Have delayed mega-IPOs intensified pressure on AI funding?

A boom in AI spending may have consequences not just for companies involved but every investor and the entire US economy. Analyst John Ficenec explains why and what the outcomes might be.

30th June 2026 14:17

by John Ficenec from interactive investor

The logos of OpenAI and Anthropic. Photo: Imen Ben Youssef/Hans Lucas/AFP via Getty Images.

At the very heart of the AI spending boom is the rather large question of how it is all going to be paid for. The two largest AI companies Open AI and Anthropic are showing incredible growth but also yawning losses.

While the possibilities of the new technology are tantalising, they aren’t making anywhere near enough money to support themselves. The picture is further complicated because being private companies they publish no accounts. In situations like this, it is best to follow the money of those paying the bills to try and understand what is going on.

- Invest with ii: Open a SIPP | Best SIPP Investments | SIPP Cashback Offers

Who is picking up the tab?

The challenge is that while programmes like Chat GPT and Claude are experiencing exponential growth, it is still unclear how many customers will be willing to pay and at what price. The likes of Claude developer Anthropic and Open AI, which built Chat GPT, need constant financial support as, despite record revenues, they operate at massive losses.

While there has been steady funding from major investors like the Singapore sovereign wealth fund GIC, Softbank and the Qatar Investment Authority, what is unusual about these new AI companies is that the heavy lifting is coming from other technology firms Alphabet Inc Class A (NASDAQ:GOOGL), Meta Platforms Inc Class A (NASDAQ:META), Amazon.com Inc (NASDAQ:AMZN) and Microsoft Corp (NASDAQ:MSFT).

The question is how long these companies can continue to shoulder the cash needs of the AI boom. All this is against a backdrop where one of the main sources of funding is becoming increasingly expensive.

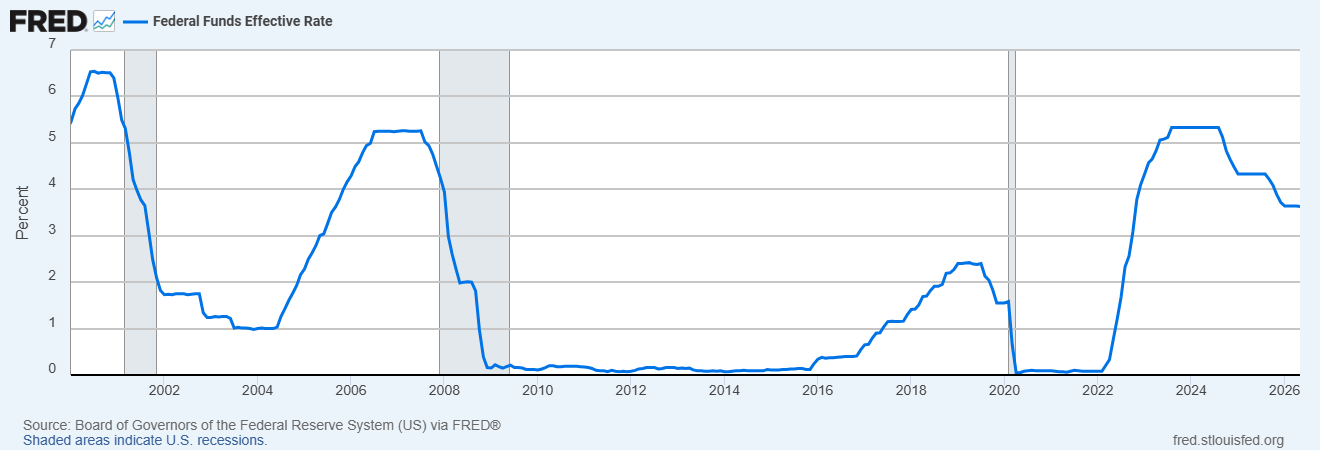

Rising rates

The cost of debt is soaring which is a significant headwind for technology companies. Looking at Microsoft during the first two decades after its 1986 stock market listing, it hardly carried any debt. Even up until 2010 it only had $4.9 billion (£3.7 billion) in long-term borrowing, but with near zero interest rates after the 2008 financial crisis, that borrowing ballooned. Microsoft was borrowing $60 billion long term by 2020, having peaked at around $66 billion a year earlier.

- Bill Ackman talks IPOs, SpaceX and favourite tech stocks

- Stockwatch: take profits or risk going hungry in AI moving feast?

It made perfect sense for Microsoft to borrow when it was so cheap. In 2015, it could borrow $5 billion in short-term commercial paper, which is between a week and two months, for 0.12%. However, that cost jumped to 5.4% by 2024. The long-term borrowing, which is typically more expensive to cover the risk, was costing on average 2% in 2015 but jumped to 4% by 2025.

US Federal funds rate – 2000 to 2026

Microsoft is not alone in reaching for the debt lever. Amazon funded expansion between 2000 and 2010 largely through the cash it generated, while at the same time paying no dividends or share buybacks. That changed with near zero interest rates in 2009, and long-term debt jumped from $184 million in 2010 to $33.2 billion 10 years later and had doubled again by the end of 2025 to $66 billion.

Meta had no long-term debt at the end of 2020, yet by the end of 2025 it had borrowed an extra $58.7 billion. Alphabet has seen long-term debt jump from $2 billion in 2015 to $14 billion by 2020 and $46 billion by 2025.

Higher debts always increase the risk to shareholders as it has a claim on assets ahead of shareholders. If trading and profits slow then debt is repaid first. But borrowing is never viewed in isolation, it must be considered against how profitable the company is, how much cash it generates to pay those debts and how much of those profits are retained within the company, increasing the value of the shareholders equity.

Profit machines

On the surface there is nothing to worry about in the world of tech. Amazon may have seen long-term debt double in the past five years, but its net income has tripled from $21 billion in 2020 to $78 billion at the end of 2025. The value of the equity has quadrupled to $411 billion over the same period. So, while Amazon’s long-term debt was 35% of its equity in 2020, it has halved to 16% of the equity at the end of 2025.

- AI boom or bubble? How to navigate risks and opportunities

- Stockwatch: should you follow Warren Buffett into tech giant?

Microsoft had long-term borrowing of $60 billion at the end of 2020 against equity of $118 billion, or 51%, and generated $44 billion in net income that year. By the end of 2025, the long-term debt was $40 billion against equity of $343 billion, or 12%, with net income of $102 billion. Using a standard leverage ratio of debt to equity, the risk to shareholders is falling.

Circular economy

Despite this, it is important to dig into the quality of those earnings because they are unlike anything seen in the past 40 years. Take Microsoft as an example; it makes software like Windows, which is the operating system for nearly all personal computers, alongside programmes such as Word, Excel, etc, packaged in Microsoft 365 for work. It also builds and supports the networks needed for companies to run their systems. This is all very much in the line of business, of creating a product or a service and selling it.

More recently that business has become blurred by AI investment. Microsoft first invested $1 billion in Open AI in 2019, three years before Chat GPT was launched, cementing its position with another $10 billion in early 2023 and holds 27% of the company. This deal ensured that Open AI uses the Microsoft Azure cloud computing system to run its large language model programmes like Chat GPT. Each time Chat GPT is asked a question, it uses a large amount of computing power to come up with an answer, which is provided by Microsoft Azure data centres which charge for that use.

Microsoft had it written into the terms of Open AI that if they needed any new computing power, they had to use Microsoft data centres first. This changed in a reorganization of Open AI at the end of last year where Open AI was allowed more flexibility to use other data centres to power Chat GPT. But Open AI is still contracted to use Microsoft data centres first to power the API system, which is the version of Chat GPT used by professional developers and companies, and is arguably the larger potential revenue driver. Microsoft is also entitled to recognise 20% of Open AI revenue.

Microsoft executives revealed that they had spent over $100 billion on Open AI during the past six years, on a company that is contractually obliged to use their data centres. It is those same data centres, running the Azure cloud computing services, that are powering Microsoft’s results to record highs of revenue and profit.

Amazon is a similar picture as it holds a significant investment in Anthropic, which in turn uses Amazon Web Services (AWS) data centres to power Claude. AWS has driven the revenue and net income growth during the past five years, and because they don’t pay dividends or share buybacks, the equity has also soared.

Amazon also benefits as the value of Anthropic has increased from $65 billion in early 2025 to $965 billion in the latest May fundraise. In the first quarter of 2026, Amazon recognised $16.8 billion in non-operating income from the jump in Anthropic’s value, which is over half of the total $30 billion in net income for the period.

The issue here is that the tail is beginning to wag the dog where AI investing is concerned. Microsoft and Amazon are now so dependent on AI for earnings growth it becomes difficult to stop committing to more investment. And it is only the technology giants Microsoft, Amazon, Meta and Alphabet that have the firepower to fund the build out of data centres.

Cash squeeze

We are approaching an inflection point within the next six months, one that we may have already passed, where the technology companies are spending more money on AI than they are making from other parts of the business. Amazon said free cashflow had fallen to $1 billion in the preceding 12 months, compared to $26 billion at the same stage a year earlier due to spending on data centres. Microsoft free cashflow fell 22% in the third quarter ended March, and Meta generated $12 billion in free cashflow during the first quarter, but after increasing capital spending targets to between $125 billion and $145 billion, some analysts forecast negative free cashflow by the end of this year.

There has been an explosion in pseudo borrowing at the technology companies too. That is contractual agreements to pay for services in the future that don’t all appear on the balance sheet. Microsoft has seen construction commitments increase from $5 billion in 2020 to $32 billion in 2025, and purchase commitments soar from $27 billion in 2020 to $110 billion in 2025, the majority of which are due in the current financial year. Add together the long-term debt, leases, construction and purchase commitments, and the total is more than doubled from $179 billion in 2020 to $397 billion in 2025.

The cash burn that is needed to fund an estimated $725 billion in capital investment this year goes some way to explaining the sudden rush to raise funds. Alphabet raised $20 billion in debt earlier this year, including a 100-year bond, and this is on the back of around $17.5 billion raised at the end of last year. Meta raised $25 billion earlier this year and is thought to be exploring an $85 billion equity issuance. Amazon raised $15 billion in debt at the end of last year, $40 billion in March and another $17.5 billion in June.

- Ian Cowie: how I’m investing in space

- How will SpaceX affect tracker funds?

- Investing in space: funds, trusts, and ETFs offering a route in

What would greatly relieve the pressure would be either a sudden increase in paying customers for AI, rather than just a huge spike in usage from people doing their homework and photoshopping kittens. Or, if both Open AI and Anthropic can IPO, then raising money from public markets would provide fresh funding.

That is why the Space Exploration Technologies Corp Class A (NASDAQ:SPCX) IPO has become so crucial to the fortunes of the entire sector. The continued success of SpaceX is needed to support investor appetite for the $1 trillion valuation of Anthropic and Open AI. It was hoped that both Anthropic and Open AI would quickly follow on to the stock market, but those plans seem to have stalled on cooling investor appetite. Open AI filed confidential draft listing documents with US regulators in early June, but it is thought to be delaying until next year now rather than accept a valuation below $1 trillion. Anthropic has filed similar documentation, with analysts expecting an IPO around October this year.

A bridge too far?

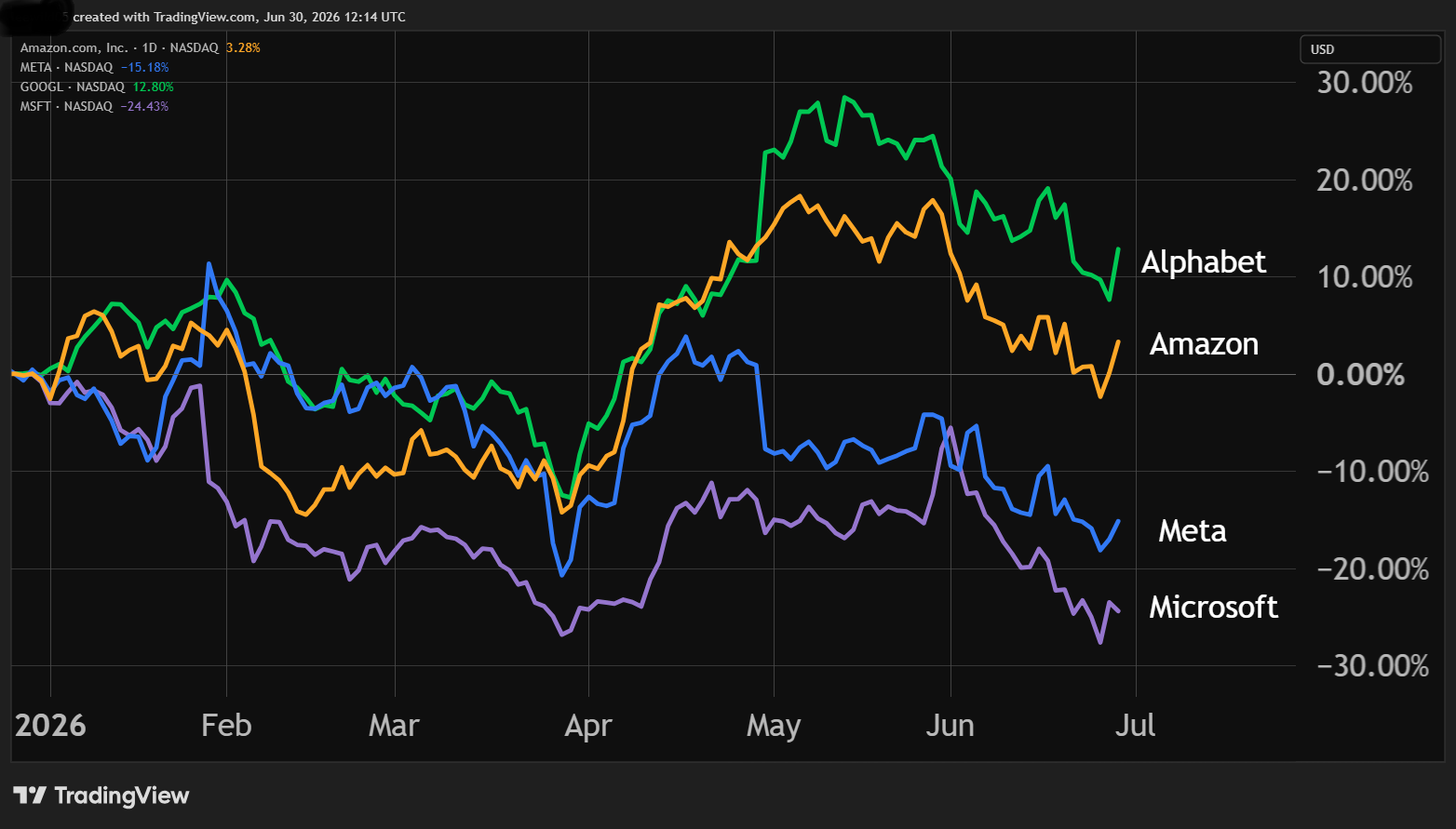

In the absence of fresh funds from public markets, the burden of spending will have to be borne by Meta, Amazon, Microsoft and Alphabet. This goes some way to explaining the varying fortunes this year with Alphabet up 8%, Amazon flat, Meta down 17% and Microsoft down 23%.

Source: TradingView. Past performance is not a guide to future performance.

We’ve been here before where the technology sector has required heavy investment before the vision of its founders was realised. Amazon was loss making for many years before the share price exploded. They would argue they should be given the benefit of the doubt given stellar past performance. But the past success was based on strong cash generation or during a period when borrowing was almost free and money was being pumped into the economy.

Source: TradingView. Past performance is not a guide to future performance.

That leads us to another solution which has been mooted - US government intervention. Given how important the AI sector has become to the US economy, President Donald Trump has raised the possibility of taking strategic stakes in these AI companies to secure the technology and support growth. If AI spending was to stall, the economic growth of the US would almost grind to a halt. Trump has already taken a 10% stake in chip maker Intel Corp (NASDAQ:INTC) due to its critical role in the supply chain.

Right now, the pressure is building in the world of technology. The cost of borrowing needed to fund these investments has risen sharply, and the amount of that borrowing has risen sharply too.

The AI companies themselves are still loss making, and while there is nothing inherently wrong with this, the publicly listed companies that are funding the growth are blurring the lines between the belief of the founders in this technology and the fiduciary duty to people who hold the shares. Every pound, or dollar spent by the publicly traded companies must be done with the express aim of maximising returns for shareholders.

This has undoubtedly been true with exceptional share price gains from AI up until now. But the drift in the fundamental strategy of these companies from their classic model of selling products and services to investing billions in private companies, has increased risks to shareholders, and the profitability and returns are yet to be proven.

John Ficenec is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.