Shares for the future: no quick and emphatic recovery here

There’s no doubt this former favourite is a good company, but it’s just slipped five places down analyst Richard Beddard’s list after he cut its score.

22nd May 2026 14:58

by Richard Beddard from interactive investor

Pretty much as Churchill Chinawarned last summer and confirmed in February, revenue for the year to December 2025 fell 3%, and profit fell by 31%. It was the third consecutive year that revenue fell modestly. It was the second year profit declined substantially.

- Invest with ii: Open a Stocks & Shares ISA | ISA Investment Ideas | Transfer a Stocks & Shares ISA

What a bad year looks like

Kudos to the company for telling it as it was in July. Churchill’s chief financial officer told me his projections were realistic because the company did not want to return with another warning before the year end.

The contraction has had a severe impact on the financial ratios I use to judge businesses.

Churchill’s profit margin, which had not yet returned to pre-pandemic highs, was 6% in 2025, below the 12-year average, and return on capital was half the average. At 7%, it was the second-lowest figure for the period after the pandemic year of 2020.

Cash conversion was well above average enabling the company to maintain its net cash position.

Normally, investment in equipment and payment to fund the company’s pension scheme mean cash flow lags profit substantially, but the pension scheme is in surplus and no longer requires funding.

- Trading Strategies: is BAE Systems overvalued after 270% rally?

- The risks and rewards of investing in ‘hot’ themes

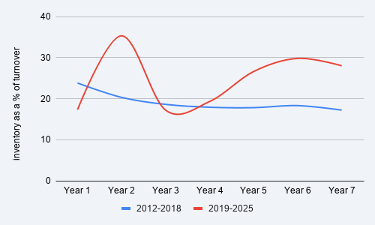

Although Churchill has continued to invest in equipment to improve efficiency and automation, it raised cash by selling more tableware from burgeoning stock.

Cash flow is welcome, but the reduction in stock contributed to lower return on capital because Churchill made less tableware, which reduced the efficiency of the factory.

Still high inventory levels must be funded, which adds to capital employed, also reducing the return on capital ratio.

Source: Churchill China annual reports 2012-2025

After a very volatile period during the pandemic, inventories may be stabilising at just below 30% of turnover (the tail of the red line in the chart). During the pre-pandemic period (blue line, and the first datapoint on the red line) inventory was generally just below 20% of turnover.

I wonder if this is due to post-Brexit and post-pandemic trade friction. Perhaps there is an ongoing requirement to hold more stock, particularly in the company’s European distribution centre.

Hospitality permacrisis

Churchill China is caught between a rock and a hard place. It specialises in manufacturing tableware for restaurants and pubs. The hospitality industry was booming before the pandemic but has been in something of a “permacrisis” since, due to the rising cost of food, energy, and pay.

Fewer customers are investing in new installations, making Churchill more reliant on replacement products. This has reduced manufacturing volumes and made it harder to raise prices.

Churchill also shares some of the challenges of its customers, principally rising energy and wage bills. A price increase of 2.9% introduced at the end of 2025, was not matched by a 6% increase in the wage bill propelled by increases in the national minimum wage and national insurance last April.

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

- Tax burden on pensioners surges: how to cut your bill

War in the Middle East has brought energy costs to the fore again. The company is gradually electrifying its plant and equipment, and over the next two years it has hedged most of its gas costs.

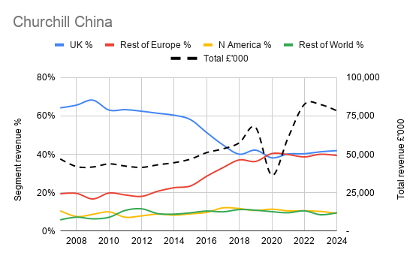

Churchill has a large market share in the UK, where it earns about 40% of revenue, and sees Europe, where it has a smaller share of a bigger market and already earns about 40% of revenue, as its main growth opportunity.

Before the pandemic, the results from Europe justified that view, but since 2020, Europe has not grown either.

Judging by last year, a trading update may be imminent, but I think a speedy recovery is unlikely. Churchill has cut its final dividend almost by half compared to the previous year and the company’s broker is forecasting a very modest increase in revenue in 2025.

Demand has picked up overseas, where current tariff regimes in the US and EU benefit Churchill China because they penalise imports from China and the Far East more.

Economic conditions in the UK, where the company earns about 40% of revenue, are less promising, and the company’s Furlong Mills subsidiary, which supplies Churchill and other potteries, has lost a customer to another supplier.

Furlong Mills was responsible for 8% of revenue in 2025.

Quality and service

Churchill China’s success has come from a technically superior product, and its ability to deliver it quickly.

It uses a proprietary manufacturing process that protects the pattern under the glaze, making the plate highly durable and relatively cheap to produce. The process is dependent on clays sourced in Britain and processed by Furlong Mills, which Churchill says also gives it a technical advantage. The benefit to customers is low lifetime cost of ownership.

The hospitality market is attractive because commercial kitchens are tough environments. Tableware is washed many times a day and the installed base needs to be topped up regularly with replacements due to breakages or expansion.

Churchill sells to hundreds of distributors around the world. It keeps them happy by maintaining enough stock to supply them within 48 hours. 70% of orders from the European distribution centre in Rotterdam were supplied within 24 hours in 2025.

As well as targeting Europe, Churchill’s long-established strategy has increased the contribution of “added value” coloured and textured plates to sales because this is its most differentiated product.

By investing in machinery to automate production and improve efficiency, it can reduce prices to encourage customers to upgrade from standard cheaper-still “whiteware” (which it also sells).

- Stockwatch: time to nibble at two cyclical shares

- British Land’s ‘compelling fundamentals’ imply big upside

Showing there are no easy options in a difficult market, Churchill China boosted factory activity by making more retail tableware in 2025. Retail tableware is less profitable though, and even at the elevated levels of 2025, retail only contributed 4% of total revenue.

Another, to my mind suboptimal, route back to growth is the distribution of complementary non-ceramic products mooted in the annual report this year. It may not be a misstep. There is logic in making better use of Churchill’s distribution network, and the company has long sold complementary products such as glassware and cutlery.

Churchill has mooted the acquisition of these businesses in this year’s annual report and I fear diworsification. We have experienced this at Churchill China’s neighbour, Portmeirion, a manufacturer of retail tableware that has not managed to add value to its distribution network by, for example, acquiring scented candle manufacturer Wax Lyrical.

Semi-vitrified business

Vitrification hardens plates, and I had hoped Churchill China’s business was as vitrified as the product. While events have proved otherwise, I do not discount its staying power and recovery potential.

Churchill had no debt at the year-end (or any other recent year-end) and it is committed to maintaining a “strong unencumbered balance sheet”. Although the company has not maintained return on capital at the arbitrary level that satisfies me, it can profit through thick and thin (8% after tax), 2025 was a near miss (7%).

Every time I go to a restaurant I check the tableware. As often as not, it is made by Churchill China. Its UK market leadership is testament to past success.

Everything I know about the company indicates it is run for the long term. That extends to its attitude towards employees. Churchill says it gives them the space to develop and grow, which may explain why the average length of service is just shy of 12 years.

This proprietorial approach no doubt stems from the ownership of the Roper family, which is still represented on the board by sales and marketing director James Roper. He owns 8% of the shares. Another family member owns 7%. The Ropers have been heavily involved since Edward Roper became managing director in 1922.

Scoring Churchill China

I appreciate the product and Churchill’s ethos, but this year’s results suggest there are no easy levers to pull for a quick and emphatic recovery.

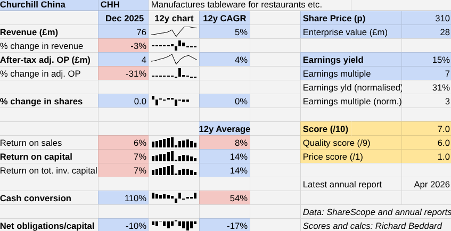

| Churchill China | CHH | Manufactures tableware for restaurants etc. | 20/05/2026 | 7/10 |

| How capably has Churchill China made money? | 1.5 | |||

| A proprietary manufacturing process enables Churchill to make durable attractive tableware cheaply. Since 2020, volatile revenue and cost inflation have eaten into profitability, resulting in low single-digit 12-year growth in revenue and profit. Return on capital dropped below 8% in 2025. | ||||

| How big are the risks? | 2.0 | |||

| Churchill China has no debt, experienced management and a vertically integrated supply chain. It is the UK market leader, so sales and profits are closely tied to the economy. Until 2020, Churchill was growing rapidly in Europe, but growth has stalled there too. It may be recovering. | ||||

| How fair and coherent is its strategy? | 2.5 | |||

| The big opportunity is Europe, because it is a much bigger market than the UK. Churchill is focusing investment on people, technology and maintaining high stock availability. Additionally, it may distribute more non-ceramic products, which could be a distraction. Employees are loyal. | ||||

| How low (high) is the share price compared to normalised profit? | 1.0 | |||

| Low. A share price of 310p values the enterprise at £28 million, about 3 times normalised profit. | ||||

| NB: Bold text indicates factors that reduce the score. Bold and italicised text doubly so. The maximum score is 3 for each criterion except price, which has a maximum of 1 (explained here) | ||||

30 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score more than 5 out of 10 to be worthy of long-term investment in sizes determined by the ideal holding size (ihs%).

Judges Scientific, Quartix Technologies and Keystone Law Group Ordinary Shares have published annual reports and are due to be re-scored.

| company | description | score | qual | price | ih% | |

| 1 | FW Thorpe | Makes lighting systems for commercial, industrial and public settings | 9.9 | 9.0 | 0.9 | 9.8% |

| 2 | Hollywood Bowl | Operates tenpin bowling centres | 8.6 | 8.0 | 0.6 | 7.2% |

| 3 | James Latham | Distributes imported panel products, timber, and laminates | 8.5 | 7.5 | 1.0 | 7.0% |

| 4 | Renew | Maintains and improves road, rail, water, and energy infrastructure | 8.1 | 7.5 | 0.6 | 6.1% |

| 5 | Jet2 | Flies people to holiday locations, often on package tours | 8.0 | 7.0 | 1.0 | 6.0% |

| 6 | Porvair | Manufactures filters and laboratory equipment | 8.0 | 8.0 | 0.0 | 6.0% |

| 7 | Solid State | Manufactures electronic systems and distributes components | 7.9 | 7.0 | 0.9 | 5.8% |

| 8 | Howden Joinery | Supplies kitchens and joinery products to builders | 7.9 | 7.0 | 0.9 | 5.7% |

| 9 | Auto Trader | Online marketplace for motor vehicles | 7.8 | 7.0 | 0.8 | 5.6% |

| 10 | Softcat | Sells software and hardware to businesses and public sector | 7.6 | 7.0 | 0.6 | 5.1% |

| 11 | Bunzl | Distributes essential everyday items consumed by businesses | 7.5 | 7.0 | 0.5 | 5.1% |

| 12 | Goodwin | Casts and machines steel and processes minerals for niche markets | 7.5 | 7.5 | 0.0 | 5.0% |

| 13 | Judges Scientific | Manufactures scientific instruments | 7.3 | 7.0 | 0.3 | 4.6% |

| 14 | Volution | Manufacturer of ventilation products | 7.3 | 8.5 | -1.2 | 4.6% |

| 15 | Oxford Instruments | Makes imaging and semiconductor manufacturing systems | 7.2 | 6.5 | 0.7 | 4.4% |

| 16 | Cake Box | Cake shop franchise and sweet manufacturer | 7.2 | 7.0 | 0.2 | 4.3% |

| 17 | Advanced Medical Solutions | Manufactures surgical adhesives, sutures and dressings | 7.1 | 6.5 | 0.6 | 4.2% |

| 18 | Churchill China | Manufactures tableware for restaurants etc. | 7.0 | 6.0 | 1.0 | 4.0% |

| 19 | Focusrite | Designs recording equipment, synthesisers and sound systems | 7.0 | 6.0 | 1.0 | 4.0% |

| 20 | Cohort | Manufactures/supplies defence tech, training, consultancy | 7.0 | 8.0 | -1.0 | 3.9% |

| 21 | YouGov | Surveys public opinion and conducts market research online | 7.0 | 6.0 | 1.0 | 3.9% |

| 22 | Games Workshop | Designs, makes and distributes Warhammer. Licenses IP | 6.8 | 8.5 | -1.7 | 3.5% |

| 23 | Macfarlane | Distributes and manufactures protective packaging | 6.5 | 5.5 | 1.0 | 3.0% |

| 24 | Bloomsbury Publishing | Publishes books and educational resources | 6.5 | 7.5 | -1.0 | 3.0% |

| 25 | Anpario | Manufactures natural animal feed additives | 6.4 | 7.0 | -0.6 | 2.8% |

| 26 | Keystone Law | Operates a network of self-employed lawyers | 6.2 | 6.5 | -0.3 | 2.5% |

| 27 | Tristel | Manufactures hospital disinfectant | 6.0 | 8.0 | -2.0 | 2.5% |

| 28 | Quartix | Supplies vehicle tracking systems to small fleets | 5.9 | 7.5 | -1.6 | 2.5% |

| 29 | 4Imprint | Customises and distributes promotional goods | 5.9 | 8.0 | -2.1 | 2.5% |

| 30 | Renishaw | Makes tools and systems for manufacturers | 4.7 | 6.5 | -1.8 | 2.5% |

Click on a share's score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, and ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns Churchill China shares, and many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine and Share Sleuth, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.