Shares for the future: no longer terrified by star stock’s share price

Clouds are gathering at one of last year’s big risers, but a share price slump does mean they’re better value. Analyst Richard Beddard explains why he thinks they’re still a good long-term investment.

27th March 2026 15:29

by Richard Beddard from interactive investor

When I re-scored Goodwin (LSE:GDWN) last November, I was impressed by the business and terrified by the share price after the company published a trading update that revealed profit for the year to April 2026 would double.

To my mind, Goodwin had delivered the promise made a decade or so ago to restore the two most important companies in its Mechanical Engineering division, Goodwin Steel Castings and Goodwin International, after a crash in the oil price stymied demand for valves used in oil pipelines.

- Invest with ii: Open an ISA | ISA Investment Ideas | ISA Offers & Cashback

Goodwin enlarged its foundry and diversified to manufacture components for nuclear submarines and naval frigates, and self-shielded boxes and racks for storing radioactive zeolite at Sellafield prior to disposal.

Sales to the defence and nuclear industries are lumpy, but Goodwin has frequently referred to “multi-decade” programmes, for which it is the incumbent or, in the case of self-shielded boxes, the only company in the UK capable of supplying. The company has told me it can cast super alloys at sizes few in the world can.

On that basis, I felt the huge uplift in profit expected this year was a new base from which Goodwin would grow. It was not a blip. For what it is worth, I still think that. But Goodwin’s update has given us many reasons to be less confident in that judgement, at least in the short term.

Goodwin: clouds gathering

This week I’m re-scoring Goodwin after another trading update. Maybe I was too accommodating in November.

On Monday, Goodwin reiterated that profit should double in the year to April 2026, a prediction that is closer and consequently more reliable now.

Clouds are gathering thereafter, though. I cannot say how ominous they are because Goodwin doesn’t tell us. For some clouds, Goodwin will not know.

The first clouds are two lost tenders, one for, the company tells me, the supply of 100-year cans to Sellafield. The other was to supply Estonia with coastal radar and antennae systems from Goodwin’s Easat subsidiary.

Goodwin had been working on the tender for two years and was surprised it didn’t come its way given its position as a key supplier of another kind of nuclear waste container. In February, Sellafield awarded a 100-year can contract to LTi Metaltech. The cans store plutonium.

The loss of the Easat tender is, perhaps, less surprising, since the company is just establishing itself as a radar systems supplier. It is disappointing though, because Goodwin had been anticipating a surge in orders and “multiple simultaneous opportunities...”.

In the year to April 2025, Easat made a small profit. While the business was not as busy as it had expected, it was building systems for the Royal Thai Air Force, a civil airport in Vietnam, and Cranfield airport in the UK. Since Estonia has not joined these projects, maybe the conclusion we should draw is that Easat is still less busy than anticipated.

- Biggest FTSE 100 dividend stock leads April windfall

- Sector Screener: two FTSE 100 stocks with long-term appeal

- Four tips for ISA investors to navigate stock market volatility

In the update, Goodwin also tempered expectations about brand new business, Duvelco. Duvelco manufactures a novel high-performance plastic called Ducoya. Having built the factory, it’s now marketing the product.

We already knew that first revenues are expected in the year to April 2027, later than the company originally anticipated, but Monday’s update added that Goodwin doesn’t expect “substantial” revenue “in the early years”.

This does not directly contradict Goodwin’s belief expressed in its most recent annual report that Duvelco “will be the largest and most profitable division in years to come”, but maybe it should have inserted the word “many” into that phrase.

Delays introducing new products are not shocking. Any long-term follower of Victrex (LSE:VCT), another high-performance polymer manufacturer, knows how hard it has been for that company to establish its very well-established product in new markets.

If one of Goodwin’s sins is overconfidence, one of its virtues has been patience. It took longer than Goodwin expected to ramp up production for nuclear and defence contracts, and it is taking longer than expected for Easat to establish its radar systems.

At times, Goodwin has invested heavily in these businesses while they were losing money. Goodwin International and Goodwin Steel Castings have roared back to life and Easat was at least profitable in 2025.

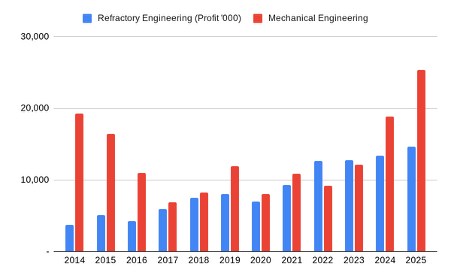

Goodwin has been able to carry these businesses at times because other aspects of the conglomerate have been making good money, most notably a second division, Refractory Engineering. Goodwin makes powders used in the casting of jewellery and tyres, for example. It also processes a wide range of minerals.

As global market leader in the supply of investment casting powder for jewellery, Refractory Engineering grew more reliably than Mechanical Engineering over the last decade, and earned higher profit margins for much of it.

However, Goodwin’s update casts an unknowable amount of shade on the Refractory Engineering division’s prospects.

The outlook for the jewellery market, Goodwin says, is tempered by the high price of gold and silver, which makes jewellery less affordable, particularly as jewellery buyers are counting their pennies more carefully due to the rising cost of living.

Here are two more clouds.

Oil, gas and petrochemicals are still significant markets for Goodwin. They brought in a combined total of 23% of revenue in 2025. Goodwin still makes valves for pipelines, although these days they are often for Liquefied Natural Gas (LNG) projects. These valves are cast by Goodwin Steel castings and machined by Goodwin International and another subsidiary, Noreva.

The company’s biggest LNG customers are in the US and the Persian Gulf states. Infrastructure in the Gulf is under attack from Iran, as it seeks to disrupt the global economy and pressure the US and Israel to end the war.

- How to trade the greatest late-cycle bull market in history

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

- Chart Insights: gold, inflation and interest rate outlook

Goodwin says that customers in the Gulf are delaying orders, although none have cancelled yet. How the Iran war will progress is, of course, another uncertainty.

The final cloud is a corollary of all the previous ones.

Goodwin is considering reducing the percentage of earnings it will pay out as a dividend. This will save resources that may be needed in more uncertain times.

Profit this year should double, so a cut in the proportion paid as a dividend need not lead to a dividend cut. It surely indicates Goodwin is concerned about the outlook for its many businesses in aggregate, though.

Re-scoring Goodwin

Re-scoring Goodwin is difficult because the trading update contains so much to worry about and no estimation of its impact. The only business segments not clouded by Goodwin’s most recent update are Defence (21% of revenue in 2025) and Mining (8% of revenue).

I’m looking past the likely short-term impacts of war, recession and lost opportunities to score the company’s long-term prospects.

Goodwin develops niche businesses too small to interest global multinationals. Their size though is a limitation, and to grow faster than its niches it must expand them by developing new products, or entering new niches by developing new businesses. We are seeing this at Easat and Duvelco.

I had already recognised the risk that new niches often take longer to establish than the company anticipates, but there is also a risk they may never flourish.

Also, I’m reintroducing a kludge. Goodwin is so complex and diverse that I don’t feel as confident as I should in my assessment of the risks.

The company is capital intensive, defence and nuclear contracts are lumpy, some markets like oil and gas are volatile, even the stalwart Refractory Engineering division is susceptible to changes in the gold price and consumer sentiment.

I have reintroduced complexity risk to Goodwin’s score, which I hated when I did it before because it was not specific. Right now, I don’t have a better way to accommodate the uncertainty.

Goodwin | GDWN | Casts and machines steel and processes minerals for niche markets | 26/03/2026 | 7.4/10 |

How capably has Goodwin made money? | 3.0 | |||

Over the last six years, family run Goodwin has grown revenue modestly and profit in the low double digits while building capacity and capabilities in niche markets new and old. In the year to April 2026, profit is expected to double. Heavy capital expenditure has reduced cash conversion, but Goodwin is seeing the benefit now. | ||||

How big are the risks? | 1.5 | |||

To grow Goodwin beyond its niches Goodwin must establish new products and businesses, which often takes longer than it expects and could result in failure.Although Goodwin’s diversity shields it from the sometimes volatile performance of individual businesses, its complexity may hide risk. | ||||

How fair and coherent is its strategy? | 3.0 | |||

Goodwin invests for the long term in global businesses too small to attract competition from large multinationals. It has a skilled workforce, high employee retention, and the directors earn a modest 10x median income (£46,000). The Goodwin family have a controlling stake. On balance, they have been good stewards. | ||||

How low (high) is the share price compared to profit? | -0.1 | |||

High. A share price of 13,700p values the enterprise at £1,070 million, about 19 times forecast profit. | ||||

NB: Bold text indicates factors that reduce the score. Bold and italicised text doubly so. The maximum score is 3 for each criterion except price, which has a maximum of 1 (explainedhere) | ||||

I still think Goodwin is a good long-term investment even though I’m not as confident as I was. Because of the dramatic decline in the share price, its score has risen despite my intervention. A score of 7.4 equates to an ideal holding size of 4.7%.

I’m no longer terrified by the price, but I am a little more circumspect about the business.

31 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score more than 5 out of 10 to be worthy of long-term investment in sizes determined by the ideal holding size (ihs%).

Howden Joinery Group (LSE:HWDN) and Bunzl (LSE:BNZL) have published annual reports. I’ve re-scored Howdens (the score is in the table below), and we will publish the breakdown next week. Bunzl will follow.

company | description | score | qual | price | ih% | |

1 | FW Thorpe | Makes lighting systems for commercial, industrial and public settings | 9.0 | 1.0 | 9.9% | |

2 | Hollywood Bowl | Operates tenpin bowling centres | 8.0 | 0.7 | 7.3% | |

3 | James Latham | Distributes imported panel products, timber, and laminates | 7.5 | 1.0 | 7.0% | |

4 | Softcat | Sells software and hardware to businesses and public sector | 7.5 | 0.8 | 6.7% | |

5 | Porvair | Manufactures filters and laboratory equipment | 8.0 | 0.3 | 6.7% | |

6 | Renew | Maintains and improves road, rail, water, and energy infrastructure | 7.5 | 0.6 | 6.3% | |

7 | Bunzl | Distributes essential everyday items consumed by organisations | 7.5 | 0.6 | 6.1% | |

8 | Jet2 | Flies people to holiday locations, often on package tours | 7.0 | 1.0 | 6.0% | |

9 | Solid State | Manufactures electronic systems and distributes components | 7.0 | 1.0 | 5.9% | |

10 | Auto Trader | Online marketplace for motor vehicles | 7.0 | 0.9 | 5.7% | |

11 | Howden Joinery | Supplies kitchens and joinery products to builders | 7.8 | 7.0 | 0.8 | 5.5% |

12 | Judges Scientific | Manufactures scientific instruments | 7.0 | 0.7 | 5.3% | |

13 | Churchill China | Manufactures tableware for restaurants etc. | 6.5 | 1.0 | 5.0% | |

14 | Anpario | Manufactures natural animal feed additives | 7.0 | 0.4 | 4.9% | |

15 | Oxford Instruments | Makes imaging and semiconductor manufacturing systems | 6.5 | 0.9 | 4.8% | |

16 | Goodwin | Casts and machines steel and processes minerals for niche markets | 7.4 | 7.5 | -0.1 | 4.7% |

17 | Volution | Manufacturer of ventilation products | 8.5 | -1.2 | 4.5% | |

18 | Advanced Medical Solutions | Manufactures surgical adhesives, sutures and dressings | 6.5 | 0.8 | 4.5% | |

19 | Cake Box | Cake shop franchise and sweet manufacturer | 7.0 | 0.2 | 4.4% | |

20 | Focusrite | Designs recording equipment, synthesisers and sound systems | 6.0 | 1.0 | 4.0% | |

21 | Macfarlane | Distributes and manufactures protective packaging | 6.0 | 1.0 | 4.0% | |

22 | YouGov | Surveys public opinion and conducts market research online | 6.0 | 1.0 | 4.0% | |

23 | Keystone Law | Operates a network of self-employed lawyers | 6.5 | 0.5 | 3.9% | |

24 | Games Workshop | Designs, makes and distributes Warhammer. Licenses IP | 8.5 | -1.7 | 3.6% | |

25 | Bloomsbury Publishing | Publishes books and educational resources | 7.5 | -0.7 | 3.5% | |

26 | Cohort | Manufactures/supplies defence tech, training, consultancy | 8.0 | -1.5 | 3.1% | |

27 | Quartix | Supplies vehicle tracking systems to small fleets | 7.5 | -1.3 | 2.5% | |

28 | Tristel | Manufactures hospital disinfectant | 8.0 | -1.9 | 2.5% | |

29 | 4Imprint | Customises and distributes promotional goods | 8.0 | -2.1 | 2.5% | |

30 | Renishaw | Makes tools and systems for manufacturers | 6.5 | -0.9 | 2.5% |

Click on a share's score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, and ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine and Share Sleuth, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.