 million were slightly outweighed by £18.1 million current liabilities, but overall the balance sheet looks satisfactory in support of development.

The 6 May AGM statement reiterated such guidance, saying that year-to-date revenue momentum had been maintained despite challenging macroeconomic conditions including the Middle East conflict. Long-haul demand from Asia had seen some softness albeit offset by strong intra-European travel, with overall revenues not materially affected to date.

Capital upside potential plus speculative intrigue

Hostelworld may not be a most exciting business yet there currently looks a current window to invest before various initiatives deliver, as early signs show they should for 2026 onwards. Higher living and travel costs should prompt interest in budget accommodation.

An improvement in PE simply from 7x to 10x would be material for capital value implying a 170p target based on the 2027 EPS consensus.

Admittedly, there is no real record of dividend payments despite nearly seven years of listing. But a maiden payout of 2.4p per share last year is expected to rise to 4.7p in respect of 2027, implying a material 4.3% yield with 3.6x cover.

There is potentially synergy for the AI initiatives to be applied to a much larger business if they can integrate well enough, and the “earnings arbitrage” element anyway presents takeover appeal.

I examined Hostelworld last October at 124p, concluding a “hold” stance was appropriate given its first nine months of revenue was broadly flat. I upgrade to “buy” now due to better financial growth prospects.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.