Share Sleuth: the firm I’ve bought again despite a pricey valuation

Richard Beddard explains why he invested in the company he did after the Decision Engine suggested six potential trades.

5th June 2026 15:01

by Richard Beddard from interactive investor

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

After the reduction of Share Sleuth’s Renishaw (LSE:RSW) holding last month and dividends paid, the portfolio’s cash balance was £9,262 on 28 May, the day when I considered this month’s trade.

That was more than enough to add a new holding, or increase an existing one. The minimum trade size, set at 2.5% of the portfolio’s total value, was just shy of £5,550.

- Invest with ii: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

Additions

The Decision Engine covers 30 shares. Twenty-four were already Share Sleuth members. The other six were potential new additions.

This month, the Decision Engine only offered the six new additions as potential trades. Existing portfolio members were all near their ideal sizes (as determined by their scores) and therefore not eligible.

Adding a new share is a big step. Although I’ve scored the share, I haven’t seen fit to invest in it. Other, often more familiar, options have always seemed better.

| # | company | description | score | qual | price | ih% | ss% | ih%-% |

| 6 | Auto Trader | Online marketplace for motor vehicles | 7.9 | 7.0 | 0.9 | 5.9% | 5.9% | |

| 11 | Judges Scientific | Manufactures scientific instruments | 7.5 | 7.0 | 0.5 | 5.1% | 5.1% | |

| 12 | Cake Box | Cake shop franchise and sweet manufacturer | 7.2 | 7.0 | 0.2 | 4.3% | 4.3% | |

| 19 | YouGov | Surveys public opinion and conducts market research online | 6.9 | 6.0 | 0.9 | 3.9% | 3.9% | |

| 24 | Keystone Law | Operates a network of self-employed lawyers | 6.4 | 6.5 | -0.1 | 2.7% | 2.7% | |

| 28 | Tristel | Manufactures hospital disinfectant | 6.1 | 8.0 | -1.9 | 2.5% | 2.5% |

Click on a share’s score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio, ss% is the actual size of Share Sleuth’s holding, and ih%-% is the difference between ideal and actual sizes.

There is a technical reason why I didn’t add the three highest-ranked shares available this month, and Keystone Law Group Ordinary Shares (LSE:KEYS), which was fifth in the pecking order.

Judges Scientific (LSE:JDG) and Keystone Law have published annual reports and will be among the next companies I re-score. Autotrader Group (LSE:AUTO) has published full-year results and should publish its annual report later this month. I’ll be rescoring it shortly as well.

I should have re-scored Auto Trader already, because I promised to earlier this year during the “SaaSpocalypse”. Then there was a sell-off in software and data businesses.

Auto Trader is the dominant UK second-hand car marketplace. It owns a massive silo of real-time data, which it uses to provide unparalleled services to car buyers and sellers.

As far as Auto Trader is concerned, there’s a growing belief that buyers might turn to AI to search for car deals, and dealers might use AI to promote their inventory directly into chatbots and search engines.

- Don’t write off UK stocks: two undervalued FTSE 100 shares

- Don’t miss the next big IPO: get the latest IPO news and updates straight to your inbox

- AIM market takeovers boom plus 3 potential targets

Many buyers look to Auto Trader for advice, and it seems likely that some are already turning to chatbots. Over time, this may weaken the allure of the brand and the number of people engaging with the platform.

There is a contrarian belief, famously championed by UK fund manager Nick Train, that the proprietary data of companies such as Auto Trader will remain irreproducible and AI will enable companies like Auto Trader to get more value out of it.

I need to give Auto Trader my full attention, so I’ve chosen to wait until I score it properly. In the meantime, I have belatedly updated my scoresheet to include AI risk, and that has introduced more uncertainty. Erring on the side of caution, I have reduced its score by half a point.

| Auto Trader | AUTO | Online marketplace for motor vehicles | 29/05/2026 | 7.4/10 |

| How capably has Auto Trader made money? | 3.0 | |||

| Auto Trader has grown revenue and profit at about 10% CAGR over the last decade by selling advertising subscriptions to car dealers and additional packages to generate, promote and price listings. As the biggest classified site by far, powerful network effects pull in buyers and dealers. | ||||

| How big are the risks? | 1.5 | |||

| Because Auto Trader is dominant it is not clear to me how much potential there is for growth. Retailers have new competitors: manufacturers, leasing companies, and leasing comparison sites. AI may allow buyers and sellers to bypass the marketplace. | ||||

| How fair and coherent is its strategy? | 2.0 | |||

| Auto Trader’s strategy is to bring more of the deal process online. but the poor reception of Deal Builder shows dealers are questioning whether it is adding enough value to justify price increases. The app is highly rated, and employees are motivated and loyal. | ||||

| How low (high) is the share price compared to normalised profit? | 0.9 | |||

| Low. A share price of 427p values the enterprise at £3,460 million, about 12 times normalised profit. | ||||

| NB: Bold text indicates factors that reduce the score. Bold and italicised text doubly so. The maximum score is 3 for each criterion except price, which has a maximum of 1 (explained here) | ||||

I previously scored Auto Trader last December.

Cake Box Holdings Ordinary Shares (LSE:CBOX) was also past the end of its financial year. It will be publishing its full-year results this month and published a broadly positive trading update last week. The latest results will include a full year of Indian sweet maker Ambala, which the company acquired a year ago.

Ambala was a substantial acquisition and a different kind of business. It is a manufacturer and Cake Box is a supplier of ingredients and recipes to its franchisees.

Due to increased complexity and the debt taken on by Cake Box, I decided to score the new entity before committing to it. Re-scoring will be triggered by the publication of the annual report, probably in August.

Having delayed decisions on four of the shares, I was left considering the two lowest scoring of the available shares. They will not publish annual reports until November.

That is fine. In my judgement, all Decision Engine shares are good long-term investments. The Decision Engine guides me to lower holding sizes for lower-scoring shares, but doesn’t stop me holding them.

- My 10-point checklist for picking smaller company shares

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

- Five AIM shares trading at a discount

As I wrote when I last scored them, Tristel (LSE:TSTL) and YouGov (LSE:YOU) are both management merry-go-rounds.

YouGov is a whole bundle of risks (which, in addition to management, include AI and dubious acquisitions), compensated for by a very low share price.

Tristel is a much more stable situation. It has a unique product and a large market to grow into, but the shares are pricey. I know Tristel much better since it was a portfolio member between November 2012 and January 2025.

The company is searching for a new chief executive only two years after Matt Sassone replaced its founder. But it is still performing well. He may just have got an offer he couldn’t refuse.

| Tristel | TSTL | Manufactures hospital disinfectant | 29/05/2026 | 6.1/10 |

| How capably has Tristel made money? | 2.5 | |||

| Tristel has achieved double-digit profit growth for over a decade by developing unique disinfectants and introducing them into new geographical markets. It is highly profitable and cash generative. The company’s founder retired in September 2024. The CFO retired in June. The new CEO has also received a better offer. | ||||

| How big are the risks? | 2.5 | |||

| Unique, prosperous, and financially strong, there are few obvious risks, apart from the fact that it needs a settled board. Trio, Tristel’s primary product, uses pre-wetted wipes strengthened with plastic. To meet environmental targets, customers and Tristel would almost certainly prefer it to be plastic free. | ||||

| How fair and coherent is its strategy? | 3.0 | |||

| Although the company has mooted acquisitions, it is focused on exploiting its unique IP by doing what it has done in the past: protecting and improving its products and rolling them out worldwide. Tristel makes hospitals safer and rewards employees, particularly its executives. | ||||

| How low (high) is the share price compared to normalised profit? | -1.9 | |||

| High. A share price of 373p values the enterprise at £177 million, about 29 times normalised profit. | ||||

| NB: Bold text indicates factors that reduce the score. Bold and italicised text doubly so. The maximum score is 3 for each criterion except price, which has a maximum of 1 (explained here) | ||||

I last scored Tristel in February.

When I liquidated Share Sleuth’s Tristel holding I wrote that “It pained me to liquidate Tristel...But the price is high, and the score, which I updated in December, precludes me from adding to the holding.”

Last week, the price was a little lower and I could add a holding at the minimum size of 2.5% of the portfolio’s total value.

Share Sleuth owned Tristel continuously between November 2012 and January 2025. The sale price in November 2025 was 420p.

Reductions

The Decision Engine also nudged me to reduce some of Share Sleuth’s holdings.

| Reductions, 28/05/2026 | ||||||||

| # | company | description | score | qual | price | ih% | ss% | ih%-% |

| 15 | Oxford Instruments | Makes imaging and semiconductor manufacturing systems | 7.0 | 6.5 | 0.5 | 4.1% | 7.0% | -3.0% |

| 21 | Games Workshop | Designs, makes and distributes Warhammer. Licences IP | 6.7 | 8.5 | -1.8 | 3.5% | 6.0% | -2.5% |

| 26 | Cohort | Manufactures/supplies defence tech, training, consultancy | 6.2 | 8.0 | -1.8 | 2.5% | 5.1% | -2.6% |

| 27 | Bloomsbury Publishing | Publishes books and educational resources | 6.2 | 7.5 | -1.3 | 2.5% | 5.5% | -3.0% |

Click on a share’s score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio, ss% is the actual size of Share Sleuth’s holding, and ih%-% is the difference between ideal and actual sizes.

I chose not to remove Bloomsbury Publishing (LSE:BMY) and Cohort (LSE:CHRT)last month, and I’m unaware of any developments since. Games Workshop Group (LSE:GAW) was a marginal trade, the difference between its ideal holding size and the actual holding size was 2.5% of the portfolio’s total value - the minimum trade size.

Oxford Instruments (LSE:OXIG) surprised me in a pleasant way. Its price has gone up steadily this year, and it has emerged as one of the most oversized Share Sleuth holdings.

The discrepancy between ideal and actual holding sizes remained relatively modest (3%), Share Sleuth didn’t need cash to fund an addition, and Oxford Instruments is another company publishing an annual report soon.

I was happy to sit on a winner for a while.

Trade

On Friday 29 May, I added 1,432 shares in Tristel.

The actual price, quoted by a broker, was 3.84p. The trade cost £5,501 after deducting £10 in lieu of fees.

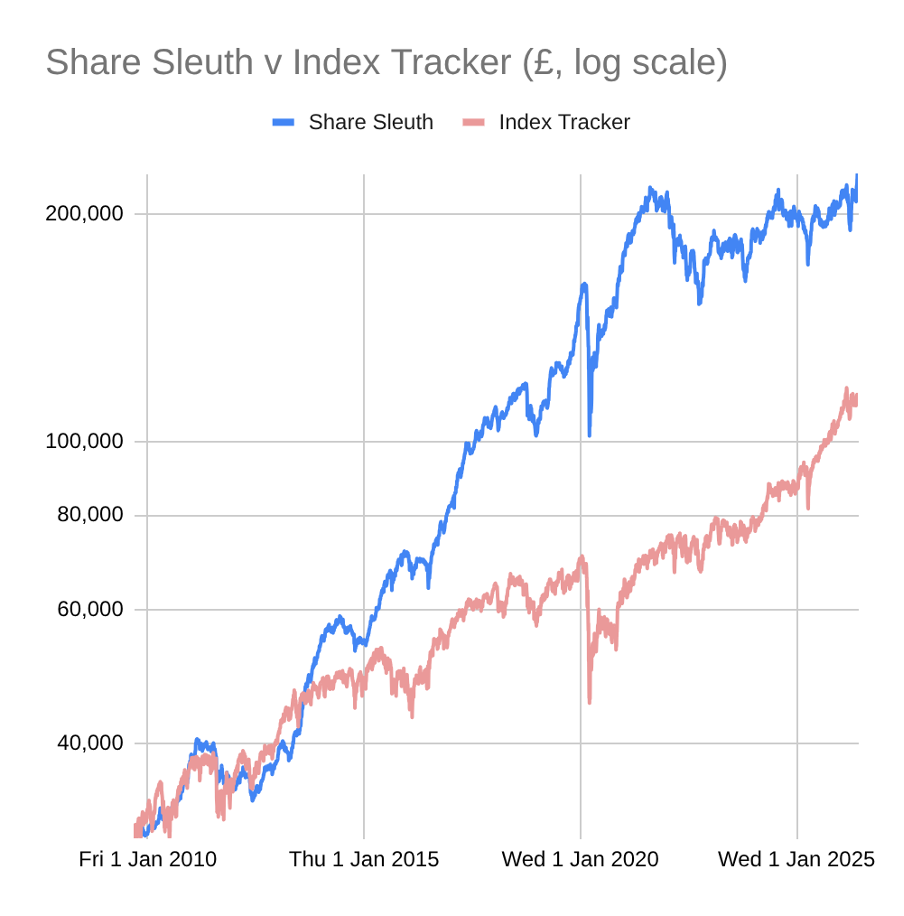

Share Sleuth performance

At the close on Tuesday 2 June, Share Sleuth was worth £222,249, 641% more than the £30,000 of pretend money we started with in September 2009.

The same amount invested in accumulation units of a FTSE All-Share index tracking fund would be worth £113,974, an increase of 280%.

Past performance is not a guide to future performance.

After the trade and dividends paid by 4imprint Group (LSE:FOUR), Games Workshop, Howden Joinery Group (LSE:HWDN), and Softcat (LSE:SCT), Share Sleuth’s cash pile is £3,892.

The minimum trade size, 2.5% of the portfolio’s value, was £5,556.

| Share Sleuth, 02 Jun 2026 | Cost (£) | Value (£) | Return (%) | ||

| Cash (2% of portfolio) | 3,892 | ||||

| Current holdings (25 shares) | 218,357 | ||||

| Total, and performance since 9 September 2009 | 30,000 | 222,249 | 641 | ||

| Benchmark: FTSE All-Share index tracker (acc) | 30,000 | 113,974 | 280 | ||

| Companies | Shares | Cost (£) | Value (£) | Return (%) | |

| AMS | Advanced Medical Solutions | 1,965 | 4,503 | 4,205 | -7 |

| ANP | Anpario | 1,124 | 4,057 | 6,216 | 53 |

| BMY | Bloomsbury | 1,882 | 8,354 | 12,214 | 46 |

| BNZL | Bunzl | 417 | 9,798 | 9,516 | -3 |

| BOWL | Hollywood Bowl | 4,002 | 10,348 | 11,406 | 10 |

| CHH | Churchill China | 1,495 | 17,228 | 5,083 | -70 |

| CHRT | Cohort | 836 | 6,315 | 10,701 | 69 |

| FAN | Volution | 830 | 5,151 | 5,030 | -2 |

| FOUR | 4Imprint | 116 | 2,251 | 4,338 | 93 |

| GAW | Games Workshop | 66 | 4,116 | 12,929 | 214 |

| GDWN | Goodwin | 36 | 871 | 5,357 | 515 |

| HWDN | Howden Joinery | 1,476 | 10,371 | 11,144 | 7 |

| JET2 | Jet2 | 822 | 5,211 | 10,259 | 97 |

| LTHM | James Latham | 1,150 | 14,437 | 11,500 | -20 |

| MACF | Macfarlane | 7,689 | 10,011 | 4,967 | -50 |

| OXIG | Oxford Instruments | 505 | 10,044 | 16,322 | 63 |

| PRV | Porvair | 906 | 4,999 | 7,556 | 51 |

| QTX | Quartix | 1,618 | 3,988 | 4,328 | 9 |

| RNWH | Renew Holdings | 1,310 | 9,804 | 11,502 | 17 |

| RSW | Renishaw | 117 | 3,698 | 6,353 | 72 |

| SCT | Softcat | 675 | 9,995 | 12,508 | 25 |

| SOLI | Solid State | 5,009 | 6,033 | 9,768 | 62 |

| TFW | Thorpe (F W) | 6,153 | 14,861 | 15,690 | 6 |

| TSTL | Tristel | 1,432 | 5,509 | 5,477 | -1 |

| TUNE | Focusrite | 2,020 | 14,128 | 3,990 | -72 |

Notes

Costs include £10 broker fee, and 0.5% stamp duty where appropriate

Cash earns no interest

Dividends and sale proceeds are credited to the cash balance

Objective: To beat the index tracking fund handsomely over five year periods

Source: ShareScope.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns all the shares in the Share Sleuth portfolio except Tristel (he cannot trade a share on his own account within a week of publication of an article about a share).

For more on the Decision Engine and Share Sleuth, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.