Shares for the future: upgrade makes this a top five stock

This company’s ‘buy and build’ strategy is tried and tested, and analyst Richard Beddard has given it extra points. Here’s why it’s one of his favourites.

20th March 2026 15:31

by Richard Beddard from interactive investor

The year to November 2024 was Hooman Javvi’s first year as Porvair (LSE:PRV) chief executive.

In some respects, his predecessor Ben Stocks is a hard act to follow. During Stocks’ 27-year tenure, he focused Porvair on filtration and laboratory equipment generating strong returns and steady growth. But Javvi has taken over a business with a tried and tested strategy.

- Invest with ii: Open an ISA | ISA Investment Ideas | ISA Offers & Cashback

Perhaps all he needs to do is follow it.

Year zero for new broom

2025 was not a vintage year, probably due to the negative impact of belligerent trade policies and war on industry, and the fact that Porvair’s results were not augmented by acquisitions. The company made its first acquisition for two years just after the financial year end.

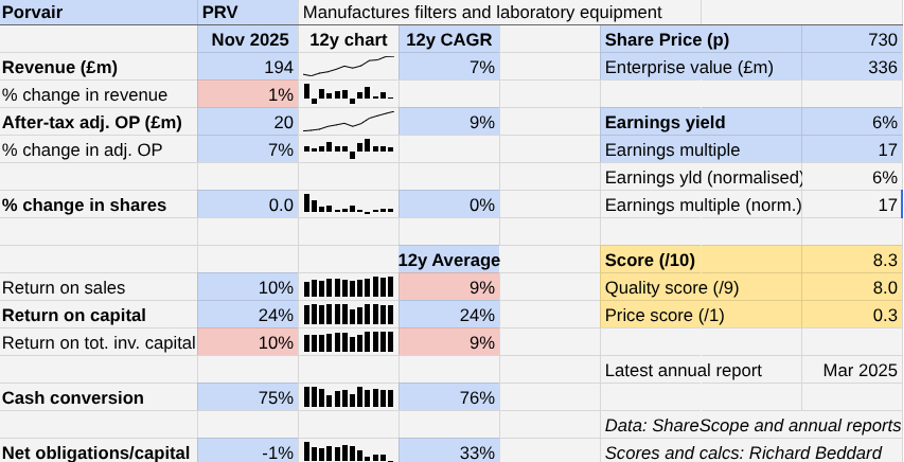

Revenue increased 1%, well below the long-term average of 7%. Profit grew 7%, slightly below the long-term average of 9%. Porvair was as efficient as ever, achieving 24% return on capital and 75% cash conversion.

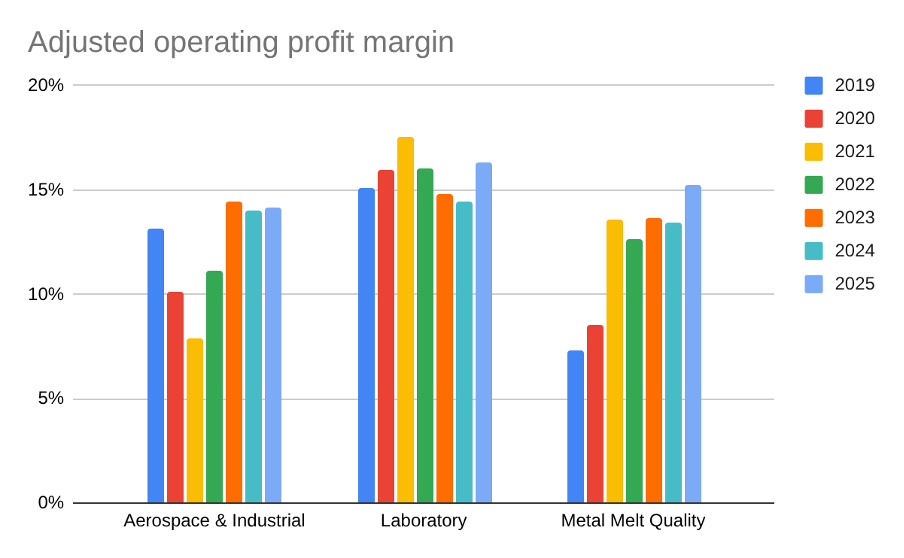

Porvair makes filtration and laboratory equipment. All three divisions were highly profitable but the most impressive improvement in profitability was achieved by the Metal Melt Quality division.

Source: Porvair annual reports.

Metal Melt Quality makes filters used in the production of aluminium and alloys through its subsidiary Selee.

Historically, Selee’s performance has been less reliable than the rest of the business, but new patented filters and high demand for aluminium has lifted the division’s profit margin to the average for the group.

Lightweight and easy to recycle, aluminium is likely to remain in demand as manufacturers focus on sustainability. Electric vehicle manufacturers need it to reduce the weight of their heavy cars. Porvair reports growing demand for aluminium cans as packagers reduce plastic.

After the year end, Porvair acquired Drache for the division, adding a European base to its facilities in the US and Asia. Although it is Porvair’s biggest acquisition in recent times, it is fairly typical: small, complementary and consequently low risk.

Acquisition | Date | Consideration (£m) |

Royal Dahlman | 2019 | 7.15 |

Kbiosystems | 2021 | 6.9 |

Ratiolab | 2023 | 8.1 |

European Filter Corporation | 2023 | 10.3 |

Drache | 2026 | 17.8 |

Source: Porvair annual reports.

Drache’s £17.8 million cost was less than Porvair earned in free cash flow in 2025.

Unless economic conditions deteriorate even more, growth in 2026 seems likely because of the newcomer’s contribution.

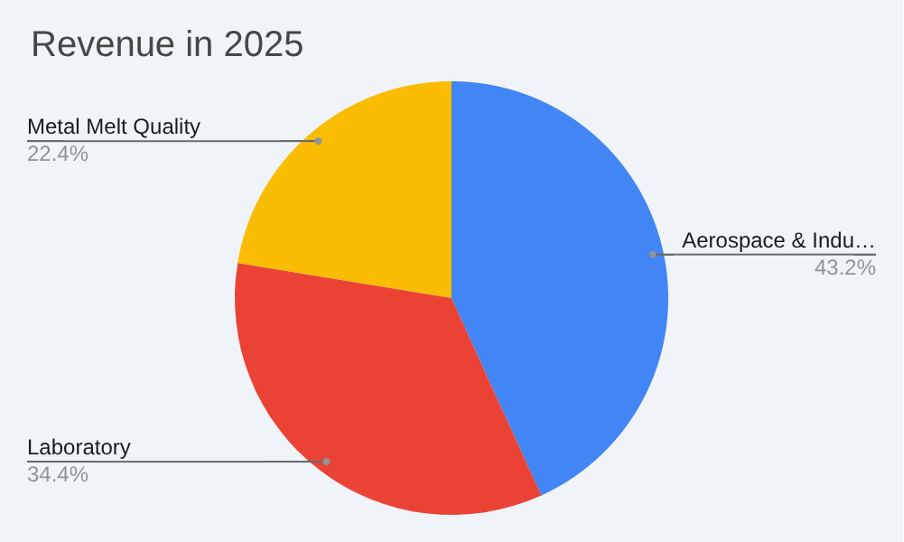

Porvair makes most of its money by manufacturing filters, the primary focus of the biggest of the company’s three business segments, Aerospace and Industrial, and the smallest, Metal Melt Quality:

Source: Porvair annual report 2025.

Filters protect equipment from contaminants in liquids and gases and remove impurities and pollutants. They are designed into aircraft systems like fuel tanks, hydraulics and cooling systems.

Porvair supplies over 200 parts for the Airbus A321XLR, the newest long-range member of the A320 family. They help reduce NOx emissions, fuel burn, and enable the plane to fly with up to 50% Sustainable Aviation Fuel.

Filters are also used in the nuclear, petrochemical, microelectronics and shipping industries.

The Laboratory division is also involved in filtration. It supplies equipment for analysing drinking water, sea water and wastewater, protecting public health and advancing environmental science.

Porvair manufactures filters and other consumables used in the preparation of samples, water analysers and robotic sample handlers.

Risks well mitigated

While heavy industry and aerospace are cyclical industries, filters need to be replaced frequently, either following a regular schedule or, as in the case of aluminium production, after each use.

Because they are consumables, filters generate more reliable revenue than the capital equipment they protect. Because they are designed into equipment, they remain in demand for a long time.

Repeat business can slow down when the economy does, but Porvair has grown fairly consistently. Profit has only contracted once in the last 12 years recorded in my spreadsheet and that was 2020, the first year of the pandemic.

- AIM market winners and losers since Iran war broke out

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

- Stockwatch: hedges and opportunities amid the crisis

Growth has been augmented by self-funded acquisitions. However, Porvair is restricted by the cost, which reduces the after-tax return on total invested capital to 10%. These are specialist businesses that generally do not come particularly cheaply.

Porvair supplies companies producing hydrocarbons (like petrochemicals) or using them (aviation). While governments would like to reduce our reliance on fossil fuels, Porvair makes them cleaner by removing pollutants and improving efficiency.

Other aspects of the business, like molten aluminium filters, are benefiting or are likely to benefit from a more sustainable economy. Potential growth areas include SAF and hydrogen production.

Porvair says tariffs have not yet had a significant effect on the business, even though it rates them the most likely and impactful risk facing the business. This is probably because it manufactures in the US, China and Europe.

Scoring Porvair: tried and tested strategy

The company has reviewed strategy under its new chief executive and aims to build on Porvair’s existing strengths. It will present this strategy to analysts later in the year.

In the meantime, I cannot detect any deviations from the company’s tried and tested buy and build strategy in the update provided in the annual report.

Porvair | PRV | Manufactures filters and laboratory equipment | 18/03/2026 | 8.3/10 |

How capably has Porvair made money? | 2.5 | |||

Porvair has grown revenue and profit at high single-digit CAGRs, by developing better filters and laboratory equipment and acquiring like businesses, which it has self-funded. It has been highly profitable, cash generative, and unencumbered by debt. | ||||

How big are the risks? | 2.5 | |||

The company is under new management.Demand from petrochemicals and related industries may fall if economies wean themselves from fossil fuels, but more opportunities should emerge in, for example, sustainable aviation fuel, hydrogen, nuclear containment, and cleaning up the environment. | ||||

How fair and coherent is its strategy? | 3.0 | |||

Under Porvair’s new CEO, I can detect no significant change in its tried and tested strategy. Buy and build enables Porvair to refocus on markets with the greatest potential, funding acquisitions and product development from reliable cash flow. Low staff turnover indicates it is a good place to work. | ||||

How low (high) is the share price compared to normalised profit? | 0.3 | |||

Low. A share price of 730p values the enterprise at £336 million, about 17 times normalised profit. | ||||

NB: Bold text indicates factors that reduce the score. Bold and italicised text doubly so. The maximum score is 3 for each criterion except price, which has a maximum of 1 (explainedhere) | ||||

Porvair’s “voluntary quit ratio” is 9%, up slightly on 2024, but it suggests that employees stick around. If 9% of staff chose to go each year, typically they stay for over 10 years. That bodes well for the retention of skills in what is a specialist business.

30 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score more than 5 out of 10 to be worthy of long-term investment in sizes determined by the ideal holding size (ihs%).

Howden Joinery Group (LSE:HWDN) and Bunzl (LSE:BNZL) have published annual reports and are due to be re-scored. I am also re-evaluating Softcat (LSE:SCT) and Autotrader Group (LSE:AUTO).

company | description | score | qual | price | ih% | |

1 | FW Thorpe | Makes lighting systems for commercial, industrial and public settings | 9.0 | 0.9 | 9.9% | |

2 | Hollywood Bowl | Operates tenpin bowling centres | 8.0 | 0.6 | 7.3% | |

3 | James Latham | Distributes imported panel products, timber, and laminates | 7.5 | 1.0 | 7.0% | |

4 | Porvair | Manufactures filters and laboratory equipment | 8.3 | 8.0 | 0.3 | 6.6% |

5 | Softcat | Sells software and hardware to businesses and public sector | 7.5 | 0.8 | 6.6% | |

6 | Howden Joinery | Supplies kitchens and joinery products to builders | 7.5 | 0.7 | 6.4% | |

7 | Jet2 | Flies people to holiday locations, often on package tours | 7.0 | 1.0 | 6.0% | |

8 | Renew | Maintains and improves road, rail, water, and energy infrastructure | 7.5 | 0.5 | 6.0% | |

9 | Bunzl | Distributes essential everyday items consumed by organisations | 7.5 | 0.5 | 5.9% | |

10 | Solid State | Manufactures electronic systems and distributes components | 7.0 | 0.9 | 5.9% | |

11 | Auto Trader | Online marketplace for motor vehicles | 7.0 | 0.8 | 5.7% | |

12 | Judges Scientific | Manufactures scientific instruments | 7.0 | 0.8 | 5.6% | |

13 | Churchill China | Manufactures tableware for restaurants etc. | 6.5 | 1.0 | 5.0% | |

14 | Oxford Instruments | Makes imaging and semiconductor manufacturing systems | 6.5 | 0.9 | 4.7% | |

15 | Volution | Manufacturer of ventilation products | 8.5 | -1.2 | 4.5% | |

16 | Advanced Medical Solutions | Manufactures surgical adhesives, sutures and dressings | 6.5 | 0.7 | 4.5% | |

17 | Cake Box | Cake shop franchise and sweet manufacturer | 7.0 | 0.2 | 4.4% | |

18 | Anpario | Manufactures natural animal feed additives | 7.0 | 0.1 | 4.3% | |

19 | Focusrite | Designs recording equipment, synthesisers and sound systems | 6.0 | 1.0 | 4.0% | |

20 | Macfarlane | Distributes and manufactures protective packaging | 6.0 | 1.0 | 4.0% | |

21 | YouGov | Surveys public opinion and conducts market research online | 6.0 | 1.0 | 3.9% | |

22 | Keystone Law | Operates a network of self-employed lawyers | 6.5 | 0.3 | 3.7% | |

23 | Games Workshop | Designs, makes and distributes Warhammer. Licenses IP | 8.5 | -1.7 | 3.7% | |

24 | Bloomsbury Publishing | Publishes books and educational resources | 7.5 | -0.7 | 3.5% | |

25 | Cohort | Manufactures/supplies defence tech, training, consultancy | 8.0 | -1.7 | 2.5% | |

26 | Goodwin | Casts and machines steel and processes minerals for niche markets | 8.5 | -2.2 | 2.5% | |

27 | Quartix | Supplies vehicle tracking systems to small fleets | 7.5 | -1.3 | 2.5% | |

28 | Tristel | Manufactures hospital disinfectant | 8.0 | -2.0 | 2.5% | |

29 | 4Imprint | Customises and distributes promotional goods | 8.0 | -2.1 | 2.5% | |

30 | Renishaw | Makes tools and systems for manufacturers | 6.5 | -1.0 | 2.5% |

Click on a share’s score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, and ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns Porvair and many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine and Share Sleuth, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.