Shares for the future: a business transformed and positioned for growth?

Its shares are not cheap anymore, but the company is managing the things it can control well, which keeps this stock in analyst Richard Beddard’s top 20.

3rd July 2026 15:02

by Richard Beddard from interactive investor

The first hurdle in understanding Oxford Instruments (LSE:OXIG) is the science. The second is the geopolitics.

Big profits from tiny atoms

Primarily, the company makes sophisticated scientific instruments used by researchers at academic institutions and in commercial teams. They are active in research and development, quality assurance, and increasingly in production environments.

- Invest with ii: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

About three-quarters of total revenue and 96% of adjusted operating profit in the year to March 2026 was earned in Oxford Instruments’ Imaging & Analysis division.

These companies make microscopes, detectors, and cameras. They are used by materials scientists, semiconductor designers, and life scientists to measure the properties of materials, drugs, and semiconductors, for example, at the tiniest scales.

Oxford Instruments’ second division, Advanced Technologies, earns more than 90% of revenue from compound semiconductor manufacturing systems.

Compound semiconductors are made from more than one element. They are more powerful and flexible than traditional silicon and account for about 8% of the rapidly growing $130 billion (£97.2 billion) semiconductor manufacturing equipment market.

Oxford Instruments’ etch and deposition technology adds a layer only a few atoms thick to semiconductor wafers and selectively removes it to create circuits, also with atomic accuracy.

The thinness of these layers is a major determinant of how powerful and efficient the semiconductors are. Thin layers also require less material to produce, which reduces semiconductor fabricators’ manufacturing costs.

Oxford Instruments says demanding applications like artificial intelligence (AI) are driving a shift from silicon to compound semiconductors. It has developed volume manufacturing systems so it can grow out of its research and development niche.

To make the most of the opportunity, it opened a new manufacturing facility near Bristol in 2025, tripling its pre-existing capacity.

Imaging & Analysis remains highly profitable, but it has contracted somewhat in recent years due to post-Covid destocking, trade restrictions, and low productivity at Belfast subsidiary, Andor, which was restructured in the year to March 2026.

Despite promising signs of turnaround and growth, neither division grew in 2026, though.

2026: a game of two halves

There were more headwinds: tariff increases, the erection of other trade barriers, and cuts in academic funding in the first quarter of the financial year, April to June 2025. These triggered an 11% decline in Imaging and Analysis orders.

A recovery in the second half of the year, helped by the restructuring, resulted in a small increase in the value of orders at the end of the year, compared to the previous year at constant currency rates.

The Advanced Technologies division experienced strong demand all year and the order book was 28% higher than it was in March 2025.

The orders did not translate into revenue growth at either division. At Imaging & Analysis, revenue declined, and at Advanced Technologies it was flat.

In both divisions, revenue lagged orders because growth was strongest in the final quarter. Many of the orders are being delivered in the current financial year.

This situation was compounded at Advanced Technologies by longer lead times.

The new volume manufacturing systems take longer to make and Oxford Instruments is inexperienced in building them. Manufacturing challenges at its new facility in Bristol delayed some deliveries and some customers delayed receipt of equipment because their new semiconductor fabrication plants (fabs) were not ready for them.

Exacerbated by currency headwinds, Oxford Instruments’ revenue fell 5%. Adjusted after-tax operating profit fell 9%. Return on capital was a sub-par but still very healthy 26%.

Other things being equal, 2027 should be better than 2026 as the company turns an improved order book into revenue and profit.

It anticipates revenue in the Advanced Technologies division will grow by a high teen percentage. Adjusted operating profit margin in the division should improve as depreciation and other fixed costs are spread over more sales. The company says its medium-term divisional target is 12-15%.

That would compare very favourably with 2026, when Advanced Technologies achieved a 3% profit margin.

Profitability at Imaging & Analysis should improve on a creditable 23% profit margin in 2026, due to a reduced cost base and renewed focus on its most profitable products.

Organic investment, for now

Although acquisitions are part of the strategy, since two companies joined Imaging & Analysis in 2024, Oxford Instruments has preferred to invest in research & development and use spare cash to buy back shares.

The company spent almost 9% of revenue on Research and Development in 2025 and 2026. Its immediate priorities are to revamp its camera portfolio, adapt Imaging & Analysis’ metrology tools for use in semiconductor manufacturing contexts, adapt its volume manufacturing technology to the future needs of the semiconductor industry as they develop, and improve the usability of the software that drives its equipment, using AI.

In the rapid growth of the Advanced Technologies’ order book, we have the first sign that the investment in volume manufacturing systems is paying off.

Oxford Instruments’ largest-ever order, secured in 2026, was from a manufacturer of optical transceivers used in data centres. It was followed post-year end by another large order from a semiconductor fabricator.

The adoption of the company’s systems by fabricators like Cohere, which is building plants to equip data centres in Europe and the US, is a boost to Oxford Instruments’ credibility.

- Why Glencore shares are tipped to rally over 50%

- The FTSE 100 stocks paying an extra £1bn of dividends in July

- FTSE 100 ex-dividend dates: July 2026

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

It is tempting to imagine uninterrupted growth as the systems are chosen more widely. It may also be naive.

Hitherto, Oxford Instruments says compound semiconductor fabrication has not experienced the cyclicality associated with silicon, but there is much speculation that investment in data centres fuelled by the AI boom is unsustainable.

In mitigation, Oxford Instruments has diverse customers. Semiconductor revenue from both divisions contributed 32% of total revenue in 2026.

Also, the technology is not limited to a particular type of compound semiconductor. The company is supplying customers in diverse and growing segments of the market like electric vehicle (EV) battery technology, 5G networks, and augmented and virtual reality.

China vs US, academic vs commercial

The geopolitical disruptions that have stifled recent growth are also proving sticky.

Oxford Instruments’ two biggest markets are the US (25% of total revenue) and China (22%), which declined 7% and 8% respectively in 2026. This was partly due to tariffs and trade restrictions on magnets containing rare earth metals.

Adapting to these developments comes at a cost. To mitigate tariffs, Oxford Instruments relocated some atomic force microscope manufacturing from the US to Germany, and outsourced production of some electron microscope detectors for the Chinese market to a local manufacturing partner.

The company also re-engineered products to reduce their reliance on rare earth metals and found non-Chinese sources.

These developments come after tightened UK export restrictions on strategically sensitive technologies prevented their sale in China and wiped £23 million from Oxford Instrument’s order book in 2024.

It may be tempting, but I think it would be rash to conclude that trade has reached a new equilibrium.

The same may be true of academic funding. Across both divisions, orders from academia, which amounted to about 40% of total orders, declined 9% in 2026. Due to changing priorities, governments have reduced funding and we do not know how sticky this will be.

Scoring Oxford Instruments

Richard Tyson, Oxford Instruments’ chief executive of three years, says the business is transformed and positioned for growth, specifically 5-8% compound annual growth rate (CAGR) for organic revenue growth.

He runs a simpler (but hardly simple) business. Having divested one moonshot, Nanoscience, in January, it is focusing on another that is closer to lift off.

Meanwhile, Oxford Instruments is managing its Imaging & Analysis businesses more efficiently.

Worries about geopolitics, academic funding, and the AI boom are largely out of the company’s control. It appears to be managing the things it can control well.

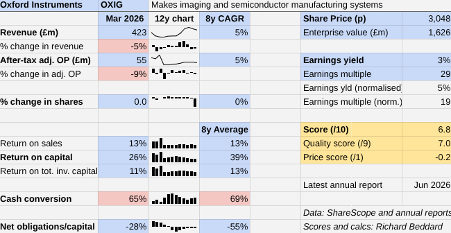

| Oxford Instruments | OXIG | Makes imaging and semiconductor manufacturing systems | 01/07/2026 | 6.8/10 |

| How capably has Oxford Instruments made money? | 2.0 | |||

| Oxford Instruments has increased profit at mid-single digit CAGRs since 2018 by focusing on imaging, analysis, and manufacturing technologies with broad applications in industry and academia. Its chief executive of three years has focused the business on its most profitable and fastest-growing products. | ||||

| How big are the risks? | 2.0 | |||

| Tariffs and trade restrictions may continue to disrupt trade. Changes in government spending priorities may continue to put pressure on academic funding which accounts for about 40% of revenue. The semiconductor market, a focus for growth, may be overheating due to the AI boom. | ||||

| How fair and coherent is its strategy? | 3.0 | |||

| The company has simplified the business and is maintaining high levels of R&D to refresh products and address the rapidly evolving needs of customers, choosing for now to buy back its own shares rather than bolt on acquisitions to Imaging & Analysis. Voluntary staff turnover is consistently below 10%. | ||||

| How low (high) is the share price compared to normalised profit? | -0.2 | |||

| High. A share price of 3,048p values the enterprise at £1,626 million, about 19 times normalised profit. | ||||

| NB: Bold text indicates factors that reduce the score. Bold and italicised text doubly so. The maximum score is 3 for each criterion except price, which has a maximum of 1 (explained here) | ||||

30 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score more than 5 out of 10 to be worthy of long-term investment in sizes determined by the ideal holding size (ihs%).

Autotrader Group (LSE:AUTO), Bloomsbury Publishing (LSE:BMY), and Focusrite (LSE:TUNE) have published annual reports and are due to be re-scored.

| company | description | score | qual | price | ih% | |

| 1 | FW Thorpe | Makes lighting systems for commercial, industrial and public settings | 9.9 | 9 | 0.9 | 9.90% |

| 2 | James Latham | Distributes imported panel products, timber, and laminates | 8.5 | 7.5 | 1 | 7.00% |

| 3 | Hollywood Bowl | Operates tenpin bowling centres | 8.5 | 8 | 0.5 | 6.90% |

| 4 | Renew | Maintains and improves road, rail, water, and energy infrastructure | 8.1 | 7.5 | 0.6 | 6.10% |

| 5 | Jet2 | Flies people to holiday locations, often on package tours | 8 | 7 | 1 | 6.00% |

| 6 | Porvair | Manufactures filters and laboratory equipment | 7.9 | 8 | -0.1 | 5.80% |

| 7 | Solid State | Manufactures electronic systems and distributes components | 7.7 | 7 | 0.7 | 5.40% |

| 8 | Howden Joinery | Supplies kitchens and joinery to builders and online to DIYers | 7.7 | 7 | 0.7 | 5.30% |

| 9 | Anpario | Manufactures natural animal feed additives | 7.5 | 7 | 0.5 | 4.90% |

| 10 | Judges Scientific | Acquires and grows businesses that manufacture scientific instruments | 7.4 | 6.5 | 0.9 | 4.90% |

| 11 | Keystone Law | Operates a network of self-employed lawyers | 7.4 | 7 | 0.4 | 4.80% |

| 12 | Auto Trader | Online marketplace for motor vehicles | 7.4 | 6.5 | 0.9 | 4.70% |

| 13 | Bunzl | Distributes essential everyday items consumed by businesses | 7.3 | 7 | 0.3 | 4.70% |

| 14 | Cake Box | Cake shop franchise and sweet manufacturer | 7.2 | 7 | 0.2 | 4.30% |

| 15 | Volution | Manufacturer of ventilation products | 7.1 | 8.5 | -1.4 | 4.20% |

| 16 | Churchill China | Manufactures tableware for restaurants etc. | 7 | 6 | 1 | 4.00% |

| 17 | Focusrite | Designs recording equipment, synthesisers and sound systems | 7 | 6 | 1 | 4.00% |

| 18 | YouGov | Surveys public opinion and conducts market research online | 6.9 | 6 | 0.9 | 3.90% |

| 19 | Quartix | Supplies vehicle tracking systems to small fleets | 6.9 | 7 | -0.1 | 3.80% |

| 20 | Oxford Instruments | Makes imaging and semiconductor manufacturing systems | 6.8 | 7 | -0.2 | 3.50% |

| 21 | Games Workshop | Designs, makes and distributes Warhammer. Licences IP | 6.7 | 8.5 | -1.8 | 3.40% |

| 22 | Goodwin | Casts and machines steel and processes minerals for niche markets | 6.6 | 7.5 | -0.9 | 3.20% |

| 23 | Cohort | Manufactures/supplies defence tech, training, consultancy | 6.6 | 8 | -1.4 | 3.10% |

| 24 | Softcat | Sells software and hardware to businesses and public sector | 6.5 | 7 | -0.5 | 3.10% |

| 25 | Macfarlane | Distributes and manufactures protective packaging | 6.5 | 5.5 | 1 | 3.00% |

| 26 | Bloomsbury Publishing | Publishes books and educational resources | 6.4 | 7.5 | -1.1 | 2.80% |

| 27 | Advanced Medical Solutions | Manufactures surgical adhesives, sutures and dressings | 6.2 | 6.5 | -0.3 | 2.50% |

| 28 | Tristel | Manufactures hospital disinfectant | 5.9 | 8 | -2.1 | 2.50% |

| 29 | 4Imprint | Customises and distributes promotional goods | 5.9 | 8 | -2.1 | 2.50% |

| 30 | Renishaw | Makes tools and systems for manufacturers | 4.6 | 6.5 | -1.9 | 2.50% |

Click on a share's score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, and ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns Oxford Instruments and many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine and Share Sleuth, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.