Bond Boss: why gilt yields are so high, and what it means

Gilt yields have risen even as growth slows. Here’s what’s driving the move and what investors need to understand.

24th June 2026 09:05

by Jonathan Mondillo from Aberdeen

For years, investors worked with a simple assumption: when growth slows, bond yields fall and bond prices rise.

But today’s market is telling a different story. UK government bond, or gilt, yields are rising - even as the economic outlook looks increasingly uncertain. That means bond prices are falling.

So, why are gilt yields heading higher? And what does it mean for investors?

- Invest with ii: Buy Bonds | Free Regular Investing | General Investing with ii

Why are gilt yields heading higher?

At first glance, the current environment should support government bonds. Growth risks have increased and geopolitical uncertainty is high. But to understand why gilt yields have moved higher, it’s worth looking at the three components that make up that yield:

- Expectations for future interest rates

- The inflation outlook

- An added cushion for uncertainty, known as the ‘term premium’.

The Iran conflict has pushed all three higher - particularly through its impact on energy prices and inflation expectations.

At the start of the year, expectations were so different. 2026 should have been the year that UK inflation finally falls below 2%, allowing the Bank of England (BoE) to make at least two interest rate cuts.

But it wasn’t to be. Higher oil and gas prices mean inflation potentially edges higher. This puts the central bank in an uncomfortable position.

Markets have moved accordingly. Gilt yields have inevitably moved higher to reflect stronger inflation, higher expected BoE interest rates and greater uncertainty. And that’s before politics enters the picture.

But why have gilts performed worse than other countries?

The scars of 2022 still linger. The energy-price surge that year, saw UK inflation move aggressively higher and stay elevated longer than in Europe and the US.

When energy prices rose again this year, with the lessons of 2022 still fresh, UK yields reacted more sharply to oil than those in other markets.

Then we have the politics. The gilt market is fragile enough at the best of times. Higher oil prices were damaging enough but another bout of UK political turmoil then pushed gilt yields sharply higher in May.

The UK’s public finances are under pressure. That makes investors more sensitive to any suggestion of higher borrowing, particularly during periods of political uncertainty. This is one reason UK borrowing costs have risen faster than in other markets.

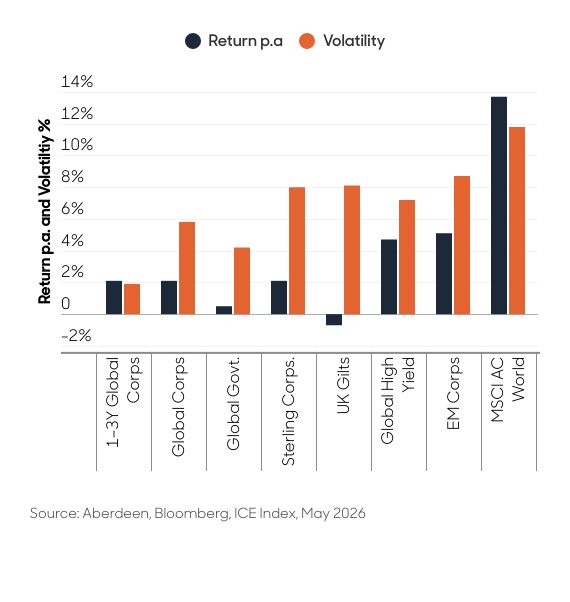

Gilts haven’t been behaving for a while

Over the past decade, UK gilts have delivered slightly negative annual returns, while experiencing volatility comparable to sterling corporate bonds.

By contrast, global government bonds have produced modest positive returns with lower volatility (see Chart 1).

Chart 1: Bonds 10-year return & volatility

Source: Aberdeen, Bloomberg, ICE Index, May 2026.

More striking is how gilts behave in times of stress.

Since early 2021 - a period marked by repeated shocks, from the pandemic and domestic political instability to war in Ukraine and recent energy supply disruption - gilts have often been more volatile than comparable corporate bonds.

This challenges the idea they provide consistent stability.

Why have gilts been more volatile?

To answer this, we need to go back to the three components that drive yields: expectations for future interest rates; the inflation outlook; and the ‘term premium’.

Inflation surged in 2022 and has remained stubbornly high. This means the BoE had to raise interest rates very quickly and only reduced them slowly.

What’s more, political risk is ever present.

The 49-day tenure of former prime minister Liz Truss put the UK’s strained public finances in the global spotlight. Since then, bond investors have scrutinised every fiscal decision, from Budgets to Spring Statements.

- Bond Boss: relief rallies and volatility - bonds still the real stress test

- Bond Boss: why short-dated income is back in favour

What direction will gilt yields head this summer?

Our base case is that yields move lower.

We expect the peace process in the Middle East to hold. If it does, oil and gas prices should continue to fall, easing inflation pressures. That would give the BoE room to stay on hold and possibly start signalling rate cuts next year. In that scenario, gilt yields should fall. We particularly favour short-dated gilts.

Politics may still cause some short-term volatility, but it does not change the broader outlook. Markets have been reassured by signals from Andy Burnham, who is likely to succeed Keir Starmer as prime minister, that the current government’s fiscal conservatism will stay in place. That confidence should hold over the medium term.

The combination of lower oil prices and reduced political tension may be enough to put downward pressure on gilt yields for the rest of this year.

How about the medium term, will that volatility dissipate?

The conditions are in place for the gilt market to regain its reputation as a more traditional and steady asset class.

Inflation may rise in the short term before moving back towards 2%. Unlike in 2022, the labour market is now weaker, so higher inflation is less likely to trigger faster wage growth and a new inflation spiral.

Recent political turmoil has taught UK politicians not to underestimate the gilt market. It is central to the economy. The quickest way for the government to improve public finances is via reduced borrowing costs (lower gilt yields).

- Everything you need to know about investing in gilts

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

While unlikely at this point, a leadership contest could cause some short-term volatility, but if Burnham sticks to the fiscal rules, that disruption should be limited.

What options are available when it comes to gilts?

One way to think about bonds is to separate what drives returns. Investors do not simply ‘own’ bonds. They hold a combination of:

- Income, from coupon payments

- Price exposure, driven by changes in yields.

This is particularly relevant for gilts, where coupon structure plays an important role:

Low-coupon gilts provide less income and rely more on price movements for returns. They can be more tax efficient for UK investors, as capital gains are not taxed on gilts.

High-coupon gilts, by contrast, offer greater income upfront, but that income is taxable outside a tax wrapper.

The result is a trade-off: tax efficiency versus income. In a higher-yield environment, this distinction becomes more important.

When yields are high and uncertainty remains elevated, understanding how gilts generate returns - through income, price movements and tax treatment - becomes more important than ever.

Special thanks to Matt Amis and the rates team for their insight on this topic.

Jonathan Mondillo is global head of fixed income at Aberdeen.

ii is an Aberdeen business.

Aberdeen is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.