Stockwatch: time to nibble at two cyclical shares

Directors have been buying up one of these companies and analyst Edmond Jackson believes the other is strategically well-positioned and attractively rated.

19th May 2026 10:52

by Edmond Jackson from interactive investor

In a 21 April macro piece – Are stock market highs really justified? – I queried if it was premature to consider recruiter shares after their unique five-year bear market.

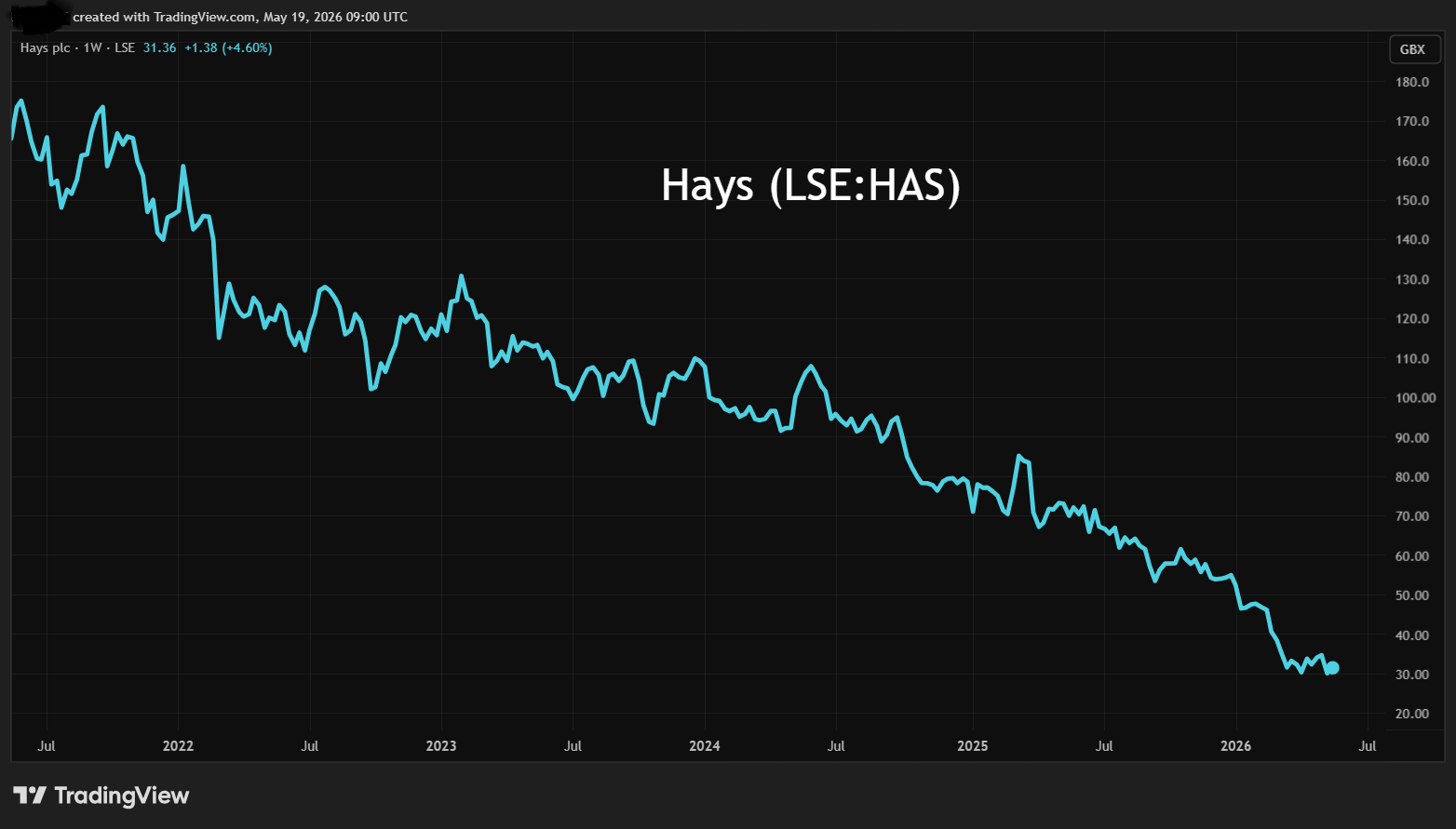

Mid-cap Hays and small-cap Robert Walters had seen their shares rise slightly after updates affirmed tough conditions, but charts did not affirm a bottom. Hays had edged up a couple of pence to 35p by 7 May, but as the wider market has seen a reality check over inflation and a stubborn Middle East war, the shares fell back below 30p. Walters has similarly eased, from 97p to 88p.

- Our Services: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

Despite this, I remain alert to recruiters given that those listed entities are “quality cyclicals” where it is possible that the shares start recovering well before evidence manifests of an upturn.

In terms of judging stock market lows, there have just been two interesting news items.

Hays’ new CEO bought £147,300 worth of shares at 30.3p on 14 May, which followed his buying £147,200 worth at 38.6p on 2 March, plus £96,200 worth at 56.6p on 1 October 2025. Four other Hays directors have also bought small lots lately in the near £500 million mid-cap company.

Source: TradingView. Past performance is not a guide to future performance.

Yesterday its shares rose 3.4%, or 1p to 31p, whether in recognition and/or with the market, but it does show how this kind of share can be sensitive to a break in gloom when down at this level.

The five-year chart is initially uninspiring and, for what forecasts are worth, net losses in the June 2024 and 2025 fiscal years are expected to rebound to an £18 million profit in respect of June 2026 and £31 million in 2027.

That would imply price/earnings (PE) multiples of 27x, easing to 15x, which can still seem rich given the challenges for white-collar professional recruitment that Hays is chiefly exposed to, plus any threat to jobs from AI.

It also seems high relative to reported operating margins well below 1.0% since the June 2024 fiscal year, hence returns on capital employed of 3.3% declining to 1.5%:

Hays - financial summary

Year end 30 Jun

| 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| Turnover (£ million) | 5,930 | 5,648 | 6,589 | 7,583 | 6,949 | 6,607 |

| Operating profit (£m) | 95.1 | 95.1 | 210 | 197 | 25.1 | 14.9 |

| Net profit (£m) | 47.5 | 61.5 | 154 | 138 | -4.9 | -7.8 |

| Operating margin (%) | 1.6 | 1.7 | 3.2 | 2.6 | 0.4 | 0.2 |

| Reported earnings/share (p) | 3.1 | 3.6 | 9.1 | 8.5 | -0.3 | -0.5 |

| Normalised earnings/share (p) | 5.7 | 3.4 | 9.3 | 8.5 | 1.4 | -0.4 |

| Operational cashflow/share (p) | 23.1 | 0.4 | 10.1 | 10.2 | 6.0 | 6.9 |

| Capital expenditure/share (p) | 1.7 | 1.1 | 1.4 | 1.8 | 1.5 | 1.4 |

| Free cashflow/share (p) | 21.4 | -0.7 | 8.7 | 8.4 | 4.5 | 5.5 |

| Dividend per share (p) | 0.0 | 1.2 | 2.9 | 3.0 | 3.0 | 1.2 |

| Earnings cover (x) | 0.0 | 3.0 | 3.2 | 2.8 | -0.1 | -0.4 |

| Return on total capital (%) | 9.0 | 9.1 | 21.9 | 23.3 | 3.3 | 2.1 |

| Cash (£m) | 485 | 411 | 296 | 146 | 161 | 169 |

| Net debt (£m) | -256 | -209 | -111 | 54.2 | 123 | 144 |

| Net assets (£m) | 853 | 872 | 796 | 670 | 558 | 467 |

| Net assets per share (p) | 50.9 | 52.0 | 48.2 | 42.2 | 35.2 | 29.3 |

Source: company accounts.

The UK and Ireland represent 27% of net fee income (or gross profit, the key performance benchmark for recruiters). Germany is the largest contributor at 32% and has seen a prolonged period of stagnation, but is forecast to grow between 0.5% and 1.2% in 2026.

Obviously, such forecasts are exposed to the risk that conflict, or at least a lack of resolution, in the Middle East drags on, given higher energy costs and supplies disruption. Germany remains a turnaround situation for Vodafone Group; and it’s difficult for Hays, too, with net fee income there down 11% over January to March.

Hence, it is easy to understand why investors are cautious about potentially “catching a falling knife”, although it may only need signs of underlying market stabilisation for a cyclical share like this to tick higher.

- Results upgrade sparks Currys rally

- Insider: here's what directors at 3i and Aviva have been up to

- 10 hottest ISA shares, funds and trusts: week ended 15 May 2026

One’s macro view likely dominates what stance to take. In April, I felt forced to compromise with “hold”.

Does material repeat buying of a cyclical share by its new CEO warrant including in appraisal for investment timing, or does it chiefly reflect his animal spirits on being appointed? Whatever, it certainly affirms belief in long-term value.

The prospective yield is 2.8% covered twice by earnings, again depending how reliable those forecasts are. Not exactly a prop, the focus remains on earnings recovery, but even if earnings per share (EPS) of 9.1p and 8.5p were “peak” in the June 2023 and 2024 years, a recovery to just 3p on a two-year view implies a PE of 10.

Hence, I empathise with the CEO’s buying and upgrade – albeit as a starter “buy” at 31p rather than loading up. Hostilities in the Middle East fired up again yesterday and it remains hard to see where a durable settlement lies.

Staffline arrests its share price fall

By contrast, AIM-listed Staffline Group is a £43 million blue-collar recruitment group with a record of bucking the macro trend recently. It serves food retail and logistics via Recruitment GB, which enjoys a strong position with over £1 billion revenue. Recruitment Ireland is lower at £100 million but still enjoys a 20% share in Northern Ireland, serving both temporary and permanent white-collar recruitment. A defensive angle is offered by way of health and social care in the public sector.

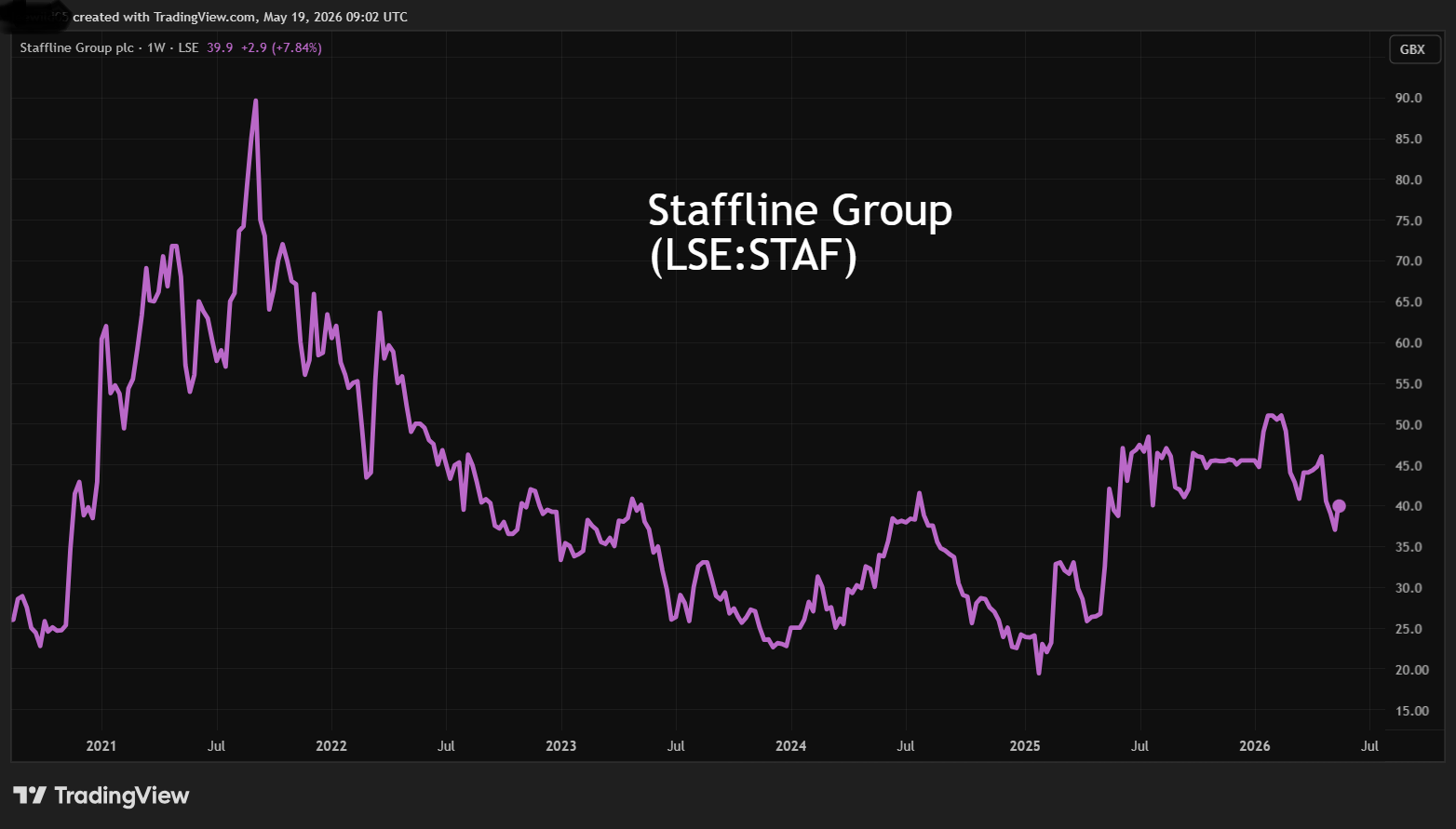

Its five-year chart is relatively encouraging versus Hays’, although any sense of a bullish “bowl” is checked by flatlining from last September, while April-May saw a drop from 45p to 37p:

Source: TradingView. Past performance is not a guide to future performance.

Possibly, Staffline got caught up in the perception of permanent white-collar recruitment being disrupted by lay-offs and encroaching AI, although it is chiefly a different business, supplying up to 50,000 workers daily to clients with flexible working needs.

While this can seem like it is exposed to the “gig economy”, the Employment Rights Act 2025 insists on guaranteed hours – extending to agency workers – hence it ought to favour larger recruiters that are compliant. Staffline does appear to be taking market share, both via more staff to existing clients and new contracts.

A watershed development last May was a partnership with logistics provider Culina Group, outsourcing all its agency labour requirements to Staffline and contributing around £100 million revenue this year in the context of consensus for £1,234 million.

Admittedly, reported operating margins are low like Hays – recovering to 1.2% last year, although return on capital was 31%.

Staffline shares dipped 2p last Friday as macro fears resurfaced but rose 3p to 40p yesterday as a bullish AGM update coincided with a rising market.

During the first four months of 2026 there has been a 14.6% like-for-like increase in net fee income on continuing activities, underpinned by a 9.1% rise in temporary worker hours for Recruitment GB. This is said to reflect sustained demand both for temporary and agency-based recruitment. Recruitment Ireland has similarly seen a strong start to 2026.

The company said: “This excellent operational performance is underpinned by a healthy new business pipeline, driven by organic growth and market share gains across Staffline’s blue-chip customer base.”

- High-yielding shares beyond the FTSE 100 that the pros are backing

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

Strong trading cash flows have been part-deployed to buy back 6.0% of the issued share capital for £3.2 million at an average 45.4p per share. Staffline said: “Notwithstanding the ongoing challenging macro-economic backdrop, 2026 results will be in line with management’s expectations, as the group’s scale and reach, coupled with its reputation for service excellence and governance, continue to deliver strong organic growth.”

That’s some chutzpah – asserting to results for the year to 31 December – given, as I explained in a 5 May macro piece, that it looks like the real economic crunch will come from June unless the Strait of Hormuz is promptly reopened.

The pattern of Staffline directors’ trading contrasts with Hays, with no share buying since chair Thomas Spain bought £180,400 worth at 34.7p in June 2024. He subsequently sold down a lot more but is closely associated with Henry Spain Investment Services, which owns 29.2% of the company, and this holding has not changed lately. Meanwhile, executives have simply exercised share options and sold all shares arising, or at least enough to pay tax.

Two brokers following Staffline have kept their £6.5 million net profit forecasts for 2026 but raised EPS (due to buybacks) from 5.6p to 6.0p, implying a 36% increase and forward PE of 6.6x at the 39.5p mid share price. So, might such a radically lower PE versus Hays adequately compensate for the risks?

Notwithstanding the 2020 disruption of Covid, the six-year profits record is bumpy and there is no dividend payout policy, which some investors would say is proof of cash flow reliability, hence more vital than yield itself.

Staffline did, however, launch another buyback scheme involving five million shares, or 4.3% of the issued share capital, which is more tax-advantageous for capital gain-oriented investors. That said, such schemes can be periodic unlike commitment to a dividend policy. I see this as less important anyway than whether Staffline is strategically well-positioned and attractively rated, which it appears to be.

Staffline Group - financial summary

Year end 31 Dec

| 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| Turnover (£ million) | 928 | 943 | 928 | 871 | 993 | 1,107 |

| Operating profit (£m) | -44.3 | 2.3 | 4.6 | 1.6 | 9.9 | 13.0 |

| Net profit (£m) | -52.7 | 1.2 | 3.8 | -11.0 | -8.3 | 4.8 |

| Operating margin (%) | -4.8 | 0.2 | 0.5 | 0.2 | 1.0 | 1.2 |

| Reported earnings/share (p) | -64.6 | 1.3 | 2.3 | -0.8 | 3.0 | 4.4 |

| Normalised earnings/share (p) | -10.4 | 2.5 | 3.0 | 1.5 | 3.1 | 4.4 |

| Operational cashflow/share (p) | 86.9 | -18.7 | 3.6 | 8.0 | 15.3 | 4.8 |

| Capital expenditure/share (p) | 3.5 | 3.7 | 2.0 | 1.7 | 3.2 | 4.0 |

| Free cashflow/share (p) | 83.4 | -22.4 | 1.6 | 6.3 | 12.1 | 0.8 |

| Dividend per share (p) | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Return on total capital (%) | -76.2 | 3.0 | 6.0 | 2.7 | 21.5 | 30.9 |

| Cash (£m) | 24.5 | 29.8 | 31.0 | 13.3 | 14.6 | 8.4 |

| Net debt (£m) | 14.0 | -2.3 | -0.1 | 0.2 | -4.9 | 2.5 |

| Net assets (£m) | 22.2 | 68.2 | 71.7 | 54.9 | 41.4 | 38.6 |

| Net assets per share (p) | 29.1 | 41.1 | 43.3 | 36.8 | 29.1 | 31.4 |

Source: company accounts.

I therefore believe it also merits a starter “buy” stance with better value credentials than Hays. Accumulating either or both shares, however, will be a case of feeling one’s way forward relative to macro cues.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.