"Enormous potential" for agriculture funds

22nd April 2014 12:21

by Iain Murray from ii contributor

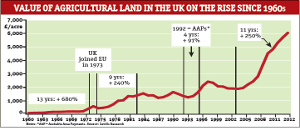

Savills' head of rural research, Ian Bailey, adds a fifth reason - short supply. "If you go back 50 years we were turning over about 2.5% of all available agricultural land every year, but now it is only about a quarter of 1%. So the market is very tight. And of the land that comes onto the market, some 50% is bought by farmers wanting to expand their businesses."

Investor spectrum

Tom Raynham, head of the agricultural investment acquisitions team at estate agent Knight Frank, says land is an asset that attracts a spectrum of investors. "They include people who might not be able to buy a whole farm, but have money to invest in a fund that will then go out and buy a farm.Then there are private individuals who are looking either to expand on their own land holdings or just invest into land for the first time. Then there are corporations, institutions and pension funds." An example of a farm asset manager is Manor House Farms, which set up Farm Funds in 2009. It runs farms on behalf of a pool of investors, each of whom becomes a "farmer" with access to the farmland assets and activities. The system works rather like a racehorse consortium in which part-owners enjoy the asset but leave its management to experts. Among the attractions of land, says Ian Bailey, is the fact that it does well in recessionary times. "The fundamentals of food production and food security are high on the political agenda. Land may also produce energy with solar cells and windfarms. And you can live on it, enjoy it, and raise your family on it. It's a very diverse product."Moreover, with certain caveats, it's an asset that you can pass on as a tax-free inheritance. In pure monetary terms, it's an investment that delivers impressive capital gains over the long term, but a relatively unimpressive annual yield of 2% or less.

If you want to get rich you should be buying farmland"Jim Rogers

For the more adventurous investor there are opportunities overseas. DGC Asset Management specialises in the "identification, acquisition, development and operation of productive agricultural property and distressed real estate". Its managing director David Garner says: "Our overall remit is to look at small-scale assetbacked projects where we can add value to existing land assets and the production of high-value crops." As an example of potential returns, Garner cites a two-year project in Australia where DGC conducted research and due diligence to find the most appropriate location, strategy and structure, as well as a farmer to contract and operate the land.

"We generated an annualised net return after all fees and costs and local taxes of 9%-18% over two years." Buying land is not the only way to invest in agriculture. There are a number of funds that specialise in the food industry. The three main players in the UK are the fund, and . Their performance of late has been disappointing. But agriculture is not a short-term story and the managers of these funds urge investors to bear in mind the powerful logic of the macro case for the food industry. Henry Boucher, who runs the Sarasin fund, says: "Compared with the sharp re-rating of many developed market global equities last year, food has been out of favour. But we see enormous potential for companies to generate real shareholder value through the inexorable growth in the food economy. Our thematic approach helps us to focus on these opportunities and to capture the profits generated over time."

One reason why food is subject to swings in investor sentiment is the volatility of soft commodity prices, but according to James Govan, manager of the Baring fund, such fears are largely misplaced. "We can basically divide the agriculture universe into three broad segments - upstream, midstream and downstream. Upstream are fertiliser, crop and seed protection and machinery companies, as well as plantations and farms. These companies tend to be positively correlated to soft commodity prices, or at least benefit from strong soft commodity prices."

Midstream are the processing and distribution companies, which own grain-storage assets as well as processing corn and soybean into things like ethanol. Meat companies, too, fall into the midstream. The midstream tends to benefit from greater volumes in grains and edible oils and lower crop prices. Finally, the downstream firms include food manufacturers such as Nestlé and Unilever and retailers such as Tesco. "So, yes the fund will move on soft commodity prices, but within it there is a natural hedge. We are not dependent on rising crop prices in order to do well. For example, last year we had record corn production in the US, bumper crops in both South and North America, so we moved some of the allocation of the fund from the upstream to the midstream sectors," explains Govan.

Big risks with ETCs

You can also invest in food through exchange traded commodities (ETCs) that track the performance of a single commodity or an index. ETCs are traded in the same way as shares. There are also basket ETCs that track diff erent commodities. However, the value of ETCs is highly volatile. Risk-averse investors are better advised to stick with equities, which is exactly what the Baring fund does. When it comes to investing in food, then, we can discount the words of the economist John Maynard Keynes, who commented that in the long run we are all dead. Without agriculture we would all be dead in the short run.