Shares for the future: another good year boosts this firm’s score

A higher score for valuation has nudged this stock four places higher in analyst Richard Beddard’s Decision Engine. That’s despite a big concern about one unavoidable issue.

29th May 2026 15:00

by Richard Beddard from interactive investor

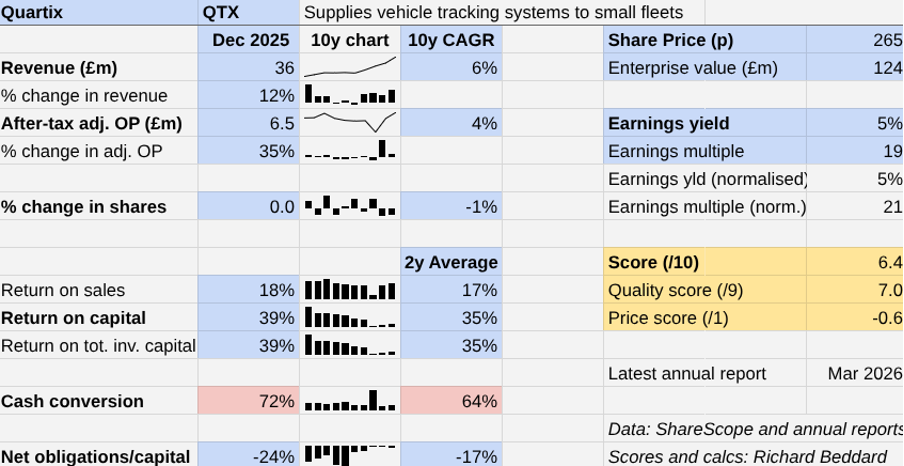

The year to December 2025 was Quartix Technologies’ second good year on the trot, following a wayward period for the vehicle tracker. Revenue increased 12% and adjusted operating profit increased 35% after tax, compared to figures restated in 2024 due to a change in accounting policy.

- Invest with ii: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

Future imperfect

The change requires Quartix to recognise the value of its tracking systems as property plant and equipment rather than recognising the value of the contracts under which they were rented out. This has barely impacted revenue, profit, and cash flow but has had a major impact on Quartix’s balance sheet.

The value of the assets carried is higher, and consequently so is the capital employed by the business. This has reduced capital-based ratios like return on capital.

Historical comparisons with dates before 2024 for these ratios are nonsensical, which is why I have only averaged the last two years in my calculations:

Mercifully, the numbers are still very good. Average return on capital is 35%. Net obligations to capital is still negative, which means the company had more cash than debt of any kind including leases at the year end.

Over the past 10 years, Quartix has grown revenue and profit modestly at mid-single digit compound annual growth rates (CAGR). Its future, though, may not resemble its past.

In the 2010s, there were two strands to the business. Quartix’s biggest revenue stream was the one that remains: subscriptions to a vehicle tracking service for small and medium-sized commercial van fleets.

- Don’t miss the next big IPO: get the latest IPO news and updates straight to your inbox

- Stockwatch: should Taylor Wimpey shares be in your portfolio?

But by 2022, Quartix had substantively stopped selling trackers to the insurance industry via a single large supplier. The trackers were used to monitor new drivers.

Quartix also wasted time and money on a diworsification in 2023. It acquired Konetik, a software business used by fleet operators to decide which electric vehicles to buy based on their tracking data. Quartix bought the business, then decided it had no future and closed it.

Shorn of these complications, Quartix may grow faster. The last two years have been promising.

Recurring revenue

The attraction of commercial fleets is the recurring monthly revenues from subscriptions for as long as the customer uses the service.

Quartix makes it easy for customers to subscribe by providing trackers at no up-front cost and not committing them beyond their initial often two-year term. After the initial term, they pay as they go.

The longer Quartix collects subscriptions, the more profitable it is because the biggest cost is marketing the service on price comparison sites, by telephone, through distributors and field sales in larger markets.

Typically, customers stay with Quartix for seven years. The trackers are small devices made from inexpensive components and assembled in the UK.

The devices send data from vehicles to Quartix’s cloud-based software via mobile networks so owners can monitor fleets in real time on a computer or mobile app. This helps them prevent moonlighting and ensure vehicles are driven safely and economically.

By providing generic devices simple enough to be installed and configured by customers, Quartix keeps costs low, pricing competitive, and still earns a decent profit.

Board concern

My biggest concern remains Quartix’s management. This is not because its three-person board is unimpressive, but because it is probably unsustainable. Part-time executive chair Andy Walters founded the company in 2001, and he is accompanied by two non-executive directors.

A typical board for a listed company, comprising a full-time chief executive, a chief financial officer and maybe others, would increase costs considerably.

Quartix experienced this a few years ago, when Walters, now 70, retired. That experiment quickly unravelled after the ill-fated Konetik acquisition, which precipitated the founder’s return.

Below the PLC board, an operating board runs the company. It is staffed by Quartix loyalists, fronted by Dan Mendis, chief commercial and operating officer and Sally Morton, finance director. The company says it has a succession plan, but we don’t know what it is.

- Aviva shares tipped to boom and dividend grow

- Stockwatch: should you follow Warren Buffett into tech giant?

I’m also keeping an eye on plans to shut down the 2G network, which Quartix’s older units still rely on. Quartix says its network provider will shut off its 2G network in 2029, but doesn’t quantify how many units will need to be replaced with 4G units or units that can roam on other networks.

Quartix is currently bearing the cost of replacing units in France for the same reason, and has previously replaced them in the US. Even though the UK is its biggest market, Quartix expects the impact to be “minimised” by commercially confidential “additional contractual support” from its network provider, and replacing 2G units through customer churn and service upgrades.

The use of the word “minimised” does not reassure me as much as the word “minimal” would!

Overseas growth

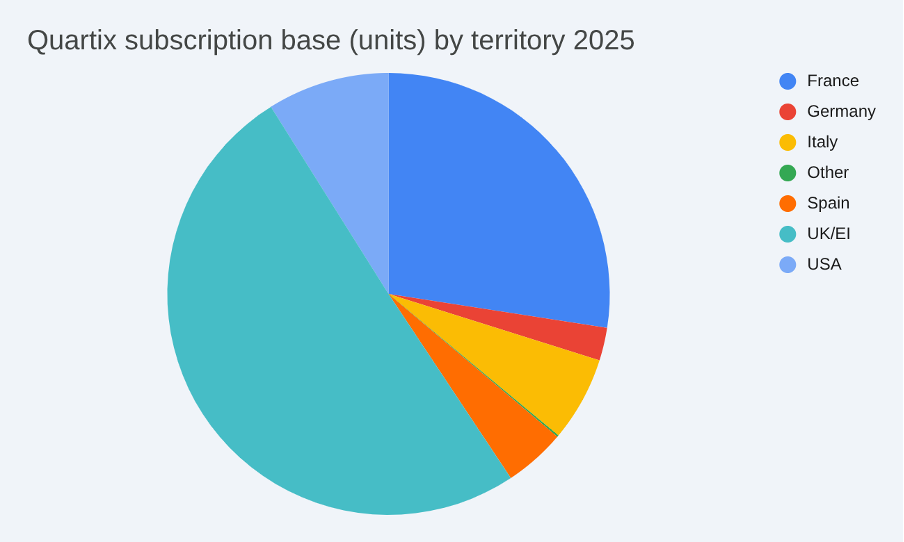

Quartix is still growing in the UK, but it has long looked abroad. It first targeted France in 2010 and has an established business there. More recently, it has entered other European markets and the US.

It has found the US market most challenging, and in 2024 it reversed previous management’s decision to focus its US expansion on field sales in Texas.

This policy contrasted strongly with Quartix’s nationwide and predominantly direct sales model in other countries, and sales contracted. While the US has returned to modest revenue growth, it remains the worst-performing territory. While revenue grew in 2025 due to price rises, the subscription base didn’t grow at all.

Growth in other new markets, Italy, Spain and Germany, is much more encouraging.

Source: Quartix annual report 2025.

Customers used to stick with Quartix for longer, but attrition has increased in recent years, probably because Quartix and its competitors have made trackers easier to install.

Quartix has always relied on winning more business than it loses to grow, but since last year it has pulled on another lever: prices. Until 2024 it had avoided raising prices for its existing user base for fear of losing customers.

The company’s aim for each year is to earn 100% of the Annualised Recurring Revenue from its subscription base at the beginning of the year, so each new additional unit contributes to growth.

Although it hasn’t quite got there, it is moving in the right direction. In 2024, it achieved 95.7% of NRR (Net Revenue Retention). In 2025, it achieved 98.1%.

Scoring Quartix

Glass half-full: Quartix grows faster now it has focused on what it does best - fleet subscriptions.

Glass half-empty: the low-cost board gives way to a conventional one, costs rise again and the company loses focus.

| Quartix | QTX | Supplies vehicle-tracking systems to small fleets | 27/05/2026 | 6.4/10 |

| How capably has Quartix made money? | 2.0 | |||

| In the four years since Quartix exited the insurance market and a subsequent diworsification, it has focused on its biggest and most reliable market: renting vehicle trackers to small and medium-sized commercial fleets. Revenue and profit have grown at mid-single digit CAGRs. | ||||

| How big are the risks? | 2.0 | |||

| A skeleton board lowers costs, but Quartix has no succession plan. Unit attrition rates have risen in recent years, maybe due to increased competition. Quartix does not expect the shutdown of the UK 2G network will require it to replace units “in the foreseeable future” but it will incur costs when it does. | ||||

| How fair and coherent is its strategy? | 3.0 | |||

| By focusing on a simple, generic, configurable and self-installable product, Quartix keeps costs low. It is rolling out its system using direct marketing and price comparison sites across Europe and in the US, where it has been operating less long, and has lower market share than in the still-growing UK. | ||||

| How low (high) is the share price compared to normalised profit? | -0.6 | |||

| High. A share price of 265p values the enterprise at £124 million, about 21 times normalised profit. | ||||

| NB: Bold text indicates factors that reduce the score. Bold and italicised text doubly so. The maximum score is 3 for each criterion except price, which has a maximum of 1 (explained here) | ||||

I last scored Quartix in September 2025.

30 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score more than 5 out of 10 to be worthy of long-term investment in sizes determined by the ideal holding size (ihs%).

Judges Scientific and Keystone Law Group Ordinary Shares have published annual reports and are due to be re-scored.

| 0 | company | description | score | qual | price | ih% |

| 1 | FW Thorpe | Makes lighting systems for commercial, industrial and public settings | 9.9 | 9.0 | 0.9 | 9.8% |

| 2 | Hollywood Bowl | Operates tenpin bowling centres | 8.6 | 8.0 | 0.6 | 7.1% |

| 3 | James Latham | Distributes imported panel products, timber, and laminates | 8.5 | 7.5 | 1.0 | 7.0% |

| 4 | Renew | Maintains and improves road, rail, water, and energy infrastructure | 8.0 | 7.5 | 0.5 | 6.0% |

| 5 | Jet2 | Flies people to holiday locations, often on package tours | 8.0 | 7.0 | 1.0 | 6.0% |

| 6 | Auto Trader | Online marketplace for motor vehicles | 7.9 | 7.0 | 0.9 | 5.9% |

| 7 | Solid State | Manufactures electronic systems and distributes components | 7.9 | 7.0 | 0.9 | 5.8% |

| 8 | Howden Joinery | Supplies kitchens and joinery products to builders | 7.8 | 7.0 | 0.8 | 5.6% |

| 9 | Porvair | Manufactures filters and laboratory equipment | 7.8 | 8.0 | -0.2 | 5.5% |

| 10 | Bunzl | Distributes essential everyday items consumed by businesses | 7.6 | 7.0 | 0.6 | 5.1% |

| 11 | Judges Scientific | Manufactures scientific instruments | 7.5 | 7.0 | 0.5 | 5.0% |

| 12 | Cake Box | Cake shop franchise and sweet manufacturer | 7.2 | 7.0 | 0.2 | 4.3% |

| 13 | Volution | Manufacturer of ventilation products | 7.1 | 8.5 | -1.4 | 4.2% |

| 14 | Advanced Medical Solutions | Manufactures surgical adhesives, sutures and dressings | 7.1 | 6.5 | 0.6 | 4.2% |

| 15 | Churchill China | Manufactures tableware for restaurants etc. | 7.0 | 6.0 | 1.0 | 4.0% |

| 16 | Focusrite | Designs recording equipment, synthesisers and sound systems | 7.0 | 6.0 | 1.0 | 4.0% |

| 17 | Oxford Instruments | Makes imaging and semiconductor manufacturing systems | 7.0 | 6.5 | 0.5 | 4.0% |

| 18 | YouGov | Surveys public opinion and conducts market research online | 7.0 | 6.0 | 1.0 | 3.9% |

| 19 | Softcat | Sells software and hardware to businesses and public sector | 6.9 | 7.0 | -0.1 | 3.9% |

| 20 | Goodwin | Casts and machines steel and processes minerals for niche markets | 6.9 | 7.5 | -0.6 | 3.7% |

| 21 | Games Workshop | Designs, makes and distributes Warhammer. Licences IP | 6.7 | 8.5 | -1.8 | 3.5% |

| 22 | Cohort | Manufactures/supplies defence tech, training, consultancy | 6.5 | 8.0 | -1.5 | 3.1% |

| 23 | Macfarlane | Distributes and manufactures protective packaging | 6.5 | 5.5 | 1.0 | 3.0% |

| 24 | Quartix | Supplies vehicle tracking systems to small fleets | 6.4 | 7.0 | -0.6 | 2.7% |

| 25 | Anpario | Manufactures natural animal feed additives | 6.3 | 7.0 | -0.7 | 2.7% |

| 26 | Keystone Law | Operates a network of self-employed lawyers | 6.3 | 6.5 | -0.2 | 2.7% |

| 27 | Bloomsbury Publishing | Publishes books and educational resources | 6.2 | 7.5 | -1.3 | 2.5% |

| 28 | Tristel | Manufactures hospital disinfectant | 6.0 | 8.0 | -2.0 | 2.5% |

| 29 | 4Imprint | Customises and distributes promotional goods | 5.8 | 8.0 | -2.2 | 2.5% |

| 30 | Renishaw | Makes tools and systems for manufacturers | 4.5 | 6.5 | -2.0 | 2.5% |

Click on a share's score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, and ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns Quartix and many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine and Share Sleuth, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.