Stockwatch: should you buy these takeover targets?

Analyst Edmond Jackson mulls valuation arbitrage and other factors in the wake of the 10th anniversary of Brexit, and considers what this takeover trio tells us about UK plc.

26th June 2026 12:36

by Edmond Jackson from interactive investor

It is pertinent to note three offers – mooted or actual – this week versus a consensus that the risk premium for UK assets has just risen as a result of a likely Andy Burnham government engaging more spending.

The bond market appears to suspect that he may tweak fiscal rules and extend the period over which analysis is performed, spending more money up front. Infrastructure projects and higher defence spending could (somehow) be pushed off the balance sheet but markets may see through this and test a new government. So, be wary of UK assets yet to price this in.

- Invest with ii: Open an ISA | ISA Investment Ideas | Transfer a Stocks & Shares ISA

Such wariness does not, however, seem in the market for corporate control, which is taking a much longer-term view.

A second US buy in UK pawnbroking and jewellery retail

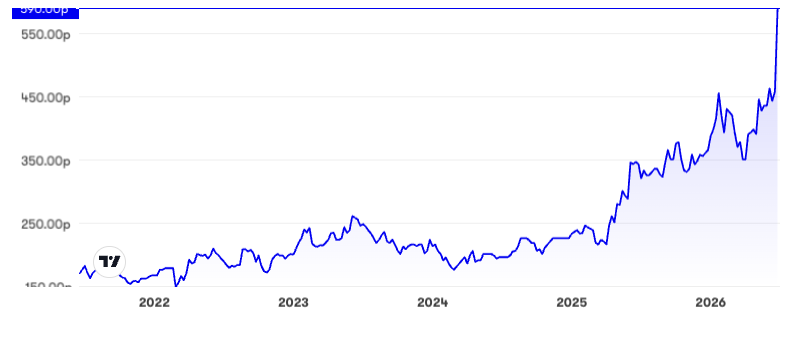

Last Tuesday, an agreed £203 million takeover was declared for Ramsdens Holdings (LSE:RFX), the pawnbroking and gold/jewellery retailer and also foreign-exchange provider, at 609p per share including dividends, representing a 46% premium to the 412p average price over the last three months, and a 22% premium to the all-time high of 493p on 3 June.

London’s relatively modest ratings meant even this premium implies an exit price/earnings (PE) of 9x, the company broker’s earnings per share (EPS) estimate for the 30 September 2026 year and 13x 2027, with modest gold prices assumed.

The market’s recent caution is in part explained by a downtrend in gold prices after a £4,000/ounce all-time high last March in response to the US/Iran war, to around £3,000 currently, but the market has for many years rated pawnbroker/gold trader shares cheaply.

Source: interactive investor. Past performance is not a guide to future performance.

The buyer is FirstCash Holdings Inc (NASDAQ:FCFS), which in May 2025 also offered £297 million for H&T Group, the UK’s largest pawnbroker, 661p per share being nearly 90% higher than January.

I drew attention to both shares as a “buy” given that pawnbroking seems a worthwhile business for challenged times, although being twinned with gold trading does leave such firms exposed to cyclicality.

For H&T, from end-2018 at 260p also 350p in January 2025 having dropped from near 500p. Amid its takeover by FirstCash, I suggested Ramsdens had similar 13% operating margins over the previous three financial years plus good dividend growth covered over twice by earnings. At 300p, the prospective yield was 4.5% and the PE around 10x versus a trading update for the six months to March 2025 suggesting interim profit ahead of expectations.

- Trading Strategies: an overlooked FTSE 100 stock to consider

- What a Burnham premiership could mean for your long-term wealth

Since FirstCash trades on 20x earnings there is the straightforward arithmetic benefit of acquiring lower-rated UK companies, and a wider US/UK valuation differential supports ongoing takeovers. This kind of trade buy also involves synergistic benefits of integration compared with private equity.

Another example of US/UK ‘valuation arbitrage’

Wednesday heralded news of a possible offer at 925p per share for Segro (LSE:SGRO), a real estate investment trust owning logistics and industrial facilities in the UK and Europe, from Prologis Inc (NYSE:PLD), a similar operator. This values Segro at £12.5 billion versus a £105 billion equivalent for Prologis.

Source: interactive investor. Past performance is not a guide to future performance.

This looks a similar “valuation arbitrage” to FirstCash buying UK pawnbrokers, in the sense that Prologis trades on the New York Stock Exchange at 2.5x net asset value (NAV) versus Segro around NAV, although it looks necessary for Prologis to raise terms.

- FTSE 100 shares round-up: Segro bid, property boom, Games Workshop

- Tax on cash but money market funds spared in ISA rule change

So, the situation could evolve given simple maths makes a deal attractive for Prologis unless it is just trying its luck. I find it speculative to firmly conclude “buy” rather than “hold”, although it seems worth consideration.

easyJet involves a dilemma of what valuation to recommend

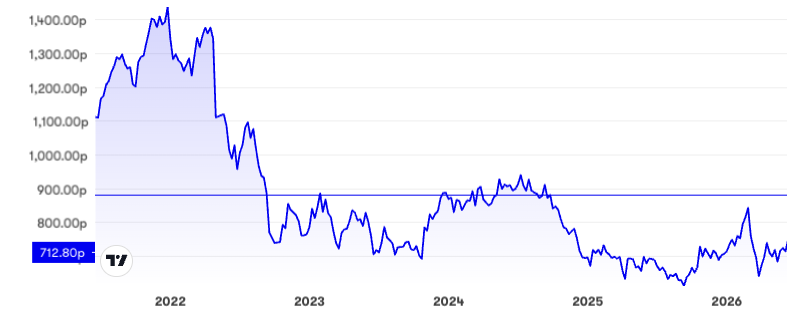

US private equity firm Castlelake is at its fourth, yet still rejected, takeover offer for easyJet (LSE:EZJ) of 650p per share, worth £4.9 billion, with the market yesterday taking encouragement over how its board is now allowing the offeror access to limited commercial information, potentially towards a more attractive proposal. A “put up or shut up” deadline has been extended to 5pm on 5 July.

Obviously you could say the board has a fiduciary duty to shareholders to exact value, hence it shouldn’t block interest, which may be different from whether they are actually minded to recommend terms unless materially higher.

- The undervalued UK bank shares tipped to rally

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

I drew attention to easyJet as a “buy” at 405p in December 2023 with a target to double over three years or so. Despite the risk of Middle East war and/or recession, its balance sheet was plenty strong with net cash, and annual revenue to 30 September had rebounded 42%. Also, three years of losses became a £324 million net profit, helped by booking strength.

Admittedly, fortunate timing had a role otherwise the shares traded volatile sideways in a 475p to 550p range until the US/Iran war saw a drop near 350p.

Source: interactive investor. Past performance is not a guide to future performance.

At 574p, the shares trail the offer price as the market weighs event probability. Even 650p only recalls 2020-21 levels, and during 2014 to 2018 around 1,500p was thrice achieved, with the main bull phase happening from around 300p in 2011.

Somewhat ironically, a pre-2020 annual revenue was just over half the £11 billion it is trending towards now, but EPS was around 75p versus the market expecting only 21p in respect of the September 2026 year and 42.5p in 2027 – implying an exit PE around 30x easing to 15x based on the 650p per share offer.

Quite whether a cyclically adjusted PE is more relevant here, or margins are being pressured [is debatable]. An operating margin of around 5% compares with 15% for International Consolidated Airlines Group SA (LSE:IAG).

So, it is tricky here for both sides to agree on price and offerors may tantalisingly go through various rounds and still back off.

I doubt this situation will turn hostile with an offer direct to shareholders, as private equity usually needs to work with existing management – in part explaining my sense of “hold” rather than “buy”.

Perhaps there is a parallel in that budget carrier easyJet and Ramsdens are both in the “coping with the higher cost of living” realm.

Scepticism may also be justified re Brexit doom

Amid the Brexit 10th anniversary, there has been much handwringing about how the UK economy will go down the swanny unless we re-join the European Union, or at least its customs union. A left-wing friend sent me a Guardian piece on small agricultural-related businesses being hit hard by red tape.

Yet, overall, trade with the EU in services is up 57% over the last decade, driven by accounting, legal and consultancy versus goods exports down 14% since 2019, with imports also affected.

Quite whether we have benefited from the Brexiteers’ mantra of the “opportunity to cut our own trade deals” given that the templates were significantly EU-based anyway [is also debatable]. Yet with a US President recently intent on punishing the EU variously on trade, being outside the EU has had some virtue.

- Brexit: biggest winners and losers 10 years on

- 10 years on from Brexit: top-performing funds and key trends

I do think this fixation with trade arrangements puts the proverbial cart before the horse. More vital is whether the UK markets goods and services adeptly and what economic demand exists abroad.

Last Tuesday’s prelims to 31 March from musical equipment group Gear4music (Holdings) (LSE:G4M) were a good example. European revenue showed the strongest growth, up 37% to £75 million, while the UK rose 26% to £114 million, with the rest-of-world being marginal. European growth had lagged the UK in recent years, not due to trade restrictions but weak economies and also aggressive discounting by under-performing rivals.

More widely, I cannot recall any UK-listed company blaming trade arrangements for weakness in European sales, although I respect red tape for smaller companies can be catastrophic and some loss of multinational investment has affected overall growth.

Foreign companies would not, however, be consistently trying to buy listed UK plc if prospects are as bad as Rejoiners contend.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.