Bond Boss: why short-dated income is back in favour

In his latest monthly column, Aberdeen’s Jonathan Mondillo explains that when bonds stop behaving, shorter maturities can help investors sleep a little easier.

9th April 2026 11:42

by Jonathan Mondillo from Aberdeen

For years, bonds played a reassuring role in portfolios. When shares stumbled, bonds usually stepped in to steady the ship.

Last month reminded investors that this comforting rule isn’t a law of nature. Sometimes, bonds don’t behave at all.

Think of it like a well‑trained dog that suddenly bolts when it hears a loud bang. You’re left standing there, leash in hand, wondering what just happened.

- Invest with ii: Investing in Bonds | Free Regular Investing | Open a SIPP

When the shock isn’t fear — it’s inflation

This time, the bang wasn’t a stock market wobble. It was inflation.

A surge in energy prices — triggered by rising geopolitical tensions — pushed oil above $100 a barrel. That didn’t just spook markets; it forced investors to rethink the path of interest rates.

And when inflation is the problem, bonds don’t always come to the rescue.

Instead of rallying, government bonds across the US, UK and Europe sold off sharply. Yields rose. Prices fell. Shares struggled too.

It felt uncomfortably familiar — more like 2022 than the tidy ‘risk‑off’ playbook many investors have grown used to.

A quick myth‑buster: bonds aren’t risk‑free

Government bonds are often described as ‘risk‑free’ but that’s only half the story.

Yes, the chance of the UK or US government failing to repay its debt is vanishingly small. But that doesn’t mean bond investors can’t lose money along the journey to a bond’s maturity date.

The real risk comes from how sensitive bond prices are to interest rates — something known as ‘duration’.

Here’s a simple way to think about it. The longer a bond’s maturity, the more it behaves like a spring:

- When yields jump, long‑dated bond prices snap back hard

- Short‑dated bonds? Much stiffer. Less dramatic moves.

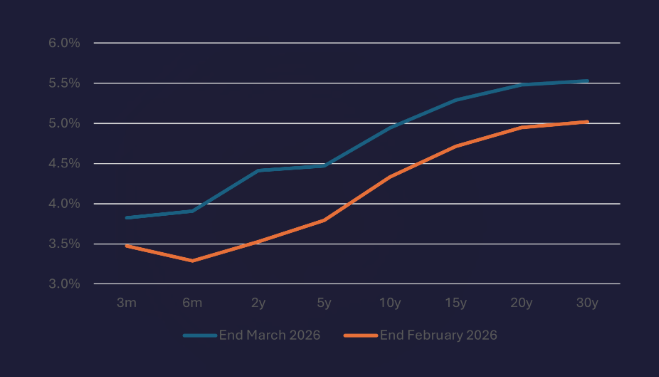

Last month, that difference mattered a lot (see Chart 1).

Chart 1: UK gilt yields (one month – 30 years) in March 2026

Source: Aberdeen.

Why bonds fell at the same time as shares

Two forces were at work.

First, markets began to question whether central banks could really cut rates as soon — or as much — as previously expected. Higher oil prices risk feeding inflation, and inflation makes rate cuts harder.

Second, investors demanded extra compensation for holding long‑dated bonds. This ‘term premium’ tends to rise when inflation feels unpredictable.

Put those together and you get higher yields along the length of the curve — exactly where bonds with longer maturities and greater duration sensitivity are most vulnerable.

In other words, investors weren’t fleeing to safety. They were repricing risk.

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

- Bond Boss: an income play less dependent on rate changes

Why shorter‑dated bonds held up better

This is where short‑dated income strategies start to look more appealing.

Short‑dated bonds (typically maturing in one to three years) are less sensitive to sudden jumps in yields. That’s because:

- More of the return comes from income, not price movements

- You’re closer to getting your money back at maturity.

A handy rule of thumb to remember is that if yields rise by 1%, a bond’s price falls by roughly 1% for each year of duration.

So, when yields move quickly, long bonds feel the pain. Short bonds bruise, but don’t break.

‘Yield is doing more of the work’

Another way to think about it is this: today, bonds don’t need falling yields to earn their keep.

With yields higher than they were a few years ago, a larger chunk of returns now comes from the income paid along the way — often called ‘carry’.

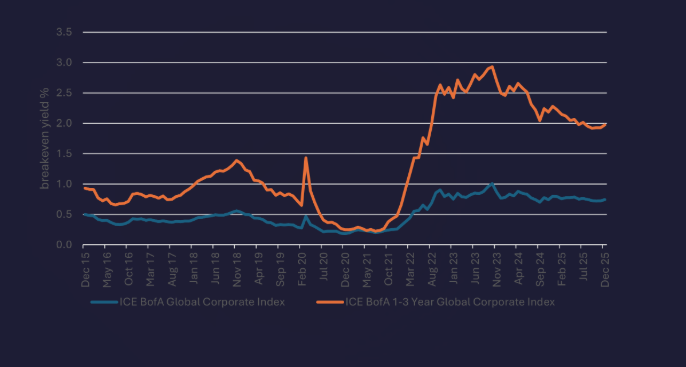

That income acts like a cushion for investors. Even if yields drift higher, the bond can still deliver a positive return over time (see Chart 2).

Chart 2: How much yields need to rise to reduce return to zero

Source: ICE BofA Global Corporate Index, ICE BofA 1-3 Year Global Corporate Index, December 2025.

Short‑dated bonds benefit most from this dynamic. You’re being paid while you wait, rather than betting heavily on where interest rates go next.

Income versus duration: what do you really own?

Many investors think they ‘own bonds’ but in reality, they’re choosing a mix of two things:

- Income — contractual cashflows over a known timeframe

- Duration — a view on where yields and inflation are heading.

Owning income is about collecting steady payments. On the other hand, owning duration is about being right about the future.

March showed how uncomfortable that second bet can be when inflation shocks arrive suddenly and markets reprice in a hurry.

So, what’s the takeaway?

Short‑dated income strategies aren’t magic. They’re not risk‑free, and they won’t be immune to volatility.

But in a world where inflation shocks travel faster than central banks can react, they offer something many investors value again: control.

Control over interest‑rate sensitivity; control over the journey, not just the destination.

When bonds stop behaving, shorter maturities and dependable income can help restore some discipline to portfolios — and help investors sleep a little easier along the way.

Jonathan Mondillo is global head of fixed income at Aberdeen.

ii is an Aberdeen business.

Aberdeen is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.