Stockwatch: a major inflection point for these two shares?

Analyst Edmond Jackson mulls share price spikes and short-seller activity at two cyclical buying opportunities.

14th July 2026 12:25

by Edmond Jackson from interactive investor

Here is another example of how short selling bakes in share price rebounds without needing firmly positive news, enabling me to update a 19 May piece examining recruiters.

- Our Services: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

Last Friday (10 July), mid-cap Hays (LSE:HAS) jumped 20% to 43p, which may seem surprising given that its fiscal fourth quarter to 30 June hardly conveyed vigour. The pace of reduction in net fee income slowed to 4% (5% like-for-like) from 7% (8% like-for-like) in January to March. But helped by an efficiency programme under a new CEO (Hays’ former chief digital and technology officer rather than a fresh outsider), pre-exceptional operating profit is guided to the top end of a previous wide range of £37 million to £45 million, which is good.

It is similar to small-cap polymer manufacturer Victrex (LSE:VCT), examined last Friday, which has had to serially downgrade forecasts, thus attracted short selling, with it only taking a broadly “in line” update for the shares to jump 20% in response.

Short selling is creating various coiled springs and, instead of complaining about shorters, I say look out for what they might imply about risk and recognise that they can get things wrong and capitalise on this.

Data shows that from 11 June, and especially up to 8 July, four hedge funds over the 0.5% (of issued share capital) disclosure threshold sold further just before this re-rate. Perhaps they thought net fee income would continue to fall, and yes, there remains a worst-case scenario where it could fall if Middle East hostilities and difficulties in the Strait of Hormuz prove chronic. But when a share is actively shorted the chances rise, and all it might need is a reduction in the rate of any underlying downturn for the market to sense a ‘short squeeze’ (when a share price is rising rather than falling, there can be a rush from hedge fund investors to close out their positions. Some are automatically forced to sell, with the share price being driven higher.)

Illustrating how short sellers might not be feared, Citadel Advisors LLC very slightly raised its short to 0.70% of Hays on 1 July, since when the shares have risen 30%. For Victrex, it raised from 0.50% on 19 June to 0.60% on 6 July before a 7 July trading update boosted the shares 20%. Citadel appeared to realise a mistake in Victrex and trimmed to 0.57% that day.

In fairness, such trades in Hays could still be in profit despite this near-term mistake. Yet despite 12% dilution to shore up the balance sheet in response to Covid, the current price area is tantalising on a technical view, looking as if a low was put in from March to June. Even amid the 2008 crisis, Hays was only briefly below 50p, likewise in late 2011 when markets sold off amid a eurozone debt panic.

Source: TradingView. Past performance is not a guide to future performance.

PE multiples remain high on a short to medium-term view

Near 1.6 billion shares in issue means a consensus expectation of barely 1.1p earnings per share (EPS) in respect of the June 2026 year despite £17.5 million net profit. This is to rise over 1.8p based on £28.3 million profit to June 2027, still well below normalised EPS of 9.3p in 2022 and 8.5p in 2023 (see table).

If realised when Hays reports prelims on 20 August, then around 49p currently (up another 14% yesterday) it implies a trailing price/earnings (PE) of 45x easing to 27x on a 12-month forward view. That can appear as if risking over-valuation if Hays is chiefly cutting costs to cope with a diminished earnings scenario rather than a genuine cyclical upturn ahead. Time will tell whether artificial intelligence (AI) is supplanting enough employee roles that Hays could fill, and clients being more inclined to use LinkedIn than an agency. But if recruitment sees much recovery on a two- to five-year view, the PE could be in mid-single digits.

- Valuable lessons learned from my 2026 share tip performance

- Insider: bosses buy two small-caps cheaply

- Stockwatch: a turnaround play for both capital upside and yield

Yield support is modest given that consensus for trailing dividend per share (DPS) of 0.45p implies barely 1.0% with 2.4x earnings cover and historically often strong cash flow, with this rising to 1.6% if 0.8p DPS is achieved 12 months hence.

I recognised this on 19 May when I suggested taking a starter position and seeing what evolves, given that the new CEO had bought £147,300 worth at 30.3p on 14 May after £147,200 worth at 38.6p on 2 March and £96,200 worth at 56.6p on 1 October 2015. Four other Hays’ directors had also bought small lots lately.

Hays - financial summary

Year end 30 Jun

| 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| Turnover (£ million) | 5,930 | 5,648 | 6,589 | 7,583 | 6,949 | 6,607 |

| Operating profit (£m) | 95.1 | 95.1 | 210 | 197 | 25.1 | 14.9 |

| Net profit (£m) | 47.5 | 61.5 | 154 | 138 | -4.9 | -7.8 |

| Operating margin (%) | 1.6 | 1.7 | 3.2 | 2.6 | 0.4 | 0.2 |

| Reported earnings/share (p) | 3.1 | 3.6 | 9.1 | 8.5 | -0.3 | -0.5 |

| Normalised earnings/share (p) | 5.7 | 3.4 | 9.3 | 8.5 | 1.4 | -0.4 |

| Operational cashflow/share (p) | 23.1 | 0.4 | 10.1 | 10.2 | 6.0 | 6.9 |

| Capital expenditure/share (p) | 1.7 | 1.1 | 1.4 | 1.8 | 1.5 | 1.4 |

| Free cashflow/share (p) | 21.4 | -0.7 | 8.7 | 8.4 | 4.5 | 5.5 |

| Dividend per share (p) | 0.0 | 1.2 | 2.9 | 3.0 | 3.0 | 1.2 |

| Earnings cover (x) | 0.0 | 3.0 | 3.2 | 2.8 | -0.1 | -0.4 |

| Return on total capital (%) | 9.0 | 9.1 | 21.9 | 23.3 | 3.3 | 2.1 |

| Cash (£m) | 485 | 411 | 296 | 146 | 161 | 169 |

| Net debt (£m) | -256 | -209 | -111 | 54.2 | 123 | 144 |

| Net assets (£m) | 853 | 872 | 796 | 670 | 558 | 467 |

| Net assets per share (p) | 50.9 | 52.0 | 48.2 | 42.2 | 35.2 | 29.3 |

Source: company accounts.

What could be the worst-case scenario to vindicate shorting?

I have made the point with builders and their suppliers that we see keen short selling, but unless a worst-case scenario materialises, such companies may only need to muddle through making productivity improvements for these trades to close out and benefit contrarian long positions (and enjoying dividends in the meantime).

Hays teases with the prospect of an update in the 20 August prelims on shaping “a more competitive operating model” as if margin can recover materially from 0.2%, where it was only around 3% in 2022 and 2023, achieving EPS of around 9p.

Global recession would be the bugbear if energy disruption and higher commodity prices conflate with diminished reserves since March. As yet, financial markets assume that renewed conflict in the Middle East will not last despite a clear stand-off on the Strait of Hormuz and US President Donald Trump mouthing a 20% tariff on all goods to pay for the US keeping it open. The sense is that there’s no US appetite to get dragged back into a regional quagmire.

The risk, however, is reprisals dragging on, with Iran in a strong position geographically to threaten shipping disruption, hence insurers withdraw cover. The US aims to “continue degrading Iran’s ability to attack civilian mariners and commercial ships” and success would be positive for the wider economy, but it raises the likelihood of ongoing attacks by Iran on its neighbours and reduces scope for a peace settlement.

Despite Hays’ near 50% share price rise in the first two weeks of July, forward visibility in recruitment is notoriously difficult. Hays ensured a caveat on how it “expects near-term market conditions to remain challenging, with greater resilience in temporary and contracting than in permanent”.

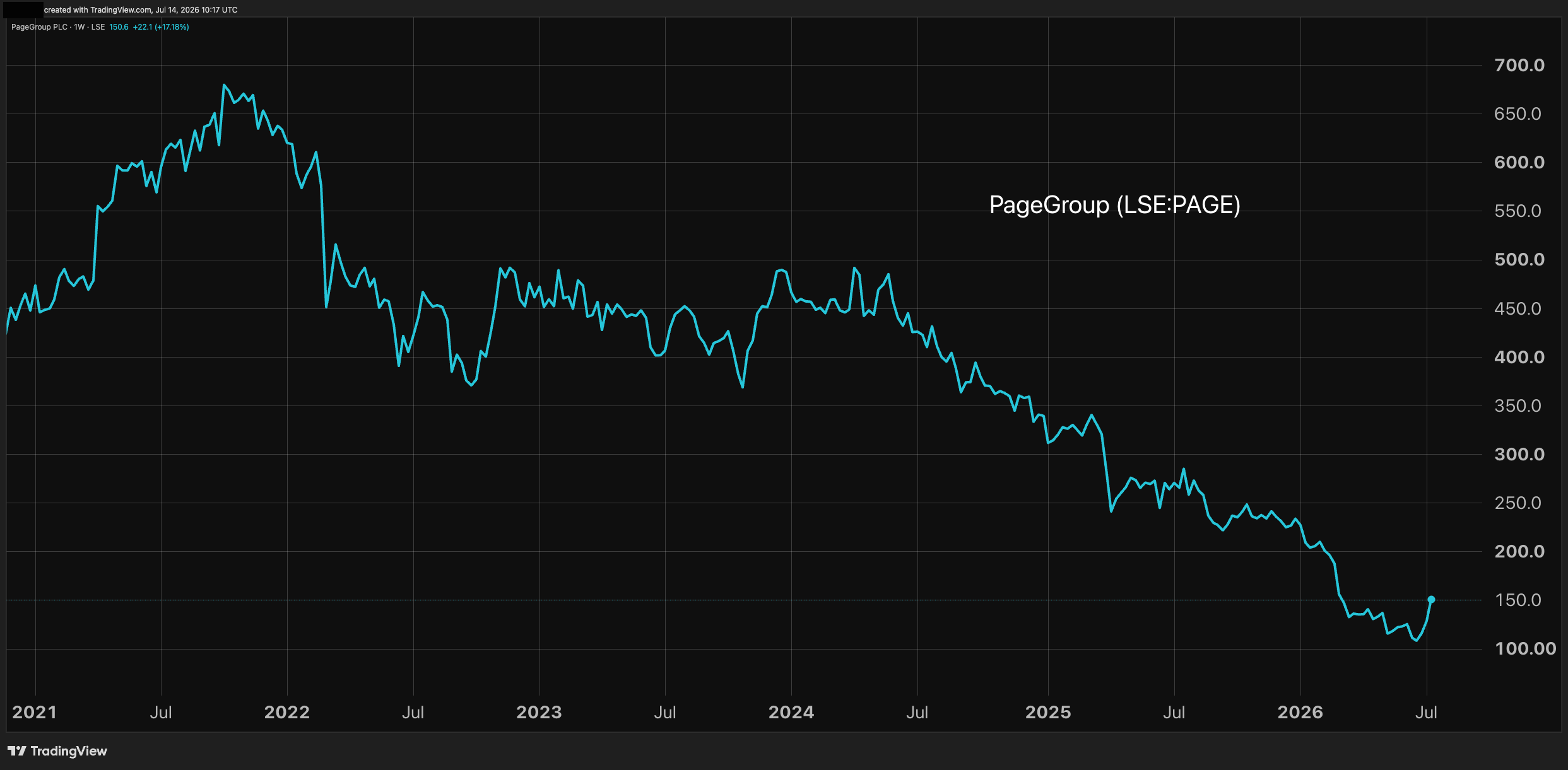

Yet PageGroup asserts a global market improvement

Yesterday its shares rose – again the magical 20% it would seem – to 154p after a second-quarter update to 30 June cited net fee income 0.2% softer like-for-like versus the first quarter down 4.9%, and also “improvement and signs of normalisation in trading in a number of our markets – now circa 50% in growth”.

PageGroup (LSE:PAGE) has, however, seen mixed performance geographically, with the Americas and Asia Pacific maintaining healthy net fee income growth versus Europe and the UK down. In terms of the fiscal first half-year, markets were 37% in growth, with the CEO citing “a high degree of uncertainty” in the outlook.

- ii view: cyclical play PageGroup surprises to the upside

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

Yet versus 3.11% of its shares shorted (over the 0.5% disclosure threshold), PageGroup also cites its highest level of productivity since the record year in 2022, and a record quarter for Page Executive, up 15%. This has been achieved despite the US/Iran conflict as a backdrop throughout the quarter.

The chart is also similar to Hays:

Source: TradingView. Past performance is not a guide to future performance.

PageGroup’s forward PE is around 33x the 2026 consensus EPS, easing near 17x for 2027, but the yield is more attractive than Hays at near 5% rising to 5.2%, albeit uncovered in 2026 and 1.1x earnings in 2027.

Not surprisingly, the market is taking its cue from underlying recruitment market dynamics on both shares rather than fretting over PEs if this is a major turning point.

I conclude with “buy” stances on both, although I would wait to see if these spikes abate after this surprise element. An averaging-in approach looks wise, plus paying attention to recession risk if the Middle East conflict festers.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.