Valuable lessons learned from my 2026 share tip performance

It’s been an interesting ride since he backed 13 shares to do well this year. Analyst John Ficenec reveals how they’ve performed so far and explains what he’s learned from the experience.

13th July 2026 13:49

by John Ficenec from interactive investor

Am I the worst stock picker in the world? That was the only conclusion I was left with after an awful start to the year. The war in Iran inflicted a worst-case scenario hit to my stock picks, and political turmoil knocked them even lower. However, the darkest investing days often teach us the most valuable lessons and bruised but unbowed these share tips have plenty more value to come.

- Learn with ii: How to become an ISA millionaire | ISA Investment Ideas | Top ISA Funds

Investing in the eye of the storm

At the start of this year, I thought the markets had become overly gloomy about the UK’s prospects. This left plenty of profitable and cash-generative companies on ratings far too low for their underlying value. It was all true, and that should have meant share prices steadily rising throughout the year. Unfortunately, President Donald Trump had other ideas, and his war against Iran was a disaster for the UK and my stock picks.

The International Monetary Fund (IMF) loudly proclaimed that rising oil prices would hit the UK the hardest of the world economies. The OECD (Organisation for Economic Co-operation and Development) joined the pile on stating that the UK would be the hardest hit of the G20 major economies and downgraded our GDP growth just for good measure.

Not only had I focused my picks on the hardest-hit economy in the world, but it was also weighted towards retail and leisure sectors that were most sensitive to this downturn. This created additional pain as the great British public retreated into their shell as oil and therefore petrol prices soared.

In a matter of weeks there was a sea of red, my picks from the pub sector Mitchells & Butlers (LSE:MAB), Wetherspoon (J D) (LSE:JDW) and Young & Co's Brewery Class A (LSE:YNGA) were all down 20%. The worst hit was travel platform On The Beach Group (LSE:OTB) that suffered a triple whammy from rising fuel prices, the loss of Dubai as a destination, and a weak consumer, sending shares down 30%. Currys (LSE:CURY), the electrical retailer, slumped 20% and industrial polymer producer Victrex (LSE:VCT) fell 20%.

- Six stocks that could double their dividend quickly

- Stockwatch: a turnaround play for both capital upside and yield

Soul searching

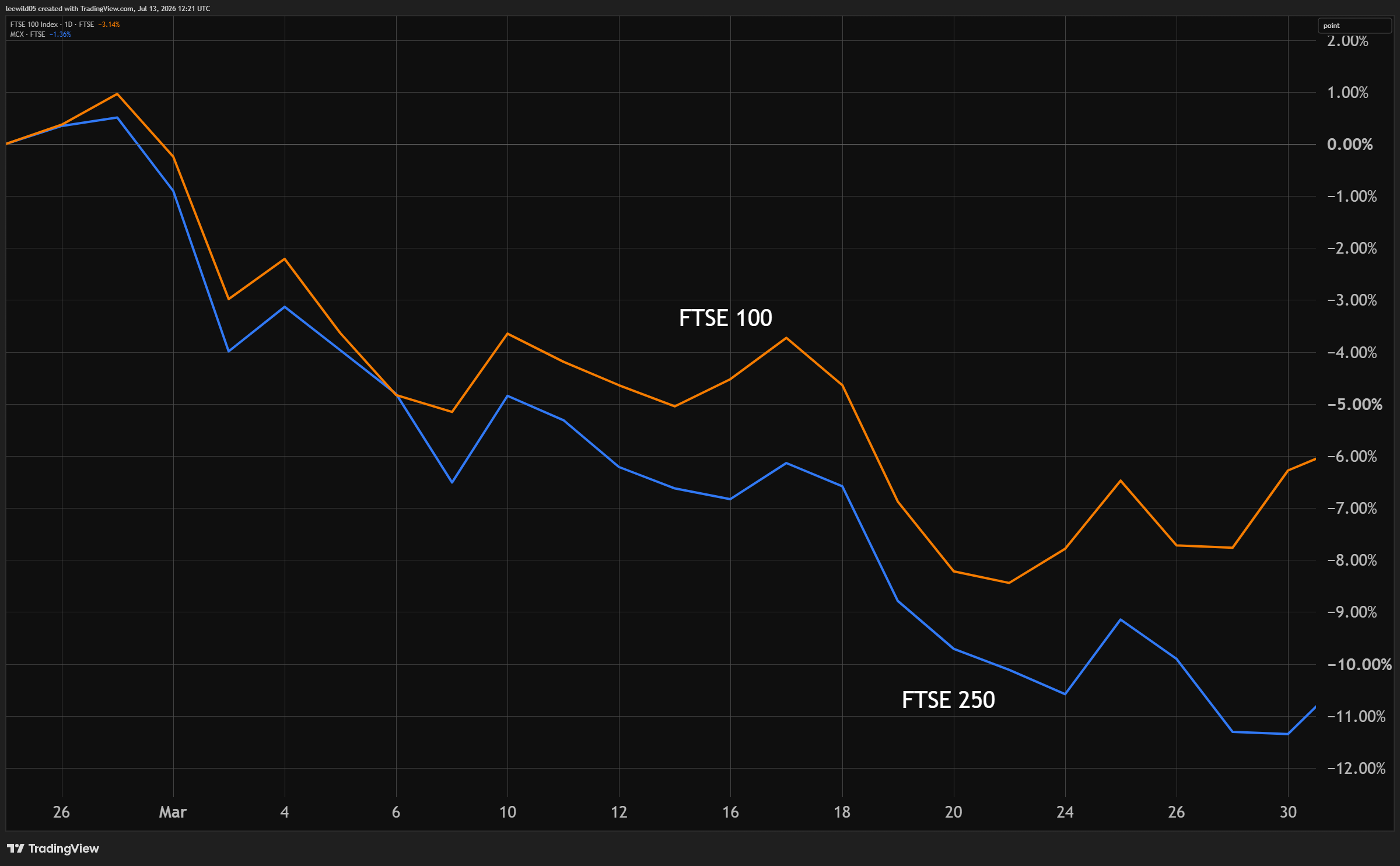

At times like this it’s a genuine question of why bother. The FTSE 100, with its heavy weighting of energy companies, was only down about 8% during the same period, so just buy a tracker and be done with it. But times of adversity ensure you test the veracity of why you invested in the first place. Going back and checking that again, especially when serious losses are staring you in the face, provides some of the most valuable lessons in investing. The first one being: what was your fundamental reason for buying these shares? And the second: how are these companies performing?

Source: TradingView. Past performance is not a guide to future performance.

Solid foundations

After overcoming the urge to chuck the towel in and sell everything, it was time to revisit the reason for picking those shares. In short, UK economic growth was returning albeit slowly, inflation was slowing, and interest rates were falling. All this should mean that cyclical stocks in the UK would recover in the months ahead. If UK growth kept steadily building, the rating on the FTSE 250 at around 12 times earnings would steadily return to historic norms of up to 20 times.

Looking through all the alarmist headlines on the UK’s economic woes from the Iran war, inflation was still falling and growth returning, even in a worst-case scenario of a prolonged war they were just being delayed.

Looking into the economic analysis there was also uncertainty about how bad the inflationary shock from higher oil prices would be. UK consumer confidence had been impacted, but household incomes were steadily improving from higher wages and slowing inflation.

The Iran war therefore was purely an external shock, that many didn’t believe would be prolonged, and the underlying UK economy was still improving despite taking a hit. Also, the conflict was not a mistake in the fundamental thinking at the start, it was an event that was impossible to predict, and it wasn’t clear how badly it would impact the companies themselves. So, the next thing to double check was the performance of the underlying companies.

Profitable performance

The reason I picked each individual share was because the companies themselves were all enjoying improved trading, cash generation and profits. Or in the case of the pub companies, although trading was slowing, the inflation pressure from wages and food prices was easing on business, while their customer base had more pounds in their pockets.

Looking through each of the companies, while there was little information initially on how the war in Iran would impact trading, there was enough momentum to suggest they could weather a short-term dip in consumer confidence.

Counting the cost

The next important step was to gain perspective on what was going on with the investments. Back in January, I picked 13 different companies, and while a 20% share price fall across the portfolio during the darkest days in March and April is alarming, not everything was falling. Companies like infrastructure group Keller Group (LSE:KLR) was up more than 20% by the end of March, and pork producer Cranswick (LSE:CWK) was steadily rising.

- Share Sleuth: a one-of-a-kind new holding for the portfolio

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

There is always the risk of succumbing to the sunk-cost fallacy here whereby you hold on exactly because it has fallen. But the underlying data on UK inflation, growth and companies themselves hadn’t changed. Given that the reason for buying the shares in the first place still held true, there was no reason to make a knee-jerk response based on some volatility. Investing in smaller companies on the FTSE 250 comes with expected risks such as these. After the initial panic I was happy to hold on.

Patience pays

A funny thing has happened during the past few months. The IMF has performed a reverse ferret and upgraded the UK’s economic outlook for this year, making it the third-fastest growing in the G7. The pub companies have all been reporting better sales and easing cost pressures, sending the shares on a nice journey upwards.

Keller Group (LSE:KLR), the groundwork and foundations specialist upgraded the profit outlook sending its shares skyward. It looked an anomaly trading on 7 times earnings in January, and so it proved.

Currys (LSE:CURY) has just reported an 18% jump in profits, with strong trading continuing into the new financial year, leaving shares up 18% from when we first looked at them. Soft drink Irn-Bru maker make AG Barr (LSE:BAG) has been largely flat, but a recent acquisition of rival Fentimans should help boost earnings later this year.

Gamma Communications (LSE:GAMA) at 893p and a price/earnings (PE) ratio of just 9 times, has attracted a takeover bid for the cash-generative business. RS Group (LSE:RS1), the distributor of industrial and electronic components across the UK, Europe, Asia, and America remains well placed to benefit from a recovery in Europe.

Victrex (LSE:VCT), the maker of high-performance polymer for aerospace, automotive, oil and gas, and medical devices is a good example of the hidden quality. The shares were hard hit by potential disruption from the Iran war, but it just announced revenues some 18% higher for the third quarter ended June. Prices that have been falling for the past few years stabilised, and shares jumped 20% higher on the trading update. The shares are still below the tip price but with strong cash generation and an 8.7% dividend, I’m happy to stay in this one.

After a roller-coaster ride so far this year, the share tips as a whole are up 9%, compared to the FTSE 250 up 1% and the FTSE 100 up 3% during the same period. It hasn’t quite kept pace with the S&P 500, which is up 10%, or the Russell 2000 of smaller US companies up 11% over the same period. But I don’t like the risk associated with an economy relying on the AI boom and I’m quite happy to take lower returns on these shores.

| Share price | |||

| 21/01/2026 | 10/07/2026 | Return | |

| Keller Group (LSE:KLR) | 1,694 | 3,438 | 103% |

| Currys (LSE:CURY) | 135 | 159 | 18% |

| Cranswick (LSE:CWK) | 5,010 | 5,510 | 10% |

| Young & Co's Brewery Class A (LSE:YNGA) | 812 | 872 | 7% |

| Wetherspoon (J D) (LSE:JDW) | 680 | 719 | 6% |

| Kier Group (LSE:KIE) | 216 | 219 | 1% |

| Mitchells & Butlers (LSE:MAB) | 260 | 261 | 0% |

| Gamma Communications (LSE:GAMA) | 889 | 888 | 0% |

| AG Barr (LSE:BAG) | 648 | 628 | -3% |

| RS Group (LSE:RS1) | 637 | 613 | -4% |

| Churchill China (LSE:CHH) | 361 | 344 | -5% |

| Victrex (LSE:VCT) | 718 | 683 | -5% |

| On The Beach Group (LSE:OTB) | 211 | 174 | -18% |

| Tips return | 8.6% |

| Total return with dividends | 10.3% |

| FTSE 100 | 3.3% |

| FTSE 250 | 0.9% |

| S&P 500 | 9.7% |

| Russell 2000 | 10.9% |

These returns illustrate why picking shares still has a future. For an investor with a portfolio of £50,000 held for a 10-year period, every 1% increase in returns is worth around an extra £10,000. So £50,000 invested for 10 years at 5% returns around £85,500, or a gain of £35,500, but if you can achieve closer to 10% a year that £50,000 becomes about £143,000, or a gain of £93,000 to your savings pot. I can’t think of anything that offers such a reward in terms of boosting your savings, despite the soul searching that comes with it.

John Ficenec is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.