Shares for the future: is this market leader worth it?

This FTSE 250 company makes most of its money in America where it is the biggest of its kind. Analyst Richard Beddard assesses the business and its valuation.

1st May 2026 15:01

by Richard Beddard from interactive investor

Revenue at promotional goods manufacturer 4imprint Group (LSE:FOUR) fell by 2% in the year to December 2025. Barring the pandemic year of 2020, it is the only fall in revenue in more than a decade. It bucked a growth trend that started when the company launched its direct sales business in 1987.

- Invest with ii: Top UK Shares | Share Prices Today | Open a Trading Account

Rare contraction

There was a 3% decline in orders in the year to December 2025 due to the impact of tariff uncertainty and weak business confidence in North America, where it earns 98% of revenue. Orders from existing customers were flat, and orders from new customers declined 12%.

Otherwise, profit margins, while modest as we might expect for a high-volume business, remained high by historical standards, leading to a 2% decline in adjusted profit and very high returns on capital. Strong cash conversion meant the company maintained its large cash surplus.

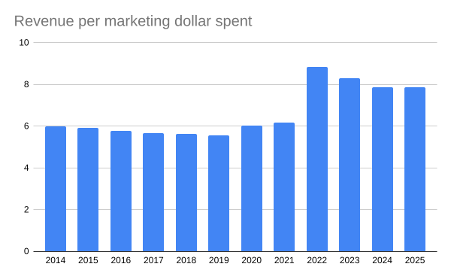

The growth in profitability in the last four years is in part due to sharp increase in revenue per marketing dollar spent. This leaped as the economy emerged from the pandemic and has persisted longer than a bounce-back theory would explain.

4imprint’s 2022 annual report explained that the reorientation of its marketing strategy was responsible.

The company is famous for its trademarked Blue Boxes of samples and catalogues, which it still sends to marketing people at businesses, charities, and other organisations.

In 2022, though, it refocused on advertising the 4imprint brand on Google and TV. In 2024, it added streaming TV to the mix. Today, its marketing spend is heavily weighted to these channels.

This shift was accelerated by the lower cost of TV advertising during the pandemic, but it is also probably a natural outcome of 4imprint’s growth. In 2022, 4imprint earned more than $1 billion (£735.4 million) for the first time. It could afford to embrace the relatively high cost of mass marketing.

- Stockwatch: this heavily shorted FTSE 100 share now offers value

- Bank of England holds rates but prospect of hikes loom

- Trading Strategies: are Rio Tinto shares worth buying now?

The company owes its scale to its business model developed by current chief executive Kevin Lyons-Tarr. The direct marketing model barely involves 4imprint in importing, customising and delivering products.

It is a marketplace, connecting marketeers to suppliers, businesses that acquire blank products, imprint them with logos and slogans, and ship them directly to 4imprint’s customers.

Typically, the customised blanks are items such as clothing, bags, mugs, and stationery. The fastest growing of 4imprint’s major product categories was outdoor and leisure in 2025, which includes hand fans, golf balls, blankets and chairs. The biggest contraction was in mugs and water bottles.

Tariff impact postponed

One of the surprises of 2025 is that profit margins remained at the elevated levels of the previous few years. This may be temporary despite the imposition of tariffs on imports into the US early in 2025. 4imprint explains that it’s mostly-US based suppliers phased in price increases later than expected.

The impact on 2025 was modest, but additional increases this year, and the potential for more, muddies the outlook for 2026. Tariff uncertainty weakens business confidence, which may mean 4imprint cannot recover all the increased cost from its customers.

The company says orders for January and February 2026 were down slightly on the same months in 2025, and the consensus of four forecasts in data site ShareScope anticipates another 2% decline in revenue and a much bigger decline in profit (more than 20%).

Some good news: 4imprint has strong supplier relationships. Over 90% of its annual spend in 2025 went to suppliers it has worked with for over 20 years. They have started shifting their sourcing as the US has embraced tariffs. In 2025, 50% of 4imprint’s revenue was manufactured in China versus about 60% in prior years. The shift was mostly to other Asian countries.

It is unclear how much further the industry can go. Tariffs have been wielded unpredictably on countries, so nowhere appears safe, and some product categories like clothing and bags can be sourced more readily than others, like drinkware.

AI spectre

More speculatively, as a middleman, 4imprint may be threatened by the development of AI.

The company says it has not experienced any disruption from new entrants enabled by AI technology or by the adoption by customers of chatbots to search for promotional goods.

I am only modestly concerned about the first possibility. If AI can improve how middlemen sell promotional goods, I would expect 4imprint to be an early adopter.

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

- Prepare for UK bank sector dividend windfall

- Utilities sector booming as fundraising questions answered

The willingness of people to search the internet for products using chatbots, means we should probably take the risk that they will be less bound to 4imprint seriously.

Strategy

4imprint is the largest distributor of promotional goods in the North American market. Its strategy is to increase market share organically, which hitherto it has achieved through slick IT systems and an employee-focused culture.

A major employer in its hometown of Oshkosh, Wisconsin, 4imprint daubs its promotional materials with images of happy workers and the products they recommend. It pays median total remuneration of $57,300, and chief executive Kevin Lyons-Tarr earns a not fanciful 11.5 times that. The company tells me total staff attrition was just 8%.

4imprint’s “Golden Rule” is to “treat others as you would wish to be treated yourself” and it guarantees on-time delivery, lowest price, and satisfaction. It also guides customers to “Better Choices”, by which it means more sustainable products, sometimes own-brands created in partnership with suppliers.

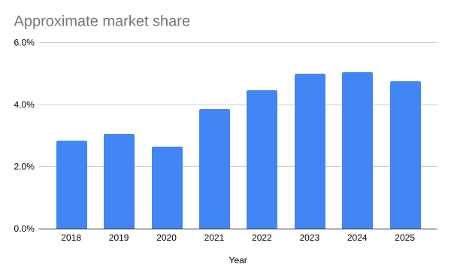

This year’s results cast a little shade on 4imprint’s ability to grow market share through thick and thin though. The company estimates the US and Canadian market was worth about $27.7 billion in 2025, giving it a market share of nearly 5%. Most years, the comparison of North American revenue to the market goes up, but in 2025 the market grew by nearly 5% while 4imprint’s revenue slipped 2%.

This is disappointing because I expect strong companies to gain market share when times are tough, and I cannot find an explanation in 4imprint’s annual report. When the market contracted during the first year of the pandemic, 4imprint’s market share also contracted.

Scoring 4imprint: quality at a price

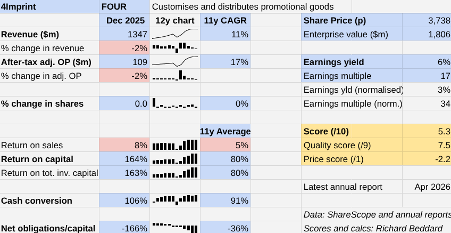

4imprint | FOUR | Customises and distributes promotional goods | 30/04/2026 | 5.8/10 |

How capably has 4imprint made money? | 3.0 | |||

4imprint has grown revenue and profit at double-digit compound annual growth rates (CAGRs) by pioneering direct sales of promotional goods in the US under the constant leadership of CEO Kevin Lyons-Tarr. Its scale is testimony to its success. | ||||

How big are the risks? | 2.0 | |||

4imprint’s fortunes are largely in its own hands. International trade restrictions have reduced customer confidence and tariffs are forcing 4imprint’s suppliers to source products elsewhere, testing the flexibility of its supply chain. The use of AI to find products may reduce its appeal. | ||||

How fair and coherent is its strategy? | 3.0 | |||

4imprint is an archetypal customer and employee-centric business. It gets more efficient as it scales up as marketing and IT costs are spread more thinly. Close relationships with suppliers should help it source products more sustainably. A decline in market share in 2025 is unsettling. | ||||

How low (high) is the share price compared to normalised profit? | -2.2 | |||

High. A share price of 3,738p values the enterprise at $1,806 million, about 34 times normalised profit. | ||||

NB: Bold text indicates factors that reduce the score. Bold and italicised text doubly so. The maximum score is 3 for each criterion except price, which has a maximum of 1 (explainedhere) | ||||

30 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score more than 5 out of 10 to be worthy of long-term investment in sizes determined by the ideal holding size (ihs%).

Judges Scientific (LSE:JDG) and Quartix Technologies (LSE:QTX) have published annual reports and are due to be re-scored.

company | description | score | qual | price | ih% | |

1 | FW Thorpe | Makes lighting systems for commercial, industrial and public settings | 9.0 | 0.9 | 9.9% | |

2 | Hollywood Bowl | Operates tenpin bowling centres | 8.0 | 0.6 | 7.2% | |

3 | James Latham | Distributes imported panel products, timber, and laminates | 7.5 | 1.0 | 7.0% | |

4 | Porvair | Manufactures filters and laboratory equipment | 8.0 | 0.3 | 6.6% | |

5 | Goodwin | Casts and machines steel and processes minerals for niche markets | 7.5 | 0.6 | 6.2% | |

6 | Renew | Maintains and improves road, rail, water, and energy infrastructure | 7.5 | 0.6 | 6.1% | |

7 | Jet2 | Flies people to holiday locations, often on package tours | 7.0 | 1.0 | 6.0% | |

8 | Solid State | Manufactures electronic systems and distributes components | 7.0 | 0.9 | 5.8% | |

9 | Howden Joinery | Supplies kitchens and joinery products to builders | 7.0 | 0.8 | 5.6% | |

10 | Auto Trader | Online marketplace for motor vehicles | 7.0 | 0.8 | 5.6% | |

11 | Softcat | Sells software and hardware to businesses and public sector | 7.0 | 0.6 | 5.3% | |

12 | Bunzl | Distributes essential everyday items consumed by businesses | 7.0 | 0.5 | 5.1% | |

13 | Churchill China | Manufactures tableware for restaurants etc. | 6.5 | 1.0 | 5.0% | |

14 | Judges Scientific | Manufactures scientific instruments | 7.0 | 0.5 | 4.9% | |

15 | Oxford Instruments | Makes imaging and semiconductor manufacturing systems | 6.5 | 0.7 | 4.5% | |

16 | Cake Box | Cake shop franchise and sweet manufacturer | 7.0 | 0.2 | 4.4% | |

17 | Volution | Manufacturer of ventilation products | 8.5 | -1.4 | 4.3% | |

18 | Focusrite | Designs recording equipment, synthesisers and sound systems | 6.0 | 1.0 | 4.0% | |

19 | YouGov | Surveys public opinion and conducts market research online | 6.0 | 1.0 | 3.9% | |

20 | Games Workshop | Designs, makes and distributes Warhammer. Licenses IP | 8.5 | -1.7 | 3.5% | |

21 | Advanced Medical Solutions | Manufactures surgical adhesives, sutures and dressings | 6.5 | 0.2 | 3.4% | |

22 | Keystone Law | Operates a network of self-employed lawyers | 6.5 | 0.2 | 3.3% | |

23 | Anpario | Manufactures natural animal feed additives | 7.0 | -0.3 | 3.3% | |

24 | Cohort | Manufactures/supplies defence tech, training, consultancy | 8.0 | -1.4 | 3.2% | |

25 | Macfarlane | Distributes and manufactures protective packaging | 5.5 | 1.0 | 3.0% | |

26 | Bloomsbury Publishing | Publishes books and educational resources | 7.5 | -1.1 | 2.8% | |

27 | Tristel | Manufactures hospital disinfectant | 8.0 | -2.1 | 2.5% | |

28 | Quartix | Supplies vehicle tracking systems to small fleets | 7.5 | -1.6 | 2.5% | |

29 | 4imprint | Customises and distributes promotional goods | 5.8 | 8.0 | -2.2 | 2.5% |

30 | Renishaw | Makes tools and systems for manufacturers | 6.5 | -1.6 | 2.5% |

Click on a share's score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, and ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns 4imprint and many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine and Share Sleuth, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.