Shares for the future: an attractive small-cap with a resilient core

Analyst Richard Beddard examines a company that’s achieved strong returns and growth – albeit slightly unsteady - in unstable markets.

26th June 2026 15:00

by Richard Beddard from interactive investor

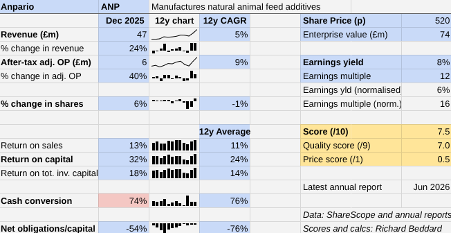

At the AGM last week, Anpario (LSE:ANP), a manufacturer of natural animal feed additives, anticipated revenue of just over £50 million, adjusted EBITDA of £10.3 million. Those numbers would deliver revenue and profit growth of about 7%.

- Our Services: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

It looks like 2026 will be a third consecutive year in which Anpario has stepped forward, a good run for a business that often takes two steps forward and one step back.

Record growth. Record profitability

Higher than normal revenue growth in 2024 (23%) and 2025 (24%) was partly due to the acquisition of Bio-Vet in September 2024.

A US manufacturer of probiotics and electrolytes for ruminants, Bio-Vet contributed £2.2 million of revenue in the last three months of 2024 and £6.7 million in 2025.

Excluding this revenue bump, Anpario’s growth slowed from 16% to 6%, close to the long-term average and the rate Anpario anticipates in 2026.

This normalisation of underlying revenue is unsurprising because 2024 particularly was an exceptional year.

In 2022 and 2023 farmers, who had overstocked due to post-Covid shortages, were shrinking their herds and trading down to less profitable feed additives in response to higher feed and energy costs and African swine flu outbreaks in some regions. Anpario’s revenue contracted by 1% in 2022 and 7% in 2023.

The fixed costs of its factory in Worksop meant profit declined more than revenue. Anpario achieved a 13% after tax return on capital, a decent level of profitability, but its lowest for over a decade.

- What a Burnham premiership could mean for your long-term wealth

- Trading Strategies: an overlooked FTSE 100 stock to consider

In 2024 and 2025 farmers restocked and traded up to more expensive and profitable products. In both years, the company achieved record Return on Capital of more than 20%.

Although this level of volatility was unusual, Anpario’s history is dotted with smaller contractions when its customers, farmers, have endured difficult times.

Through the ups and downs, it has grown revenue and adjusted operating profit at mid to high single-digit CAGRs and remained profitable and cash generative. It has reported a cash surplus at the end of every financial year.

A world of instability

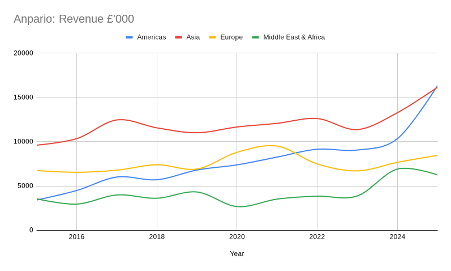

Epidemics and economic woes tend to be regional or restricted to certain species. The impact on Anpario is moderated by global and species diversification.

The company has offices that sell direct or work with distributors in all of the world’s meat-producing regions. Poultry is Anpario’s biggest market, but it also supplies fish and cattle farmers.

Source: Anpario annual reports.

The acquisition of Bio-Vet has accelerated growth in the Americas, already Anpario’s fastest-growing territory. Despite unprecedented Asian growth in 2025, for the first time, the Americas became Anpario’s most lucrative territory by revenue.

Four countries contribute more than 10% of revenue each and more than 50% of revenue together. They are the US, the Philippines, China and the UK. In all but China, Anpario singled out increased sales of Orego-Stim, already its biggest revenue earner, as a major contributor to growth in 2025.

Orego-Stim is a high-margin “premium” product made from oregano oil, which has natural antibiotic and antiparasitic properties.

Anpario deliberately positions itself in the natural animal feed additive market because the science is settled, natural ingredients are safe to use and beneficial to animal health. The company has expertise in sourcing and formulating ingredients, and it demonstrates their effectiveness in collaboration with academics. This means research and development costs are low but the product is differentiated.

Additives are used in low volumes so they can be manufactured centrally and are relatively cheap to ship around the world from Anpario’s factory in Worksop, even when alternative overland routes must be used to avoid choked sea lanes.

- The AIM companies involved in new space race

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

The company’s growth strategies use its expertise and distribution network. For example, Anpario reformulates products for new species and combines ingredients in new ways for existing products.

Anpario’s strong performance in the UK in 2025 was also propelled by Optomega Algae, another premium product. Optomega Algae is an Omega 3 supplement developed as a sustainable alternative to Anpario’s Optomega supplement, which is made from fish oil. The sustainable version is produced from algae grown using natural waste from sugarcane production. The same waste powers the factory.

Orego-Stim is in Anpario’s phytobiotic range. These nutrients control bad microbes in the animal gut. Bio-Vet is a specialist in probiotics and prebiotics. These encourage good gut bacteria.

Anpario is making new combinations and feed protocols by combining phytobiotics with Bio-Vet products. It has already enhanced some Bio-Vet electrolyte formulations to include Orego-Stim.

The company is also introducing Bio-Vet products to its global distribution network. The 2025 annual report says Anpario is close to gaining approval for BioVet’s QuadriCal in a number of new territories. QuadriCal is a calcium supplement for cattle.

Chief executive Richard Edwards oversaw the acquisition spree that assembled Anpario in the years leading up to 2012, but until BioVet in 2024, the company had made no further significant acquisitions.

They do not come easily. Although there are many smaller one or two product companies, they are usually privately held and their owners rarely sell cheaply. Although Anpario had been courting Bio-Vet since 2017, it took seven years and ultimately the death of the founder to seal the deal.

- Sector Screener: do BP shares still have investment potential?

- Bill Ackman talks IPOs, SpaceX and favourite tech stocks

The temptation to overpay may be great, but the time between deals and the fact that Anpario earned a handsome 18% Return on Total Invested Capital (ROTIC) in 2025 (including all acquisitions at cost) strongly suggests Anpario does not.

Generally, Anpario has strong environmental credentials. Natural additives are alternatives to antibiotic growth promoters and toxic chemicals like zinc. They increase the productivity of animals, which increases the efficiency of farms. Healthier animals produce less methane, which is a greenhouse gas.

The company also treats employees well. There is a wide bonus pool and a preference for promoting from within. Opportunities at the top may not come often but when Karen Prior stood down as group finance director in 2021, her replacement was Marc Wilson, who joined in 2010 when he was in his early 20s. Prior remains on the board as corporate responsibility director.

Scoring Anpario

Anpario has achieved strong returns and slightly unsteady growth in unstable markets. This appears to be due to a coherent and conservative long-term strategy. I think it will prosper through thick and thin.

| Anpario | ANP | Manufactures natural animal feed additives | 24/06/2026 | 7.5/10 |

| How capably has Anpario made money? | 2.0 | |||

| Anpario is a highly profitable business formed in a series of acquisitions that ended in 2012. Since then, it has refined feed additive formulations, opened sales offices in the major meat-producing regions and developed online sales. This has brought it modest growth in revenue and profitover the long term. | ||||

| How big are the risks? | 2.0 | |||

| Farming is capricious and demand fluctuates considerably. There are cheap and sometimes nasty substitutes for Anpario’s natural high-quality additives. Fixed costs weigh on profit when revenue falls but are mitigated by decent margins and a strong balance sheet. | ||||

| How fair and coherent is its strategy? | 3.0 | |||

| Natural additives make animals healthier, farms more productive, and replace growth promoters that harm humans. Anpario is an employee and environmentally friendly company. Its strategy is to demonstrate the efficacy of natural additives, introduce new products, and acquire complementary businesses. | ||||

| How low (high) is the share price compared to normalised profit? | 0.5 | |||

| Low. A share price of 520p values the enterprise at £74 million, about 16 times normalised profit. | ||||

| NB: Bold text indicates factors that reduce the score. Bold and italicised text doubly so. The maximum score is 3 for each criterion except price, which has a maximum of 1 (explained here) | ||||

30 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score more than 5 out of 10 to be worthy of long-term investment in sizes determined by the ideal holding size (ihs%).

Autotrader Group (LSE:AUTO) and Oxford Instruments (LSE:OXIG) have published annual reports and are due to be re-scored.

| company | description | score | qual | price | ih% | |

| 1 | FW Thorpe | Makes lighting systems for commercial, industrial and public settings | 9.9 | 9.0 | 0.9 | 9.8% |

| 2 | James Latham | Distributes imported panel products, timber, and laminates | 8.5 | 7.5 | 1.0 | 7.0% |

| 3 | Hollywood Bowl | Operates tenpin bowling centres | 8.4 | 8.0 | 0.4 | 6.7% |

| 4 | Renew | Maintains and improves road, rail, water, and energy infrastructure | 8.1 | 7.5 | 0.6 | 6.2% |

| 5 | Jet2 | Flies people to holiday locations, often on package tours | 8.0 | 7.0 | 1.0 | 6.0% |

| 6 | Porvair | Manufactures filters and laboratory equipment | 7.8 | 8.0 | -0.2 | 5.6% |

| 7 | Howden Joinery | Supplies kitchens and joinery to builders and online to DIYers | 7.8 | 7.0 | 0.8 | 5.5% |

| 8 | Solid State | Manufactures electronic systems and distributes components | 7.7 | 7.0 | 0.7 | 5.5% |

| 9 | Judges Scientific | Acquires and grows businesses that manufacture scientific instruments | 7.5 | 6.5 | 1.0 | 4.9% |

| 10 | Anpario | Manufactures natural animal feed additives | 7.5 | 7.0 | 0.5 | 4.9% |

| 11 | Keystone Law | Operates a network of self-employed lawyers | 7.5 | 7.0 | 0.5 | 4.9% |

| 12 | Auto Trader | Online marketplace for motor vehicles | 7.4 | 6.5 | 0.9 | 4.8% |

| 13 | Bunzl | Distributes essential everyday items consumed by businesses | 7.4 | 7.0 | 0.4 | 4.7% |

| 14 | Volution | Manufacturer of ventilation products | 7.2 | 8.5 | -1.3 | 4.4% |

| 15 | Cake Box | Cake shop franchise and sweet manufacturer | 7.2 | 7.0 | 0.2 | 4.3% |

| 16 | Oxford Instruments | Makes imaging and semiconductor manufacturing systems | 7.1 | 6.5 | 0.6 | 4.3% |

| 17 | Quartix | Supplies vehicle tracking systems to small fleets | 7.1 | 7.0 | 0.1 | 4.3% |

| 18 | Churchill China | Manufactures tableware for restaurants etc. | 7.0 | 6.0 | 1.0 | 4.0% |

| 19 | Focusrite | Designs recording equipment, synthesisers and sound systems | 7.0 | 6.0 | 1.0 | 4.0% |

| 20 | YouGov | Surveys public opinion and conducts market research online | 6.9 | 6.0 | 0.9 | 3.9% |

| 21 | Games Workshop | Designs, makes and distributes Warhammer. Licences IP | 6.7 | 8.5 | -1.8 | 3.5% |

| 22 | Advanced Medical Solutions | Manufactures surgical adhesives, sutures and dressings | 6.7 | 6.5 | 0.2 | 3.5% |

| 23 | Softcat | Sells software and hardware to businesses and public sector | 6.7 | 7.0 | -0.3 | 3.4% |

| 24 | Goodwin | Casts and machines steel and processes minerals for niche markets | 6.7 | 7.5 | -0.8 | 3.3% |

| 25 | Cohort | Manufactures/supplies defence tech, training, consultancy | 6.7 | 8.0 | -1.3 | 3.3% |

| 26 | Macfarlane | Distributes and manufactures protective packaging | 6.5 | 5.5 | 1.0 | 3.0% |

| 27 | Bloomsbury Publishing | Publishes books and educational resources | 6.3 | 7.5 | -1.2 | 2.6% |

| 28 | Tristel | Manufactures hospital disinfectant | 6.0 | 8.0 | -2.0 | 2.5% |

| 29 | 4Imprint | Customises and distributes promotional goods | 5.9 | 8.0 | -2.1 | 2.5% |

| 30 | Renishaw | Makes tools and systems for manufacturers | 4.6 | 6.5 | -1.9 | 2.5% |

Click on a share's score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, and ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns Anpario and many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine and Share Sleuth, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.