Shares for the future: this AIM share breaks into my top 10

Claiming to be one of the happiest firms of its kind in the country, analyst Richard Beddard has upgraded its shares, which he believes are now better value and a little less risky.

12th June 2026 15:19

by Richard Beddard from interactive investor

In a presentation of Keystone Law Group Ordinary Shares (LSE:KEYS)’s full-year results earlier this year, founder and chief executive James Knight said the year to January 2026 had been a good one, perhaps Keystone’s best all round.

- Learn with ii: How to become an ISA millionaire | ISA Investment Ideas | Top ISA Funds

A good year for recruitment

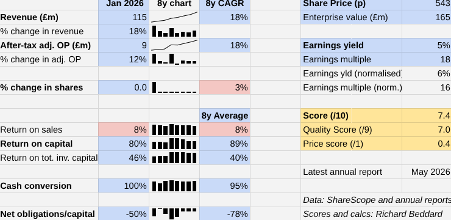

It was a good year. Revenue increased 18% and after-tax adjusted operating profit increased 12%. Keystone was highly profitable as usual because it has relatively low costs and only pays its lawyers once it receives fees for the work they do.

Founded in 2002, Keystone was the first UK platform law firm and, although others have followed it, none have listed.

Unlike traditional law firms, which are generally owned and managed by senior lawyers, equity partners, Keystone is a community of nearly 500 self-employed principals (partner-level lawyers). Shareholders own it. Typically, the lawyers operate as Personal Service Companies (PSCs). Keystone calls them Pods.

In many ways, Keystone passes as a traditional law firm. It provides the brand and administrative services. It contracts with clients and bills them. It does compliance. It runs training and networking events. Principals operate under its professional indemnity insurance cover. It provides the IT infrastructure required to practice and share work with other Keystone lawyers.

If principals need legal support a small team of 17 junior in-house lawyers can help, and Keystone provides office space in London.

- Analyst predicts FTSE 100 break above 12,000

- The Income Investor: a FTSE 100 stock with dividend potential

But the set-up is different. Keystone pays 75% of the fee income it collects as revenue to the principals, keeping 25% for itself. Typically, Keystone says, this model pays lawyers more than they would earn in a conventional firm, but the main attraction is a better work-life balance. Keystone lawyers manage their own workloads, and can work when and where they want.

Principals work from home or their own offices. Barring its central-office support staff, Keystone doesn’t pay sick pay or holiday pay and the tax regime is generally more efficient for the self-employed. Lower costs mean there is more money for the lawyers and shareholders. Lower fixed costs mean the money flows more consistently.

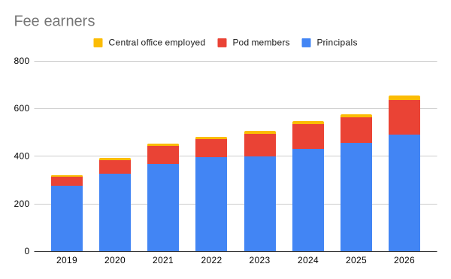

Keystone has grown by recruiting principals from conventional law firms, and as they grow their practices.

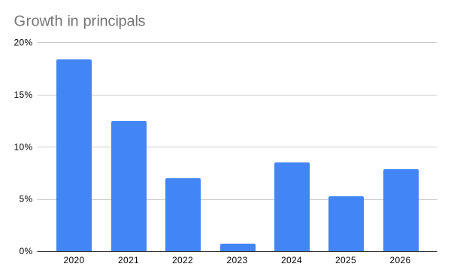

One way they can grow is by employing junior lawyers in their Pods. Fees from other fee earners was a significant contributor to growth in 2026. The number of principals grew 8%, above average for the post-Covid period, but the smaller number of other fee earners grew 35%, the best year since 2020.

Source: Keystone Law annual reports.

There is a counter-cyclical element to this growth. When lawyers are in high demand as they have been since the pandemic, law firms compete to recruit and retain them by offering high pay predicated on aggressive targets. When demand for legal services softens, lawyers must work impossibly hard to meet these targets and Keystone finds it easier to recruit them.

Perhaps we can infer that the market has softened. Keystone is finding it easier to recruit now than it was in 2023, when it achieved 1% growth in principal numbers.

More than the sum of its principals

Source: Keystone Law annual reports

A report by Codex Edge, the Platform Firms Report 2026, put Keystone in second place among platforms by lawyer headcount in 2025. Top of the list was faster-growing Setfords.

Despite many newer entrants, Keystone says it is the “premier” platform law firm, distinguished by the quality of its lawyers and the full range of legal services it can provide. This claim is borne out by the same report’s data on revenue per lawyer and profitability, which puts Keystone well ahead of Setfords.

Keystone is selective. In 2026, it received 294 qualified applicants and made offers to 96 (68 were accepted, 61 joined). 221 of its 491 principals are recognised in the leading guide to law firms and solicitors rankings (the Legal 500 UK Solicitors 2025).

- Have stock markets kept pace with World Cup final ticket boom?

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

The report’s data also shows Keystone is recruiting relatively high-quality lawyers. Only about a quarter of its recruits were not among the top 500 law firms in 2025, compared to about a half of Setfords’ recruits.

This emphasis on quality, Keystone says, reinforces its reputation, which makes it easier to recruit more high-quality lawyers.

Keystone is also more than the sum of its principals because Keystone encourages them to refer work to each other. The originator keeps 15% of the 75% lawyer cut, leaving 60% for the lawyer who does the work. More than 30% of work is referred, a ratio, James Knight says, that compares favourably with conventional firms.

Although Keystone has a minority interest in an Australian firm, it has no plans to expand abroad. The UK upper-mid market where it positions itself employs 42,000 lawyers and is worth about £14 billion. With 654 lawyers and revenue of £115 million, it may well be much closer to the beginning than the end of its UK expansion.

Platform killers

Beyond competitors, to my mind there are two significant risks. One could undermine Keystone’s platform business model. The other could undermine the fees all law firms earn.

The self-employed status of Keystone Law’s principals is justified by their autonomy, but Keystone’s annual report routinely warns that the authorities could deem them employees, substantially increasing costs.

I take this risk seriously because it is routinely disclosed in Keystone’s annual report, but I don’t have an opinion on how likely it is that its lawyers could be deemed employees.

The second risk is, of course, AI. Earlier this year Keystone adopted CoCounsel, a legal AI. This allows Keystone’s lawyers to interrogate Westlaw, one of the main case law databases, and libraries of document templates. The promise is faster research and drafting of legal documents.

It sounds like an unalloyed benefit, but AI may impact fees since lawyers are often paid by the hour and AI is quick. Keystone Law says its work is too complex to outsource entirely to AI, and it is too early to detect the impact on efficiency and pricing.

More efficiency will enable lawyers to do more work, which lawyers have been adept at generating when technology has been introduced in the past.

For now, legal services is a people business. Keystone thinks it is one of the happiest law firms in the country. Its Trustpilot score of 4.7 suggests that its clients are happy too.

Scoring Keystone Law

I like Keystone. I have penalised the unknowns quite heavily because I don’t know the sector very well. Few law firms are listed in London, and the first was Gately (not a platform firm) in 2015.

We do know that Keystone has generated steady and profitable growth since it floated three years later and outperformed more conventional peers.

The company holds its AGM on 18 June but did not provide an update last year.

| Keystone Law | KEYS | Operates a network of self-employed lawyers | 10/06/2026 | 7.4/10 |

| How capably has Keystone Law made money? | 3.0 | |||

| Under its founder and chief executive, Keystone has grown profit and revenue at double-digit CAGRs since it floated in FY 2018. It pioneered the platform model by giving senior lawyers more control of where, when and what they work on. This has given it know-how, scale, and a growing reputation. | ||||

| How big are the risks? | 1.0 | |||

| As the platform model has gained credibility, Keystone has attracted competitors. It trades on the quality of its lawyers. The self-employed status of Keystone's lawyers could change, increasing costs. AI may commodify legal work, although it may also allow Keystone’s lawyers to work more efficiently. | ||||

| How fair and coherent is its strategy? | 3.0 | |||

| Keystone pays principals once it is paid, deducting a transparent fee that fosters collaboration. It provides services allowing layers to focus on their clients. By recruiting high-profile senior lawyers Keystone’s reputation grows, in turn attracting high-quality applicants. They’re happy and so are clients! | ||||

| How low (high) is the share price compared to normalised profit? | 0.4 | |||

| Low. A share price of 543p values the enterprise at £165 million, about 16 times normalised profit. | ||||

| NB: Bold text indicates factors that reduce the score. Bold and italicised text doubly so. The maximum score is 3 for each criterion except price, which has a maximum of 1 (explained here) | ||||

Previously, the shares ranked 26th in the Decision Engine at 6.3, but the scores for both price and big risks have now doubled from 0.2 and 0.5 respectively.

30 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score more than 5 out of 10 to be worthy of long-term investment in sizes determined by the ideal holding size (ihs%).

Judges Scientific (LSE:JDG), Anpario (LSE:ANP), and Autotrader Group (LSE:AUTO) have published annual reports and are due to be re-scored.

| company | description | score | qual | price | ih% |

| FW Thorpe | Makes lighting systems for commercial, industrial and public settings | 9.9 | 9.0 | 0.9 | 9.8% |

| James Latham | Distributes imported panel products, timber, and laminates | 8.5 | 7.5 | 1.0 | 7.0% |

| Hollywood Bowl | Operates tenpin bowling centres | 8.3 | 8.0 | 0.3 | 6.6% |

| Renew | Maintains and improves road, rail, water, and energy infrastructure | 8.2 | 7.5 | 0.7 | 6.3% |

| Jet2 | Flies people to holiday locations, often on package tours | 8.0 | 7.0 | 1.0 | 6.0% |

| Solid State | Manufactures electronic systems and distributes components | 7.9 | 7.0 | 0.9 | 5.8% |

| Porvair | Manufactures filters and laboratory equipment | 7.9 | 8.0 | -0.1 | 5.7% |

| Howden Joinery | Supplies kitchens and joinery to builders and online to DIYers | 7.8 | 7.0 | 0.8 | 5.6% |

| Judges Scientific | Manufactures scientific instruments | 7.5 | 7.0 | 0.5 | 5.1% |

| Keystone Law | Operates a network of self-employed lawyers | 7.4 | 7.0 | 0.4 | 4.9% |

| Auto Trader | Online marketplace for motor vehicles | 7.4 | 6.5 | 0.9 | 4.8% |

| Bunzl | Distributes essential everyday items consumed by businesses | 7.4 | 7.0 | 0.4 | 4.8% |

| Oxford Instruments | Makes imaging and semiconductor manufacturing systems | 7.2 | 6.5 | 0.7 | 4.4% |

| Volution | Manufacturer of ventilation products | 7.2 | 8.5 | -1.3 | 4.4% |

| Cake Box | Cake shop franchise and sweet manufacturer | 7.2 | 7.0 | 0.2 | 4.3% |

| Goodwin | Casts and machines steel and processes minerals for niche markets | 7.1 | 7.5 | -0.4 | 4.3% |

| Churchill China | Manufactures tableware for restaurants etc. | 7.0 | 6.0 | 1.0 | 4.0% |

| Focusrite | Designs recording equipment, synthesisers and sound systems | 7.0 | 6.0 | 1.0 | 4.0% |

| Advanced Medical Solutions | Manufactures surgical adhesives, sutures and dressings | 7.0 | 6.5 | 0.5 | 4.0% |

| YouGov | Surveys public opinion and conducts market research online | 6.9 | 6.0 | 0.9 | 3.9% |

| Games Workshop | Designs, makes and distributes Warhammer. Licenses IP | 6.8 | 8.5 | -1.7 | 3.6% |

| Anpario | Manufactures natural animal feed additives | 6.7 | 7.0 | -0.3 | 3.5% |

| Quartix | Supplies vehicle tracking systems to small fleets | 6.5 | 7.0 | -0.5 | 3.1% |

| Macfarlane | Distributes and manufactures protective packaging | 6.5 | 5.5 | 1.0 | 3.0% |

| Softcat | Sells software and hardware to businesses and public sector | 6.4 | 7.0 | -0.6 | 2.9% |

| Cohort | Manufactures/supplies defence tech, training, consultancy | 6.4 | 8.0 | -1.6 | 2.8% |

| Bloomsbury Publishing | Publishes books and educational resources | 6.1 | 7.5 | -1.4 | 2.5% |

| Tristel | Manufactures hospital disinfectant | 6.0 | 8.0 | -2.0 | 2.5% |

| 4Imprint | Customises and distributes promotional goods | 5.9 | 8.0 | -2.1 | 2.5% |

| Renishaw | Makes tools and systems for manufacturers | 4.6 | 6.5 | -1.9 | 2.5% |

Click on a share's score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, and ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine and Share Sleuth, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.