Stockwatch: high stakes for one of UK’s most-shorted shares

Professional investors are betting against this company in droves, but analyst Edmond Jackson believes this crowded trade could trigger the mother of all short squeezes.

19th June 2026 11:24

by Edmond Jackson from interactive investor

Housebuilding shares have had a volatile week, weighing the impact of a sudden breakthrough towards a Middle East peace deal and the prospect of a new leftwards Labour government on UK inflation and interest rates.

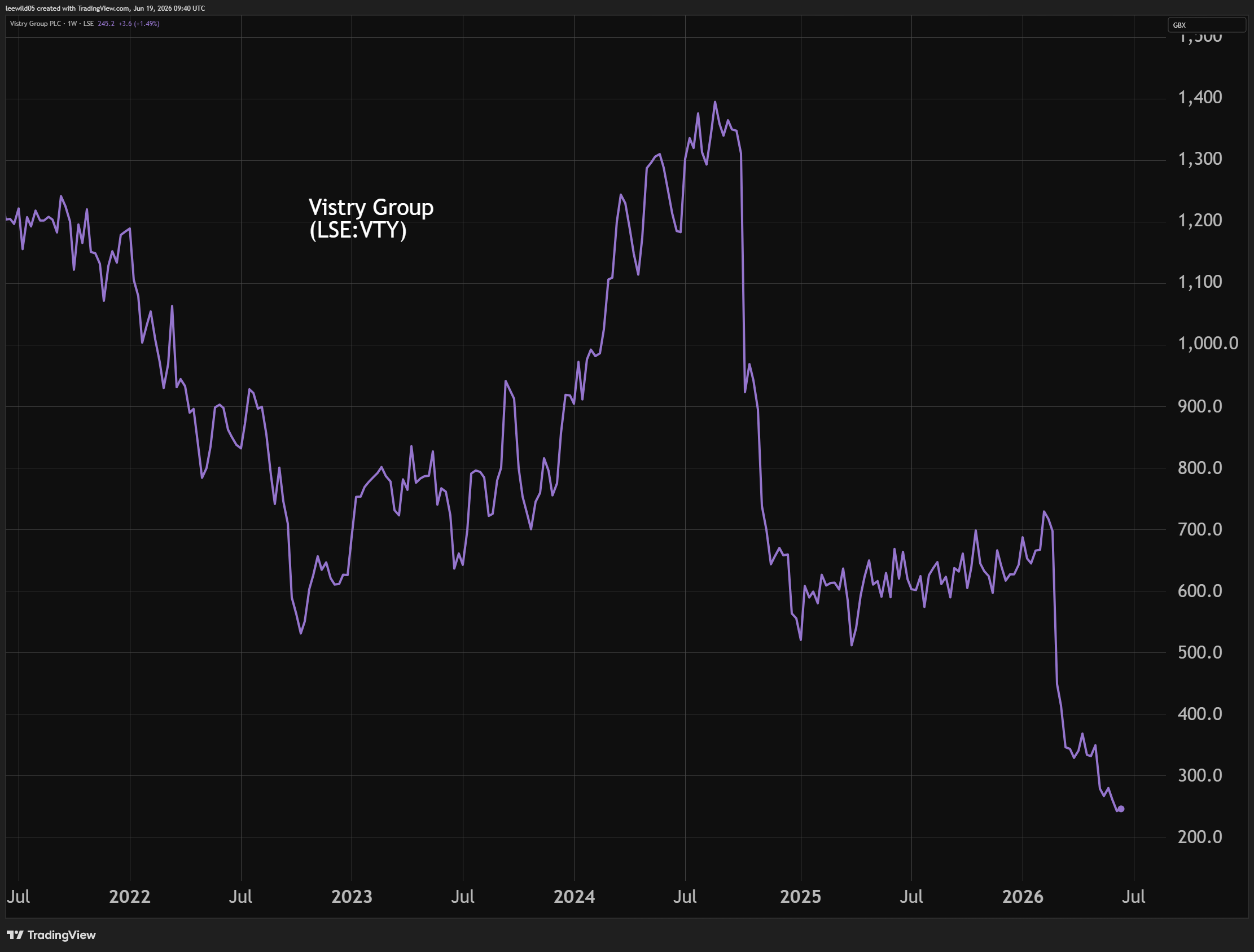

Yet I notice, in the short term at least, that Vistry Group (LSE:VTY) is overall improving from an all-time low of 220p on Tuesday to 248p, maybe because a heavy short position is sensitive to a net improvement in the mortgage rate outlook.

- Invest with ii: Top UK Shares | How to Start Trading Stocks | Open a Trading Account

Recent sentiment had shifted to negative, helping create the share price low, then came the US/Iran memorandum of understanding (MOU). UK inflation surprisingly held steady at 2.8% and the Bank of England left interest rates on hold at 3.75%.

Source: TradingView. Past performance is not a guide to future performance.

Vistry is the second most-shorted London share with 14.7% of the issued share capital out on loan, and that’s just disclosures over 0.5%; the real figure likely higher.

Such a crowded trade in an £800 million mid-cap is either going to be proven right by deteriorating fundamentals – necessitating a dilutive share issue, which I suspect is the down-bet – or there is potentially the mother of all short squeezes here.

Caveat: Vistry is a difficult speculative call

It is a fascinating test whether to trust the 2025 annual accounts that imply the company should manage through, or the short book that has soared from 1.0% in early March.

In particular, the market is concerned about true cash generation given the company has had to cut prices aggressively to achieve sales. A new CEO was appointed two months ago after the executive chair, Greg Fitzgerald, suddenly announced his retirement on 4 March with the 2025 results.

Fitzgerald had been CEO of Vistry’s predecessor, Bovis Homes, from 2017, and some investors bought into Vistry quite in awe. But a combined CEO/chair role risks over-concentration of power, and governance issues emerged when Vistry’s South division had severe internal issues prompting profit downgrades.

- How to build a World Cup-winning portfolio

- Stockwatch: why US/Iran deal looks a boon for growth

- DIY Investor Diary: how I mix tech and dividends

The current CEO led Vistry’s Yorkshire, North Midlands and West operations having joined Countryside Partnerships in 2016, which Vistry acquired in 2022. His current aims are to improve cash generation and reduce inventory levels, although exactly how serious the downturn is that he’s responding to is unclear.

Bears cite a progression in stress indicators. From October 2023, Vistry required a 10% price cut from subcontractors and suppliers as it shifted towards a “partnerships” model. While its 2023 numbers showed a 33% advance in net profit to £215 million, strains were possibly manifesting already given a subsequent drop to £74.5 million:

Vistry Group - financial summary

year-end 31 Dec

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| Turnover (£ million) | 1,055 | 1,028 | 1,061 | 1,131 | 1,812 | 2,407 | 2,729 | 3,564 | 3,779 | 3,614 |

| Operating margin (%) | 15.2 | 11.8 | 16.4 | 15.8 | 5.1 | 11.9 | 7.8 | 7.9 | 3.7 | 5.9 |

| Operating profit (£m) | 160 | 121 | 174 | 179 | 91.7 | 285 | 212 | 281 | 138 | 215 |

| Net profit (£m) | 121 | 91.3 | 137 | 138 | 76.8 | 254 | 204 | 215 | 74.5 | 138 |

| EPS - reported (p) | 84.2 | 63.5 | 95.0 | 97.7 | 34.7 | 114 | 86.3 | 61.3 | 21.8 | 42.0 |

| EPS - normalised (p) | 84.2 | 67.3 | 94.7 | 107 | 43.1 | 118 | 143 | 72.1 | 46.5 | 45.9 |

| Operating cashflow/share (p) | 43.1 | 109 | 90.9 | 153 | 82.2 | 119 | 29.9 | -20.6 | 40.7 | 56.5 |

| Capital expenditure/share (p) | 1.2 | 1.0 | 1.3 | 0.4 | 1.2 | 0.7 | 0.7 | 0.8 | 2.0 | 3.4 |

| Free cashflow/share (p) | 41.9 | 108 | 89.6 | 153 | 81.0 | 118 | 23.2 | 21.4 | 38.7 | 53.1 |

| Dividends per share (p) | 42.1 | 44.4 | 53.3 | 19.2 | 20.0 | 60.0 | 55.0 | 0.0 | 0.0 | 0.0 |

| Covered by earnings (x) | 2.0 | 1.4 | 1.8 | 5.1 | 1.7 | 1.9 | 1.6 | 0.0 | 0.0 | 0.0 |

| Return on total capital (%) | 13.5 | 10.3 | 13.6 | 12.7 | 3.4 | 10.0 | 4.8 | 6.3 | 3.1 | 4.6 |

| Cash (£m) | 38.6 | 170 | 163 | 362 | 341 | 399 | 677 | 418 | 320 | 354 |

| Net debt (£m) | -38.6 | -145 | -127 | -339 | 4.3 | -201 | -31.6 | 508 | 601 | 242 |

| Net assets (£m) | 1,016 | 1,057 | 1,061 | 1,272 | 2,195 | 2,391 | 3,250 | 3,304 | 3,236 | 3,325 |

| Net assets per share (p) | 727 | 756 | 760 | 828 | 988 | 1,075 | 940 | 956 | 977 | 1,038 |

Source: historic company REFS and company accounts.

I haven’t seen the research note, but analysis at RBC reportedly tracked over 1,200 Vistry homes listed from January to May eliciting big price cuts to achieve sales, which sounds like a dash for cash under stress. Ceding margin hardly squares with the end-2025 balance sheet showing £354 million cash.

A recent memo from the CEO to staff – offering enhanced redundancy packages – has ended up in the public domain, adding to unease over Vistry’s financial position.

There has been speculation about the risk of breaching banking covenants but unlike Crest Nicholson Holdings (LSE:CRST), there has been no such announcement.

Vistry’s end-2025 balance sheet showed the ratio of current assets to current liabilities at an ample 2.5x, while gross debt including leases was 18% of net assets or 7% based on net debt. For a debt/liquidity crisis, either the year-end figures were aggressively window-dressed or there has been a remarkably sudden downturn.

- FTSE 100 share tipped for 20% rally to record high

- Ian Cowie: how I’m investing in space

- Can the new boss fix this FTSE 100 struggler?

On a subtler level, some investors haven’t been able to swallow why Fitzgerald would suddenly leave if the business is sound. It can look like he wants to be out of the firing line if the situation is deteriorating beyond reasonable control.

He did, however, buy £893,000 worth of shares on 11 March at 407p, followed by the new non-executive chair – who has been a non-executive director since 2024 – buying £64,700 worth at 353p on 20 April.

For what consensus forecasts are worth, at 248p Vistry is on a 12-months’ forward price/earnings (PE) ratio of around 5x and, despite no dividend, the shares trade at a 64% discount to last December’s £2,168 million net tangible assets worth 682p per share. Chief assets were £3,229 million of inventories: note 9 clarified this as 60% land, 39% work in progress and 1% part-exchange properties.

Until 11 May, Vistry has also consistently bought back its shares, which could prove a far better return of capital than dividends if the market price has become unduly depressed. This also affirmed the cash position given that Vistry reported £354 million year-end cash versus £498 million debt (all long term) and £98 million leases;, which meant a net £51 million net finance charge relative to £223 million reported operating profit.

AGM trading update was a mixed affair

Guidance on 13 May was for significantly lower first-half profit due to actions to accelerate cash generation, albeit a similar second half to last year, implying a profit warning for 2026 as a whole. However, the range of forecasts behind consensus is a wide one. While average net debt is expected to be higher in the first half, it was guided to being significantly lower in the second.

I believe if the company was teetering towards financial distress, this update would have been terser.

An operational review is due to share findings no later than half-year results on 24 September and, given a thorough response to the late 2024 fiasco of the South division, should mean that any skeletons have been rattled.

Bears cite strategic risk with the partnerships model where long-term fixed-price contracts make it hard to pass on rising build costs. Instead, margins take a hit. Public funding for social and affordable housing has met with planning delays and under-funded councils.

- A challenging Q1 as expected, but Tesco juggernaut rolls on

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

- New state pension proposal highlights challenges for younger workers

Yet the board and new CEO remain “fully committed to the partnerships strategy and the key role our differentiated model can play in delivering the huge need for new housing across the country”. In theory, pre-selling mixed-tenure and affordable homes to local authorities, housing associations and institutional investors achieves a “capital-light” approach, with stage payments as construction advances, hence higher returns on capital benefiting cash flow.

Trust the financial statements or short book?

Implicitly, the extent of conviction among some hedge funds – eight of which have raised short bets in the last month versus four reducing – implies that Vistry either is not being fully frank about its financial position or misinterprets the extent of the UK housing downturn under way.

Even if management has kept a polite-as-possible face it doesn’t look to me as if debt is so serious unless a downturn compromises covenants. The extent of discount to assets qualifies the shares for a deep-value Benjamin Graham “bargain” investment screen. But beware, the criteria is relatively narrow and this 20th-century dean of value investing countenanced diversification among such shares.

Vistry made a first-half trading statement on 10 July 2025, hence this year’s will be axiomatic. Hedge funds are positioning around, but unless something dire has happened in the last month, the essential tenor came on 13 May.

It is a speculative high-risk/reward stance, but I believe probability tilts to the shares rating as a “buy”, aided by a crowded short trade. As ever with uncertain situations, averaging in can be wise.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.