Share Sleuth: how I decided which firm to trim to raise cash

While there’s share price momentum, Richard Beddard has almost halved this holding. Here, he explains why.

7th May 2026 10:28

by Richard Beddard from interactive investor

Like last month, this month my trading focus was on holdings I should reduce in size or liquidate. The Share Sleuth portfolio didn’t have enough cash to fund additions.

On Thursday 23 April, the day I designated for trading, Share Sleuth had £3,650 in virtual cash, about 1.7% of its total value. The minimum trade size was nearly 2.5% of the portfolio’s total value, about £5,350 on the day.

- Our Services: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

Shares in the firing line

These were my options:

| # | company | description | score | qual | price | ih% | ss% | ih%-% |

| 25 | Cohort | Manufactures/supplies defence tech, training, consultancy | 6.3 | 8.0 | -1.7 | 2.6% | 5.2% | -2.6% |

| 26 | Bloomsbury Publishing | Publishes books and educational resources | 6.3 | 7.5 | -1.2 | 2.5% | 5.6% | -3.1% |

| 30 | Renishaw | Makes tools and systems for manufacturers | 5.0 | 6.5 | -1.5 | 2.5% | 4.9% | -2.4% |

Click on a share’s score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio, ss% is the actual size of Share Sleuth’s holding, and ih%-% is the difference between ideal and actual sizes.

All these companies are good businesses. Their scores are weighed down by negative price scores, which means they are trading at a relatively high multiple of normalised profit.

The critical column in the table is the last one (ih%-%), which deducts the actual holding size (ss%) from the ideal holding size (ih%) as determined by the share’s score.

Cohort (LSE:CHRT) would have been a marginal decision. The difference between the actual and ideal holding size is 2.6% of the portfolio’s total value, just 0.1% more than the minimum trade size. I have also traded Cohort since I last scored it in September 2025. I added more shares in January and, and I don’t see a pressing need to reverse that decision so soon after I took it.

Bloomsbury Publishing (LSE:BMY) was only a little more clear-cut. It was overweight by 3.1% of the portfolio’s total value, but I have also added shares relatively recently, in early November, after I last scored it in July 2025.

A ‘b’ indicates an addition to the portfolio and an ‘s’ indicates a reduction in the holding. Share Sleuth has held Bloomsbury continuously since 2019.

Since November, Bloomsbury has announced two forthcoming titles from blockbuster author Sarah J. Maas, which means traders are anticipating blockbuster profits in the year to February 2027.

Based on past experience, that is very likely, but we cannot rely on blockbuster profits every year. Taking a long-term perspective, little has changed. We knew the books were in the pipeline, we just didn’t know for sure when they would be published.

I also considered selling shares in near miss Renishaw (LSE:RSW). Its score of 5 made it the lowest-scoring share in the Decision Engine. Relatively speaking, it is the least undervalued share of the 30. Technically, I am least wedded to it.

I treat every company in the portfolio as a forever share, one I’m willing to hold a minimum position in whatever the price. Shares with insufficient scores to justify a 2.5% minimum holding are assigned an ideal holding size of 2.5%.

This prevents me from owning lots of sub-scale holdings. It also means the Decision Engine won’t flag a potential sale to me unless the holding is at least 5% of Share Sleuth’s total value (the minimum holding size plus the minimum trade size). That seems like a big commitment to the shares I’m least confident in.

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

- FTSE 100 ex-dividend dates: May 2026

- Tony Blair Institute’s radical proposal to overhaul state pension

Renishaw was one of those shares. The holding was worth 4.9% of the portfolio’s total value, just 0.1% shy of the 5% required for a 2.5% reduction that would leave me with a 2.5% holding.

Although the Decision Engine was not offering me a trade, a trade seemed like a good idea. Halving the holding would get me to close to the minimum holding size, with close to a minimum trade.

Like Bloomsbury, Renishaw’s profitability varies considerably from year to year, although it is more susceptible to changes in demand than supply.

Renishaw’s machine tools are required by machine manufacturers in cyclical industries such as semiconductors, electronics, aerospace and defence. The company had recently confirmed that it is experiencing strong demand.

This put me in a conundrum. It was very likely Renishaw’s products would come back into demand sooner or later, and it is very probable that demand will subside again at some point in the future. Renishaw generally takes two steps forward and one step backwards.

I had not traded Renishaw since November 2023, so I could not use a recent trade to defend inaction. Instead, I put things off by a day and noted that I would sell half the holding on Friday. Then I slept on the decision.

Reducing Renishaw

On Friday 24 of April, I roughly halved the portfolio’s holding in Renishaw.

The actual price, quoted by a broker, was £44.17, which raised £5,168 after deducting £10 in lieu of fees.

A ‘b’ indicates an addition to the portfolio and an ‘s’ indicates a reduction in the holding. Share Sleuth has held Renishaw continuously since 2015.

That decision may look dubious in the coming months if the share price momentum continues, in which case I should remind you the Decision Engine is not a market timing mechanism. It determines how big the portfolio’s holdings should be based on my evaluation of the capabilities, risks, and strategy of each business.

On 5 May, Renishaw published a third-quarter trading update with more detail. It anticipates record full-year revenue for the year to June 2026 at least 9% ahead of 2025, and a more substantial increase in adjusted profit.

Much of the additional demand for machine tools is from semiconductor manufactures. Some analysts think the semiconductor sector is in a “supercycle” due to investment by hyperscalers (giant cloud computing companies).

Sales of Additive Manufacturing machines have also increased strongly. This is exciting, if it means Additive Manufacturing is developing into a mainstream manufacturing technology as Renishaw expects.

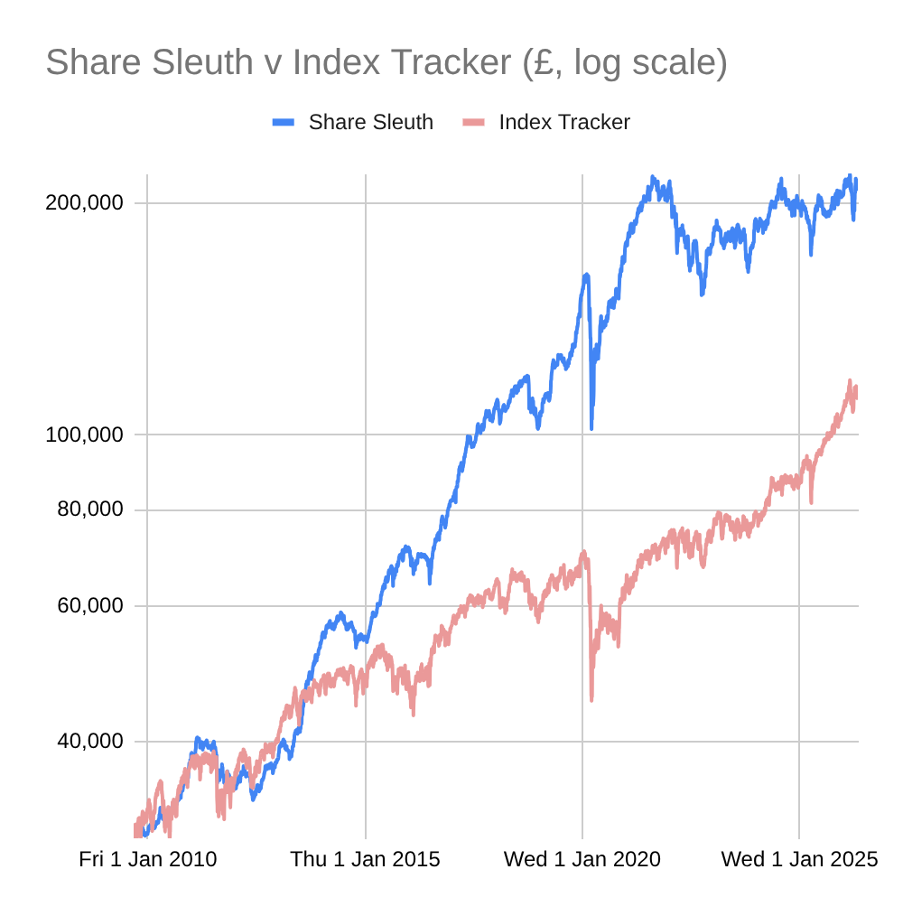

Share Sleuth performance

At the close on Tuesday 5 May, Share Sleuth was worth £209,549, 598% more than the £30,000 of pretend money we started with in September 2009.

The same amount invested in accumulation units of a FTSE All-Share index tracking fund would be worth 111,882, an increase of 273%.

Past performance is not a guide to future performance.

After dividends paid during the month from Goodwin (LSE:GDWN), Quartix Technologies (LSE:QTX) and Volution Group (LSE:FAN), Share Sleuth’s cash pile is £8,873.

The minimum trade size, 2.5% of the portfolio’s value, is £5,239.

| Share Sleuth, 05 May 2026 | Cost (£) | Value (£) | Return (%) | ||

| Cash (4% of portfolio) | 8,873 | ||||

| Current holdings (24 shares) | 200,676 | ||||

| Total, and performance since 9 September 2009 | 30,000 | 209,549 | 598 | ||

| Benchmark: FTSE All-Share index tracker (acc) | 30,000 | 111,882 | 273 | ||

| Companies | Shares | Cost (£) | Value (£) | Return (%) | |

| AMS | Advanced Medical Solutions | 1,965 | 4,503 | 4,706 | 5 |

| ANP | Anpario | 1,124 | 4,057 | 6,013 | 48 |

| BMY | Bloomsbury | 1,882 | 8,354 | 11,254 | 35 |

| BNZL | Bunzl | 417 | 9,798 | 10,200 | 4 |

| BOWL | Hollywood Bowl | 4,002 | 10,348 | 9,825 | -5 |

| CHH | Churchill China | 1,495 | 17,228 | 5,008 | -71 |

| CHRT | Cohort | 836 | 6,315 | 9,681 | 53 |

| FAN | Volution | 830 | 5,151 | 5,005 | -3 |

| FOUR | 4Imprint | 116 | 2,251 | 4,202 | 87 |

| GAW | Games Workshop | 66 | 4,116 | 13,151 | 219 |

| GDWN | Goodwin | 36 | 871 | 4,126 | 374 |

| HWDN | Howden Joinery | 1,476 | 10,371 | 11,291 | 9 |

| JET2 | Jet2 | 822 | 5,211 | 9,174 | 76 |

| LTHM | James Latham | 1,150 | 14,437 | 11,788 | -18 |

| MACF | Macfarlane | 7,689 | 10,011 | 5,075 | -49 |

| OXIG | Oxford Instruments | 505 | 10,044 | 14,716 | 47 |

| PRV | Porvair | 906 | 4,999 | 6,523 | 30 |

| QTX | Quartix | 1,618 | 3,988 | 4,126 | 3 |

| RNWH | Renew Holdings | 1,310 | 9,804 | 11,842 | 21 |

| RSW | Renishaw | 117 | 3,698 | 5,679 | 54 |

| SCT | Softcat | 675 | 9,995 | 9,477 | -5 |

| SOLI | Solid State | 5,009 | 6,033 | 8,515 | 41 |

| TFW | Thorpe (F W) | 6,153 | 14,861 | 15,259 | 3 |

| TUNE | Focusrite | 2,020 | 14,128 | 4,040 | -71 |

Notes

Costs include £10 broker fee, and 0.5% stamp duty where appropriate

Cash earns no interest

Dividends and sale proceeds are credited to the cash balance

Objective: To beat the index tracking fund handsomely over five year periods

Source: ShareScope.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns all the shares in the Share Sleuth portfolio.

For more on the Decision Engine and Share Sleuth, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.