Shares for the future: nothing dull about this FTSE 100 stock

A terrible 2025 for this blue-chip’s share price has been followed by a much better 2026, but what does analyst Richard Beddard think about prospects?

17th April 2026 15:00

by Richard Beddard from interactive investor

I am starting this year’s reappraisal of Bunzl (LSE:BNZL) with North America. The continent is where Bunzl earns 53% of revenue, and developments there shine a light on its strategy.

- Invest with ii: Top UK Shares | Share Tips & Ideas | Open a Trading Account

Roll back

North America is home to Bunzl’s biggest business, North America Distribution (aka Distribution), which contributed about 30% of total revenue in the year to December 2025. Distribution supplies packaging and other products to caterers and grocers. These are Bunzl’s two biggest sectors. Food service contributes 31% of revenue and grocery 28%.

Although the US economy was stymied by economic uncertainty, Bunzl says this served to amplify “execution issues” at Distribution, which “strongly impacted” Bunzl’s overall performance. Distribution has been misfiring for a couple of years, and to its credit, Bunzl gives over a few pages of its annual report to it.

In 2023, Bunzl restructured Distribution, dispensing with the branch model under which more than 40 general managers took responsibility for pricing and stock. It introduced a more centralised operation that separated the sales function from the supply chain.

The intention was to focus the local teams on sales and encourage the adoption of own-brand products. The outcome was reduced sales to caterers and redistributors and higher costs, which combined with price deflation also reduced profit margins.

Bunzl has responded in a number of ways, launching more own-brand products, and cutting costs. Most significantly perhaps, it has tried to “re-energise” local teams by returning more control to them.

- Stockwatch: a rare but risky example of rapid growth

- ISA investing: nine ii experts reveal their ISA tips for 2026-27

Despite only achieving a moderation in Distribution’s decline in profit margins during the second half of the financial year, Bunzl is confident in the freshly tweaked new operating model.

I believe this partial row-back exposes a tension in Bunzl’s business model. To see why, we need to take a closer look at the company’s capabilities and strategy.

Roll up

City writers often refer to Bunzl as boring. It distributes essential products that businesses and organisations like hospitals use every day. They include packaging, store supplies, cleaning equipment, hygiene products, medical consumables and safety gear.

The company claims to be the largest value-added distributor of many of these products in the world, employing over 26,000 people in more than 33 countries.

Scale gives it advantages. Being a “one-stop shop”, for example, it can reduce costs for customers by consolidating all manner of products into a single delivery.

Bunzl adds value through efficient supply and by developing sustainable own-brands, but volumes are critical to profitability. It earns modest profit margins on large volumes resulting in 2025 in an impressive 27% return on capital.

It has grown by acquiring rivals it knows well. Since 2004, it has acquired more than 230 regional distributors, and it is targeting 1,300 more. Each new acquisition grows Bunzl by a small increment, extending its territorial footprint, its product range, and its capabilities.

- Nvidia breaks records as Wall Street makes ‘astonishing’ recovery

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

Bunzl encourages the owners of acquired businesses to stay on, which is both an inducement for them to sell, and retains local supplier and customer relationships in the business.

The company improves the efficiency of new branches by consolidating warehouses, sharing IT systems, and purchasing in bulk. For example, it is in the process of reducing the number of warehouses in France from 15 to six.

In theory, the bigger Bunzl gets, the better it gets, but the centralisation of Distribution is contrary to Bunzl’s decentralised roll up strategy.

Distribution is predominantly a US business. It already has a national footprint, so acquisitions make less sense. As the business matures, it must rely more heavily on organic growth through efficiencies, extending the product range and competing for greater market share.

If Distribution has found the right balance between autonomy and efficiency, revenue and profitability should improve. But relying on organic growth in its biggest business may mean it grows less rapidly in future.

In fact, Bunzl has not acquired a food service or grocery distributor in North America since PackPro (Canada) in 2023, and generally throughout the last decade it has sought to diversify. In 2024, Bunzl reported that 70% of total announced acquisition spend over the previous five years went on acquisitions in Healthcare, Cleaning & Hygiene, and Safety.

Scoring Bunzl

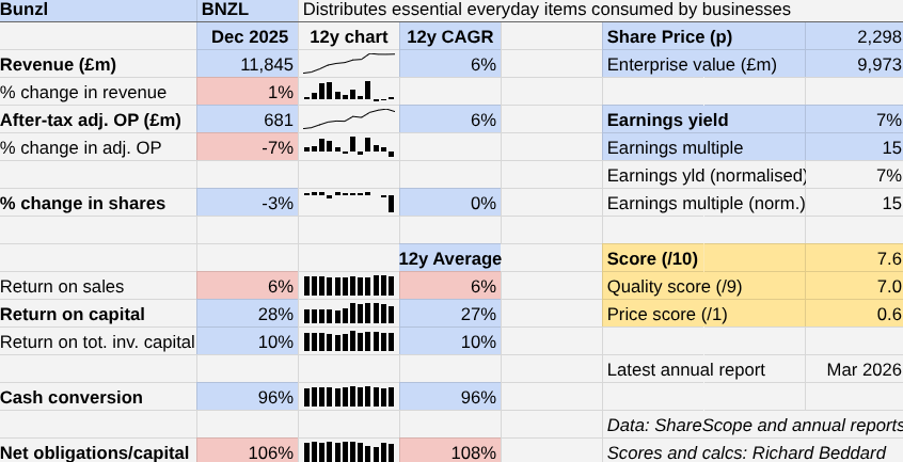

Bunzl | BNZL | Distributes essential everyday items consumed by businesses | 16/04/2026 | 7.6/10 |

How capably has Bunzl made money? | 2.0 | |||

Bunzl has achieved mid-single digit compound annual growth rates (CAGRs) by acquiring regional distributors and generating economies of scale. Except for North America Distribution, its biggest and most centralised business, it operates as a network of autonomous branches. | ||||

How big are the risks? | 2.0 | |||

The company's high debt to capital ratio can only be sustained if its long history of stable and growing cash flow and high returns on capital continue. Acquisitions have generated good returns. North America Distribution is maturing and will likely not grow as quickly. | ||||

How fair and coherent is its strategy? | 3.0 | |||

Bunzl has grown consistently through cost-effective acquisitions. To squeeze more from North America Distribution, Bunzl has centralised it contrary to its decentralised business model. Initially, this has resulted in higher costs and lower sales. It is mostly a great place to work. | ||||

How low (high) is the share price compared to normalised profit? | 0.6 | |||

Low. A share price of 2,298p values the enterprise at £9,973 million, about 15 times normalised profit. | ||||

NB: Bold text indicates factors that reduce the score. Bold and italicised text doubly so. The maximum score is 3 for each criterion except price, which has a maximum of 1 (explainedhere) | ||||

2025

There is less to say about acquisitions than usual this year, because Bunzl spent less than a third of its average spend over the last five years, albeit on eight businesses. This, it explains, was due to the prevailing uncertainty.

Inflation and tariffs can be good for Bunzl because it operates on a cost-plus basis that passes price rises on to customers. Higher prices mean higher revenue, which leads to a higher profit margin when Bunzl can keep its own cost base from rising as much.

After a year of reduced acquisition activity, organisational troubles in North America, and weak customer sentiment, though, the results were poor by Bunzl’s standards. Turnover grew 1% and adjusted after-tax operating profit fell 7%.

In every other respect Bunzl’s performance was typical. The only red flags are the ones I have learned to live with: a business with modest 6% profit margins and operating capital entirely funded by debt.

Low profit margins are compensated by high volumes, and debt is conscionable while Bunzl’s profitability is high and cash conversion is stable.

Bunzl anticipates flat profit in 2026, followed by profit growth. More may be revealed in a first-quarter trading update that should be released on 22 April.

30 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score more than 5 out of 10 to be worthy of long-term investment in sizes determined by the ideal holding size (ihs%).

4imprint Group (LSE:FOUR) and Macfarlane Group (LSE:MACF) have published annual reports and are due to be re-scored.

company | description | score | qual | price | ih% | |

1 | FW Thorpe | Makes lighting systems for commercial, industrial and public settings | 9.0 | 0.9 | 9.8% | |

2 | James Latham | Distributes imported panel products, timber, and laminates | 7.5 | 1.0 | 7.0% | |

3 | Hollywood Bowl | Operates tenpin bowling centres | 8.0 | 0.5 | 7.0% | |

4 | Porvair | Manufactures filters and laboratory equipment | 8.0 | 0.2 | 6.4% | |

5 | Jet2 | Flies people to holiday locations, often on package tours | 7.0 | 1.0 | 6.0% | |

6 | Solid State | Manufactures electronic systems and distributes components | 7.0 | 0.9 | 5.9% | |

7 | Renew | Maintains and improves road, rail, water, and energy infrastructure | 7.5 | 0.4 | 5.9% | |

8 | Auto Trader | Online marketplace for motor vehicles | 7.0 | 0.8 | 5.6% | |

9 | Softcat | Sells software and hardware to businesses and public sector | 7.0 | 0.8 | 5.5% | |

10 | Howden Joinery | Supplies kitchens and joinery products to builders | 7.0 | 0.7 | 5.4% | |

11 | Goodwin | Casts and machines steel and processes minerals for niche markets | 7.5 | 0.1 | 5.3% | |

12 | Judges Scientific | Manufactures scientific instruments | 7.0 | 0.6 | 5.3% | |

13 | Bunzl | Distributes essential everyday items consumed by businesses | 7.6 | 7.0 | 0.6 | 5.2% |

14 | Churchill China | Manufactures tableware for restaurants etc. | 6.5 | 1.0 | 5.0% | |

15 | Oxford Instruments | Makes imaging and semiconductor manufacturing systems | 6.5 | 0.8 | 4.6% | |

16 | Cake Box | Cake shop franchise and sweet manufacturer | 7.0 | 0.2 | 4.4% | |

17 | Advanced Medical Solutions | Manufactures surgical adhesives, sutures and dressings | 6.5 | 0.6 | 4.1% | |

18 | Volution | Manufacturer of ventilation products | 8.5 | -1.5 | 4.1% | |

19 | Focusrite | Designs recording equipment, synthesisers and sound systems | 6.0 | 1.0 | 4.0% | |

20 | Macfarlane | Distributes and manufactures protective packaging | 6.0 | 1.0 | 4.0% | |

21 | YouGov | Surveys public opinion and conducts market research online | 6.0 | 1.0 | 3.9% | |

22 | Keystone Law | Operates a network of self-employed lawyers | 6.5 | 0.4 | 3.8% | |

23 | Anpario | Manufactures natural animal feed additives | 7.0 | -0.2 | 3.6% | |

24 | Games Workshop | Designs, makes and distributes Warhammer. Licenses IP | 8.5 | -1.7 | 3.5% | |

25 | Bloomsbury Publishing | Publishes books and educational resources | 7.5 | -1.0 | 3.0% | |

26 | Cohort | Manufactures/supplies defence tech, training, consultancy | 8.0 | -1.7 | 2.6% | |

27 | Tristel | Manufactures hospital disinfectant | 8.0 | -1.9 | 2.5% | |

28 | Quartix | Supplies vehicle tracking systems to small fleets | 7.5 | -1.8 | 2.5% | |

29 | 4Imprint | Customises and distributes promotional goods | 8.0 | -2.3 | 2.5% | |

30 | Renishaw | Makes tools and systems for manufacturers | 6.5 | -1.0 | 2.5% |

Click on a share's score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, and ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns Bunzl and many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine and Share Sleuth, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.