Shares for the future: a FTSE 100 firm whose qualities will prevail

This blue-chip company’s growing maturity has forced a rescore, but analyst Richard Beddard continues to believe the stock is one to own long term.

2nd April 2026 08:27

by Richard Beddard from interactive investor

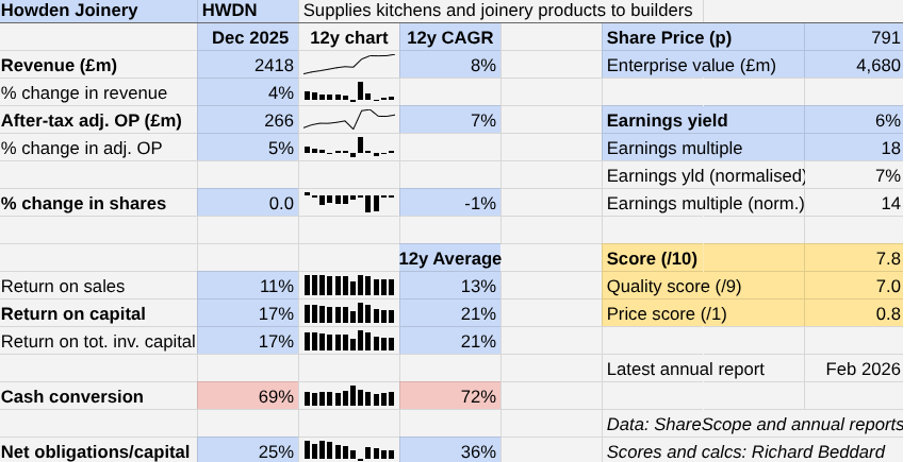

Howden Joinery Group (LSE:HWDN) grew in a contracting kitchen market in the year to December 2025. It might have grown more had it opened more depots, but at the end of the year its estate was only 2% bigger than it was at the end of 2024. It represented the slowest growth in depot numbers for at least a decade.

- Learn with ii: How many ISAs can I have? | How to become an ISA Millionaire | Pensions vs ISAs Compared

The economy is challenged on many fronts, and Howdens is experiencing teething problems in France. Nevertheless, revenue and profit grew in the mid-single digits, an improvement on the previous year but slightly below the long-term average.

The company anticipates a flat market in 2026, and modest growth as it gains more market share.

Making things easy for builders

Howdens makes things easy for builders. By selling only to the trade, it keeps prices confidential so builders can set their own margin. They get up to eight weeks credit so they can finish a job and collect payment before paying Howdens.

Howdens designs kitchens so they are easy to fit and keeps everything in stock, so builders are not delayed while they wait for parts to come in. They pick the parts up from convenient out-of-town locations.

It employs kitchen designers to help builders and their clients plan their kitchens.

This all costs money, but Howdens reaps the rewards.

- FTSE 100: big winners and losers in worst month since Covid

- Important last-minute checklist for tax year end

Trade customers are repeat purchasers. Saving them time and money keeps them coming back. Out-of-town locations are cheaper to rent than high street showrooms aimed at attracting retail customers. The builders sell the kitchens and deliver them to their customers, reducing Howdens marketing and distribution costs.

This business model was unique to the UK when Howdens introduced it over 30 years ago, and it has proved to be effective. Howdens has become the largest supplier of kitchens in the UK.

Scale confers additional advantages. For example, high volumes make it economical for Howdens to manufacture its own cabinets. A nationwide distribution network facilitates near 100% stock availability. And Howdens can buy in bulk from suppliers.

Market saturation

Almost inevitably Howdens is facing a challenge born of its own success. Sooner or later it will have saturated the UK with depots. It operated 891 at the end of the year and says it has “line of sight” to about 1,000. Even at 2025’s reduced rate, that is between four and five years of expansion.

Such targets can be lifted, but there are other reasons to believe saturation looms. Howdens reports 88% of the UK population lives within five miles of a depot. In 2019, it opened its first small footprint depots for areas with sparser, often rural populations, that could not support a full-sized depot.

Excluding fitted bedrooms, which Howdens added to the product line two years ago, Howdens estimates its share of the £11 billion UK kitchen and joinery market is roughly 20%.

- Stockwatch: is this a special situation amid the macro chaos?

- Insider: time to follow directors into these FTSE 100 stocks?

The fitted kitchen market alone is worth £6 billion, and Howdens says its share is greater than its share of joinery.

Fitted kitchens are big purchases but profitability has only been moderately sensitive to economic downturns, while Howdens has rolled out its impressive business model.

Mostly small builders repair and improve homes, so demand does not seize up when the property market does.

However, Howdens’ profit margins have fallen somewhat, from 13% to 11% during the last few inflationary years because it has absorbed losses overseas and higher costs.

Its risk report notes “geoeconomic confrontation and interstate conflict emerging as major global risks for the year ahead.

Range and territorial expansion

Beyond opening more depots, Howdens is eking more profit from existing depots through efficiencies like making better use of space and improving its digital infrastructure.

It also has a long-established brand of home appliances (Lamona) and is building own-branded ranges in flooring, bedrooms, ironmongery and other categories.

Probably the greatest growth opportunity lies overseas.

Between 2015 and 2018, Howdens operated a pilot store in the Netherlands and another in Germany. But in 2018 it chose to focus on France and Belgium, where it had been experimenting for many years. Latterly, it has targeted the Republic of Ireland too.

Howdens says France and Ireland have no big trade-only fitted kitchen suppliers, so it can establish itself there as it has here. France is much more significant, though, because of its size.

In both territories it is concentrating on particular cities such as Paris, Dublin and Cork, where there are high populations it can supply from common warehouses, and build word of mouth among tradesmen.

But France is experiencing growing pains, having added 20 stores and increased its estate by 50% in 2022. Since 2023, it has added no new depots there, focusing instead on making the ones it has opened profitable.

- Trading Strategies: a FTSE 100 to own after 23% drop

- Four tips for ISA investors to navigate stock market volatility

In 2025, Howdens closed two French depots and impaired the value of six in total, which it plans to relocate in the next two years. It is also experimenting with smaller depots in France.

It may be making headway. International sales increased 13.5% compared to 3.8% in the UK, despite the fact its international estate only grew by 1% as three new Irish depots offset the two lost French ones.

Howdens says revenue growth in France has improved markedly as it has refined the format, trained up staff, and hosted promotional activities like trade days.

In Ireland, things are going well. The company plans five new depots in 2026, two more than in 2025.

Scoring Howdens

It is hard to score companies against the backdrop of war in the Middle East and dire prognostications about the economy. To keep things in perspective, in other words. Here goes:

Howden Joinery | HWDN | Supplies kitchens and joinery products to builders | 01/04/2026 | 7.8/10 |

How capably has Howden Joinery made money? | 2.5 | |||

Under only two chief executives since it was founded in 1995, Howdens has grown at a high single-digit compound annual growth rates (CAGRs) by opening more depots and expanding its product range, mainly in the UK but also in France and latterly Ireland. Growth has been self-funded. It does not borrow from banks. | ||||

How big are the risks? | 2.0 | |||

Howdens may have saturated the UK market with depots by the early 2030s. Margins have compressed somewhat due to the rising cost of living and losses overseas, but profitability has only been moderately sensitive to economic downturns in the past. | ||||

How fair and coherent is its strategy? | 2.5 | |||

The company's founding mantra is “to be fair for all concerned”. Employees are well paid, and encouraged to be entrepreneurial. 13% of them started as apprentices. It is expanding its product range and transplanting its model to France and Ireland. In France it is experiencing growing pains. | ||||

How low (high) is the share price compared to normalised profit? | 0.8 | |||

Low. A share price of 791p values the enterprise at £4,680 million, about 14 times normalised profit. | ||||

NB: Bold text indicates factors that reduce the score. Bold and italicised text doubly so. The maximum score is 3 for each criterion except price, which has a maximum of 1 (explainedhere) | ||||

My score is lower than it was due to the growing maturity of the business and uncertainty about France and the economy. Nevertheless, I still believe Howdens’ qualities will prevail over the long term.

30 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score more than 5 out of 10 to be worthy of long-term investment in sizes determined by the ideal holding size (ihs%).

Bunzl (LSE:BNZL) has published its annual report and is due to be re-scored. I am also reconsidering the scores of Softcat (LSE:SCT) and Autotrader Group (LSE:AUTO).

company | description | score | qual | price | ih% | |

1 | FW Thorpe | Makes lighting systems for commercial, industrial and public settings | 9.0 | 1.0 | 9.9% | |

2 | Hollywood Bowl | Operates tenpin bowling centres | 8.0 | 0.7 | 7.4% | |

3 | James Latham | Distributes imported panel products, timber, and laminates | 7.5 | 1.0 | 7.0% | |

4 | Porvair | Manufactures filters and laboratory equipment | 8.0 | 0.4 | 6.7% | |

5 | Softcat | Sells software and hardware to businesses and public sector | 7.5 | 0.8 | 6.7% | |

6 | Renew | Maintains and improves road, rail, water, and energy infrastructure | 7.5 | 0.7 | 6.3% | |

7 | Goodwin | Casts and machines steel and processes minerals for niche markets | 7.5 | 0.6 | 6.1% | |

8 | Jet2 | Flies people to holiday locations, often on package tours | 7.0 | 1.0 | 6.0% | |

9 | Bunzl | Distributes essential everyday items consumed by organisations | 7.5 | 0.5 | 6.0% | |

10 | Solid State | Manufactures electronic systems and distributes components | 7.0 | 1.0 | 5.9% | |

11 | Auto Trader | Online marketplace for motor vehicles | 7.0 | 0.9 | 5.7% | |

12 | Howden Joinery | Supplies kitchens and joinery products to builders | 7.8 | 7.0 | 0.8 | 5.6% |

13 | Judges Scientific | Manufactures scientific instruments | 7.0 | 0.7 | 5.3% | |

14 | Churchill China | Manufactures tableware for restaurants etc. | 6.5 | 1.0 | 5.0% | |

15 | Oxford Instruments | Makes imaging and semiconductor manufacturing systems | 6.5 | 0.9 | 4.8% | |

16 | Volution | Manufacturer of ventilation products | 8.5 | -1.1 | 4.7% | |

17 | Advanced Medical Solutions | Manufactures surgical adhesives, sutures and dressings | 6.5 | 0.8 | 4.5% | |

18 | Anpario | Manufactures natural animal feed additives | 7.0 | 0.2 | 4.4% | |

19 | Cake Box | Cake shop franchise and sweet manufacturer | 7.0 | 0.2 | 4.4% | |

20 | Keystone Law | Operates a network of self-employed lawyers | 6.5 | 0.6 | 4.2% | |

21 | Focusrite | Designs recording equipment, synthesisers and sound systems | 6.0 | 1.0 | 4.0% | |

22 | Macfarlane | Distributes and manufactures protective packaging | 6.0 | 1.0 | 4.0% | |

23 | YouGov | Surveys public opinion and conducts market research online | 6.0 | 1.0 | 4.0% | |

24 | Games Workshop | Designs, makes and distributes Warhammer. Licenses IP | 8.5 | -1.7 | 3.6% | |

25 | Quartix | Supplies vehicle tracking systems to small fleets | 7.5 | -0.7 | 3.6% | |

26 | Bloomsbury Publishing | Publishes books and educational resources | 7.5 | -0.7 | 3.6% | |

27 | Cohort | Manufactures/supplies defence tech, training, consultancy | 8.0 | -1.4 | 3.2% | |

28 | Tristel | Manufactures hospital disinfectant | 8.0 | -1.8 | 2.5% | |

29 | Renishaw | Makes tools and systems for manufacturers | 6.5 | -0.5 | 2.5% | |

30 | 4Imprint | Customises and distributes promotional goods | 8.0 | -2.0 | 2.5% |

Click on a share's score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, and ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine and Share Sleuth, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.