Brexit: biggest winners and losers 10 years on

A decade after the UK voted to leave the European Union, Graeme Evans looks at how the UK stock market has performed against international peers, the risers, fallers and sectors to own.

23rd June 2026 08:57

by Graeme Evans from interactive investor

BT Group (LSE:BT.A) and Taylor Wimpey (LSE:TW.) shareholders are sitting on big losses whereas NatWest Group (LSE:NWG) andNext (LSE:NXT) shares have staged strong recoveries since the EU referendum 10 years ago today.

- Our Services: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

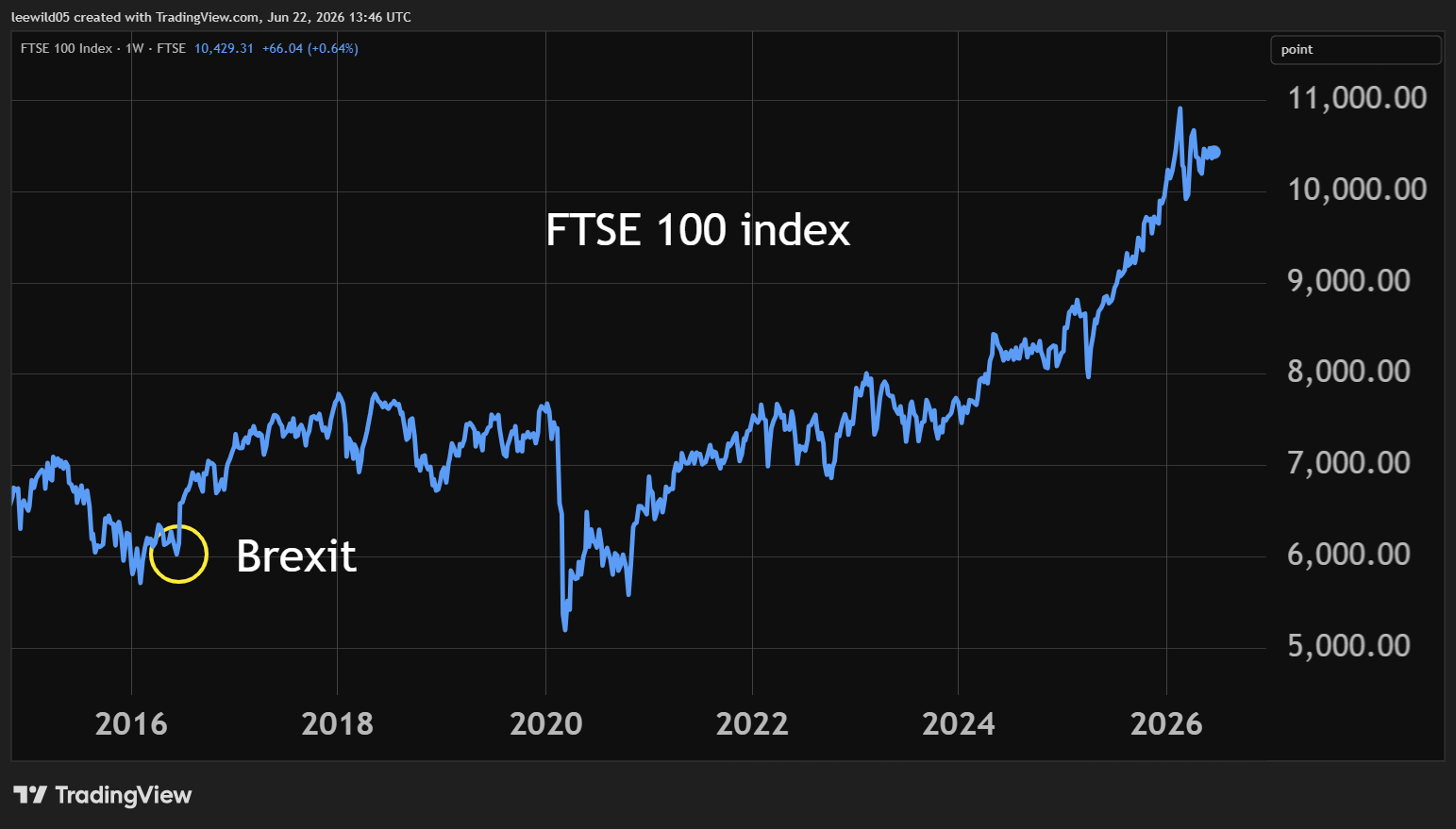

The story of the wider FTSE 100 index has been one of solid but unspectacular growth, with returns elsewhere much better than its 63.4%, or compound annual growth rate of 5%.

That’s partly due to the FTSE 100’s lower weighting of sectors which have outperformed globally, as well as the post-Brexit caution of international investors towards UK assets.

Source: TradingView. Past performance is not a guide to future performance.

The FTSE 250 index is up by an even more underwhelming 33%, or 3% a year as Deutsche Bank this week noted the return since 2020 was a third of the G7’s midcap equities average.

The larger increase in the UK’s post-pandemic borrowing costs, plus an estimated 4% decline in the size of the UK economy since Brexit and limited tech sector exposure, have left the FTSE 250 among the global backmarkers of the past decade.

- Bill Ackman talks IPOs, SpaceX and favourite tech stocks

- Insider: directors back recovery at two FTSE 250 stocks

Despite the strong trading of stocks including Greatland Resources Ltd (LSE:GGP), Jet2 Ordinary Shares (LSE:JET2) and Filtronic (LSE:FTC), the AIM 100 junior market is up by just 7.6% over the period.

The performances, which cover the 10 years up to Monday’s opening bell, are put in the shade by the 581% jump of the tech-laden Nasdaq 100, the 186% recorded by the US economy-focused Dow Jones Industrial Average and the 143% advance of Frankfurt’s Dax.

Major stock markets since Brexit

| Share price change (%) | ||||||

| Index | Price | Since Brexit | 2026 | 1 year | 3 years | 5 years |

| NASDAQ 100 | 30406.2 | 581.0 | 20.4 | 40.6 | 102.0 | 113.0 |

| NASDAQ Composite | 26517.9 | 440.0 | 14.1 | 36.4 | 94.5 | 86.0 |

| Nikkei 225 | 72354 | 346.0 | 43.7 | 88.4 | 118.0 | 150.0 |

| S&P 500 | 7500.58 | 255.0 | 9.6 | 25.7 | 71.2 | 76.6 |

| Bovespa Stock Index (Brazil) | 168334 | 226.0 | 4.5 | 22.8 | 41.5 | 30.7 |

| S&P BSE 100 Index (Mumbai) | 25584.4 | 205.0 | -6.4 | -2.5 | 33.3 | 59.4 |

| Dow Jones Industrial Average | 51564.7 | 186.0 | 7.3 | 22.2 | 51.9 | 51.9 |

| DAX Xetra (Germany) | 24913.1 | 143.0 | 1.7 | 6.7 | 55.8 | 59.3 |

| CAC 40 (Paris) | 8358.4 | 87.2 | 2.5 | 10.1 | 16.0 | 26.4 |

| Swiss Market Index | 13774 | 71.7 | 3.7 | 16.0 | 23.2 | 15.0 |

| FTSE 100 | 10354.3 | 63.4 | 4.3 | 18.0 | 38.0 | 46.0 |

| FTSE All-Share | 5567.94 | 59.9 | 4.1 | 16.8 | 36.4 | 37.6 |

| FTSE 350 | 5628.95 | 59.2 | 4.1 | 16.9 | 36.6 | 38.5 |

| SSE Composite Index (Shanghai) | 4090.48 | 41.4 | 3.1 | 21.7 | 27.9 | 15.0 |

| FTSE 250 | 23048.4 | 33.0 | 2.6 | 9.0 | 25.7 | 1.6 |

| Hang Seng (Hong Kong) | 23768.5 | 13.9 | -7.3 | 1.0 | 23.7 | -16.0 |

| FTSE AIM All-Share | 795.73 | 9.5 | 3.9 | 4.8 | 2.9 | -34.9 |

| FTSE AIM 100 | 3705.14 | 7.6 | 1.4 | 1.3 | 1.0 | -37.9 |

Source: ShareScope. Data as at UK market open 22 June 2026. Past performance is not a guide to future performance.

While a pandemic and two energy price shocks heavily influence the results, a look at trading in the period since the Brexit vote still highlights the importance of keeping a diversified portfolio, being invested for the longer term and not overreacting to negative events.

Ten of the 38 sectors in the FTSE 350 have risen by 100% or more over the subsequent decade, while 33 stocks of the current FTSE 100 have at least doubled in value, ranging from Tesco (LSE:TSCO) at 106% to Polar Capital Technology Ord (LSE:PCT) at 1,120% and Games Workshop Group (LSE:GAW) at 4,380%.

Twenty stocks are in negative territory a decade later, with the telecoms, home construction and real estate investment trust sectors among the hardest hit. That’s reflected in declines of more than 50% or more for BT Group, Vodafone Group (LSE:VOD), Barratt Redrow (LSE:BTRW) and Land Securities Group (LSE:LAND).

The shockwaves of the referendum result wiped an initial $2 trillion (£1.5 trillion) from the value of global markets, with the FTSE 100 index down by as much as 7% in early trading to less than 6,000.

The banking sector endured its worst session since the collapse of Lehman Brothers in 2008, while fears of recession and sliding house prices left Taylor Wimpey down by 29% as housebuilders and other UK-focused companies endured turbulent trading.

- Shares for the future: 2026 a low point for very profitable firm?

- Stockwatch: high stakes for one of UK’s most-shorted shares

Defensive stocks and overseas earners like GSK (LSE:GSK) and Diageo (LSE:DGE) rose on the day as sterling fell by 10% at one point against the US dollar to levels not seen since 1985 at $1.35.

Reassuring comments by Bank of England governor Mark Carney later helped the FTSE 100 index to finish 3.1% lower at 6,138, although the FTSE 250 still lost 7% at close to 16,000.

The flight to safety lifted government bond prices and gold surged 5% to its highest point in three years at $1,322 an ounce. The uncertainty left Brent crude down 5% to $48.41 a barrel.

Airlines group International Consolidated Airlines Group SA (LSE:IAG), which owns British Airways and Iberia, was among the first companies to update investors on the morning of the referendum result.

Its shares skidded by more than 20% as it issued a profit warning, although boss Willie Walsh added that he believed that the vote would not have a long-term material impact.

By the following summer the shares had doubled to just under 500p before the pandemic shattered the recovery to leave them closer to the £1 mark. They are now a third higher than the day of referendum, which compares with the 60% fall of low-cost carrier easyJet (LSE:EZJ).

FTSE 100 since Brexit

| Share price change (%) | ||||||

| Company | Price | Since Brexit | 2026 | 1 year | 3 years | 5 years |

| Games Workshop Group (LSE:GAW) | 20200p | 4380 | 6.8 | 23.9 | 93.3 | 80.2 |

| Polar Capital Technology Ord (LSE:PCT) | 729.5p | 1120 | 57.2 | 112.0 | 233.0 | 214.0 |

| Antofagasta (LSE:ANTO) | 3919.5p | 790 | 19.5 | 131.0 | 163.0 | 173.0 |

| Diploma (LSE:DPLM) | 7217.5p | 746 | 36.3 | 50.9 | 144.0 | 144.0 |

| Lion Finance Group (LSE:BGEO) | 11450p | 578 | 23.1 | 73.1 | 275.0 | 748.0 |

| Rolls-Royce Holdings (LSE:RR.) | 1399.3p | 533 | 21.7 | 57.6 | 797.0 | 1190.0 |

| Scottish Mortgage Ord (LSE:SMT) | 1476p | 474 | 24.5 | 49.2 | 125.0 | 15.8 |

| Anglo American (LSE:AAL) | 3903p | 462 | 26.5 | 94.0 | 67.4 | 39.8 |

| Computacenter (LSE:CCC) | 4255p | 409 | 45.2 | 69.8 | 89.4 | 67.8 |

| Halma (LSE:HLMA) | 3951p | 309 | 11.7 | 26.7 | 76.7 | 45.1 |

Source: ShareScope. Data as at UK market open 22 June 2026. Past performance is not a guide to future performance.

The vote mired Europe's financial sector in regulatory uncertainty and left UK lenders fearing a rising toll of impairments given the potential for a much weaker economy to add to the high level of UK household debt and real wage compression.

These worries were reflected in the first day performance of UK banks as Lloyds Banking Group (LSE:LLOY) closed 21% lower, Royal Bank of Scotland fell 19% and Barclays (LSE:BARC) reversed 18%.

RBS, which changed its name to NatWest in summer 2020, reported a 15% slowdown in mortgage applications compared to the three weeks prior to the referendum.

It also warned that the low rate and low-growth environment made achieving its longer-term cost:income ratio and return targets by 2019 much more challenging.

Even though the company had materially de-risked and its legacy credit portfolios were much reduced compared with the financial crisis a decade earlier, shares still lost a quarter of their value over the course of 2016 to close the year at 242p.

They have risen by 164% since then and by 136% across the Brexit decade, as interest in the banking sector has benefited from the resumption of shareholder returns through dividends and buybacks and the margin-enhancing impact of higher for longer interest rates.

The recovery of Lloyds Banking Group has lagged NatWest at 46%, whereas the US and investment banking exposure of Barclays has helped its shares put on 167%. Asia-focused lenders HSBC Holdings (LSE:HSBA) and Standard Chartered (LSE:STAN) are up by 216% and 256% respectively.

Bank sector since Brexit

| Share price change (%) | ||||||

| Company | Price | Since Brexit | 2026 | 1 year | 3 years | 5 years |

| Standard Chartered (LSE:STAN) | 2059p | 256 | 13.0 | 74.7 | 208.0 | 342.0 |

| HSBC Holdings (LSE:HSBA) | 1436.5p | 216 | 22.4 | 65.7 | 137.0 | 239.0 |

| Barclays (LSE:BARC) | 499.075p | 167 | 4.9 | 54.0 | 240.0 | 189.0 |

| NatWest Group (LSE:NWG) | 636.6p | 136 | -2.3 | 25.7 | 175.0 | 190.0 |

| Lloyds Banking Group (LSE:LLOY) | 105.675p | 46.5 | 7.6 | 39.9 | 146.0 | 126.0 |

Source: ShareScope. Data as at UK market open 22 June 2026. Past performance is not a guide to future performance.

Next shares started 2016 at more than 7,000p but closed at 4,848p in the wake of the Leave vote, for which chief executive Simon Wolfson had been a prominent supporter.

A month later, the retailer reported no appreciable effect on consumer behaviour and said that trading conditions in continental Europe were unlikely to be any different as most of its stock was manufactured outside the EU and already subject to EU customs and tariffs.

Currency hedging limited the near-term impact of the pound’s devaluation, with Next’s initial estimate being that prices would rise by less than 5% in 2017-18.

A disappointing year-end sale period meant shares started 2017 near 4,000p before a steady recovery from 2022 onwards to a record 14,140p and a rise of 156% since the Brexit vote.

BT started 2016 at 467.25p but ended the year down at 366.9p, with the weakening of sterling among the factors impacting on its financial performance during that period.

- Ian Cowie: how I’m investing in space

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

However, chief executive Gavin Patterson told investors in July that the board did not expect the result of the EU referendum to have a significant impact on the company’s outlook.

Since then, BT’s valuation has been hit hard by the pandemic, the cost of dealing with its pension deficit and the capital expenditure requirements of its full-fibre broadband rollout.

Those factors have taken their toll on the dividend, which rose 13% to 14p in annual results the month before the Brexit vote. Chair Michael Rake said confidence in future cash flows meant the board expected dividend growth of at least 10% for the following two years.

By 2018-19 the board has decided to hold the full-year dividend unchanged at 15.4p per share, with the most recent figure for 2025-26 at 8.32p after being cut entirely during Covid.

BT shares were near 100p in 2024 before a recovery to last month’s 225p, a performance mirrored by the wider sector and Vodafone after its shares slumped from 218p on the morning of the Brexit vote to as far as 66p. The mobile phone giant started this week at 107p.

Taylor Wimpey shares slumped from 189.8p on the morning of the EU referendum to 117p a fortnight later, only to fight back over the following year to reach 200p.

Multiple headwinds, including the challenges of planning policy, fire safety provisions and ongoing mortgage affordability concerns, have since weighed on the sector and left Taylor Wimpey outside the FTSE 100 after its shares fell below 80p.

In contrast to housebuilding and property, the aerospace and defence sector has provided shelter for investors after BAE Systems (LSE:BA.) and Rolls-Royce Holdings (LSE:RR.) surged to record highs.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.