Stockwatch: this turnaround share could march higher

Life on the stock market has been difficult for this iconic brand, but analyst Edmond Jackson sees improvements and believes a multi-year share price uptrend is possible.

9th June 2026 10:49

by Edmond Jackson from interactive investor

Footwear group Dr. Martens Ordinary Shares (LSE:DOCS) can make me feel like I’m missing out.

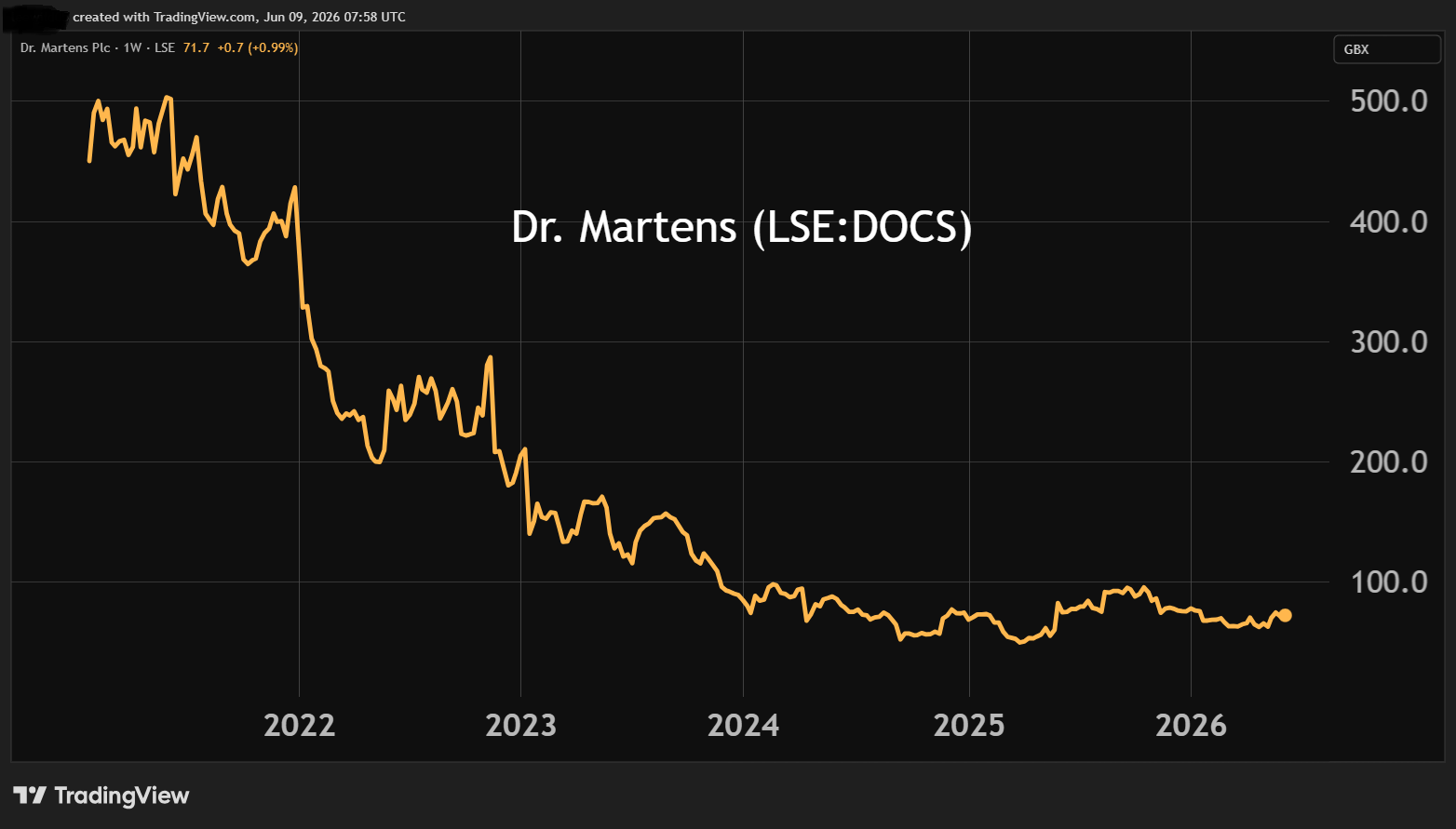

Since the annual results to 29 March were released on 19 May, its mid-cap shares have rallied from 66p to 74p (currently 71p).

The long-term chart starts to look like a “bowl” pattern manifesting after a long descent from a euphoric 450p high in 2021 after the shares listed at 370p.

- Our Services: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

Source: TradingView. Past performance is not a guide to future performance.

Assuming consensus forecasts, the March 2027 price/earnings (PE) ratio is near 15x, easing below 12x assuming net profit advances 109% to £49.7 million this year, then £60.3 million to March 2028. This would still be well below the £181 million and £129 million achieved in 2022 and 2023 respectively, hence scope to cut the PE and genuinely re-rate the shares if a more vigorous mean-reversion of profit is feasible.

As yet the dividend is being held at around 2.55p per share after a near halving from 5.84p in respect of the March 2023 year. With around two times earnings cover and plenty more in terms of free cash flow, this equates to a 3.5% yield.

Ije Nwokorie, CEO since January 2025, appears to be implementing a classic turnaround, with efficiency improvements and new strategy better attuned to customers. But I find it harder to judge the demand profile for this iconic design of footwear in a tough consumer environment.

Dr Martens is best known for its iconic eight-eye 1460 boot, yet the modern range extends to a variety of boots, chunky platform sandals, formal brogues, loafers and industrial slip-resistant workwear.

- Iran war 100 days: how stocks and markets have performed

- 10 hottest ISA shares, funds and trusts: week ended 5 June 2026

Quality seems a mixed bag relative to decades ago before outsourcing to Asia took place from 2003. For what Trustpilot reviews are worth, Dr Martens rates 2.6 out of 5.0 – “poor” – with reviews polarising between 1 star and 5 star, often relating to quality and customer service.

While any business has a portion of dissatisfied customers liable to vent online, they should be well outweighed by the positives. Management implicitly acknowledges the criticism by way of retaining a premium, hand-crafted “Made in England” collection produced at its original Wollaston, Northamptonshire, factory.

This [makes] sense as a “conviction buy” for me, but I am willing to let the evolving numbers talk.

Pivoting towards a ‘consumer-first’ operating model

There is an implied shift from “channel-first” led by retail outlets, to one of engaging customers and understanding their needs online, continuing to diversify items, and working with fewer and better wholesale partners alongside e-commerce.

This derives from when the current CEO became Dr Martens’ chief brand officer in 2024, with responsibility for implementing the strategy, having spent 11 years at the Wolff Olins global brand consultancy before being a senior director at Apple.

“Consumer-first” can sound like conceptual jargon for essential marketing realities, but its aim is to improve revenue quality by giving customers more reasons to buy. Dr Martens obviously has a distinctive brand image, although I find it hard to guesstimate the extent of appeal and of which products.

Shoes are a stand-out in the annual results: revenue was up 19%, aided by a wide range of items including new ones such as Buzz and Lowell, together with iconic styles, hence an improvement from 26% to 31% of group revenue.

Boots, however, declined from 57% to 52% of group revenue, which is concerning. In the main US market – more than a third of group revenue – “full-price” boots grew in all quarters expect the fourth, and taller boots are experiencing success.

Sandals also saw an 11% decline to 11% of group revenue, said to be due to a lack of new products which will not manifest until 2027.

Bags and accessories rose 15% but are currently only 6% of group revenue.

- Stockwatch: a blue-chip with long-term recovery potential

- Share Sleuth: the firm I’ve bought again despite a pricey valuation

Product performance is thus mixed, and boots may need to improve for the shares to sustain any uptrend. Overall revenue has slipped 1.4% to £765 million at constant currency. The Americas performed best with direct-to-consumer up 14%, but wholesale was near flat. Europe, the Middle East and Africa conversely saw wholesale up 7.6%, but full price direct-to-consumer fell 13%. Asia was broadly flat.

So, there looks to be plenty of scope for complex marketing within the current financial year’s goal to “scale higher-quality revenues via brand investment and improved retail strategy”.

Re-honing the financial base for further upside?

Nwokorie has raised the reported operating margin to 7.5% from 4.7% versus 25.2% and 17.6% in the March 2022 and 2023 financial years respectively. This can look as if further recovery is possible, although the results do not provide medium-term margin objectives.

Net bank debt has reduced 25% to £69.4 million but the income statement shows net interest costs took a lumpy 43% of £57 million operating profit. This relates to £144 million leases, so unless they are restructured the cost of higher interest rates linked to inflation could check any profits recovery – relative to a 61% rebound in adjusted pre-tax profit to £55.0 million to March 2026.

Dr Martens - financial summary

Year end 29 March

| 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 | |

| Turnover (£ million) | 349 | 454 | 672 | 773 | 908 | 1,000 | 877 | 788 | 765 |

| Operating margin (%) | 11.5 | 15.0 | 21.2 | 14.6 | 25.2 | 17.6 | 13.9 | 4.7 | 7.5 |

| Operating profit (£m) | 40.2 | 68.0 | 143 | 113 | 229 | 176 | 122 | 37.0 | 57.0 |

| Net profit (£m) | -5.7 | 17.2 | 74.8 | 35.7 | 181 | 129 | 69.2 | 4.5 | 23.8 |

| EPS - reported (p) | -0.6 | 1.7 | 7.5 | 3.6 | 18.1 | 12.9 | 7.0 | 0.5 | 2.4 |

| EPS - normalised (p) | -0.4 | 2.1 | 8.4 | 7.7 | 18.1 | 13.2 | 7.0 | 3.9 | 5.4 |

| Operating cashflow/share (p) | 4.6 | 5.6 | 12.1 | 16.0 | 18.4 | 7.7 | 17.0 | 20.2 | 14.6 |

| Capital expenditure/share (p) | 1.6 | 1.7 | 2.2 | 1.9 | 2.5 | 5.1 | 2.9 | 1.9 | 1.2 |

| Free cashflow/share (p) | 3.0 | 3.9 | 9.9 | 14.1 | 15.9 | 2.6 | 14.1 | 18.3 | 13.4 |

| Dividends per share (p) | 0.0 | 0.0 | 0.0 | 0.0 | 5.5 | 5.8 | 2.6 | 2.6 | 2.6 |

| Covered by earnings (x) | 0.0 | 0.0 | 0.0 | 0.0 | 3.3 | 2.2 | 2.8 | 0.2 | 1.0 |

| Return on total capital (%) | 10.3 | 17.6 | 27.1 | 22.5 | 32.6 | 21.3 | 15.3 | 5.1 | 8.0 |

| Cash (£m) | 86.4 | 58.4 | 117 | 114 | 228 | 158 | 111 | 156 | 180 |

| Net debt (£m) | 334 | 332 | 378 | 253 | 166 | 294 | 358 | 246 | 211 |

| Net assets (£m) | -29.4 | -8.4 | 70.5 | 151 | 328 | 404 | 368 | 366 | 362 |

| Net assets per share (p) | -2.9 | -0.8 | 7.1 | 15.1 | 32.8 | 40.4 | 38.3 | 38.0 | 37.8 |

Source: prospectus and company accounts.

Consumer impact of higher inflation and rates

It is a crux question for investing in any retail-related share currently, perhaps more so regarding a turnaround situation. Nwokorie says the current financial year involves the “scale” phase of the strategy, hence the context needs to be reasonably benign.

Are we in a “calm before the storm” moment leading to significant demand erosion for retailers, not just a threat to operating costs? Or are consensus forecasts over-cautious given that retailers are significantly hedged against energy costs and have mitigated supply chain disruption risks?

Last week, Dr Martens shares eased alongside market concerns about how a settlement to the US/Iran war remains elusive, although frankly the market seems increasingly de-sensitised to the Middle East and assumes that a peace deal will eventually be reached.

Two hedge funds go short

GLG Partners and Tages Capital edged over the 0.5% (of issued share capital) disclosure threshold for short positions from late April. Given that this is a near £700 million company it is possible they have been short some while rather than this offering being a current verdict on prospects. There had otherwise been a 0% disclosed position since May 2025.

When a bear trend intensified from 2023, GLG was active with up to 1.1% shorted, hence it does have a good record of making good calls. It is short on some 30 UK shares such as Kingfisher (LSE:KGF), Sainsbury (J) (LSE:SBRY) and B&M European Value Retail (LSE:BME), so is probably using UK retail as a means to hedge its overall equity exposure.

While private equity group Primera reportedly made £1.3 billion from DM’s flotation and may have retained a circa 38% stake “for free”, it slightly increased this to 38.4% in June 2025. Other institutional shareholders have traded mixed in recent months.

The story here is tempting in terms of a “new-broom CEO” honing efficiencies, although it’s unclear what extent of delivery the macro context will allow. There is also uncertainty as to the scale of marketing success and demand from the second half of this year. With that in mind, it is also unclear whether the shares have assuredly marked an all-time low, but the company’s past profit performance implies decent prospects for recovery. So, I believe a multi-year share price uptrend is possible.

I therefore rate Dr Martens a modest “buy” at 71p for continued initiatives fuelling a turnaround, although I lack the conviction to rank the shares a core holding.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.