SIPPs compared: ii vs Hargreaves Lansdown

Thousands of people are switching from HL to ii. Should you?

Two SIPPs; two very different fees. See how our pensions compare and if you could be better off by transferring to ii.

Important information: The ii Personal Pension (SIPP) is for people who want to make their own decisions when investing for retirement. As investment values can go down as well as up, you may end up with a retirement fund that’s worth less than what you invested. Usually, you won’t be able to withdraw your money until age 55 (57 from 2028). Before transferring your pension, check if you’ll be charged any exit fees and make sure you don't lose any valuable benefits such as guaranteed annuity rates, lower protected pension age or matching employer contributions. Tax treatment depends on your individual circumstances and may be subject to change in the future. This information is not a personal recommendation, if you’re unsure about opening a SIPP or transferring your pension(s), please speak to an authorised financial adviser.

What’s the difference between ii and Hargreaves Lansdown?

“Thousands of SIPP investors have already moved billions of pounds from Hargreaves Lansdown to interactive investor (ii), so it’s natural to wonder how the two differ and, crucially, which is best for you.

There are many similarities, with both offering a range of investment accounts, including ISAs, Trading Accounts and – yes – Self-Invested Personal Pensions (SIPPs). And through these accounts, you can easily invest in your choice of shares, bonds, funds and ETFs.

But when comparing ii vs Hargreaves Lansdown, there’s one key feature that may make all the difference: what you’ll be charged.”

Victoria Scholar, Head of Investment at ii

Compare our SIPPs at a glance

Use our table to compare key features to help you find the right pension for you.

| ii Personal Pension (SIPP) | Hargreaves Lansdown SIPP | |

|---|---|---|

| Platform charge | Flat fee | Percentage of your portfolio |

| Which? Recommended | ✔ | ✘ |

| Free regular investing | ✔ | ✔ |

| Invest in funds & shares | ✔ | ✔ |

| US & International Shares | ✔ | ✔ |

| Managed pension investments | ✔ | ✔ |

| App-based share dealing | ✔ | ✔ |

| Free pension withdrawals | ✔ | ✔Extra platform charges may apply |

| Transfer out exit fees | No exit fees | No exit fees |

| Hold foreign currency | ✔ | ✘ |

| UK-based customer support | ✔ | ✔ |

| Dividend reinvestment | ✔ 99p per trade | ✔ |

| Family features | Gift free accounts | ✘ |

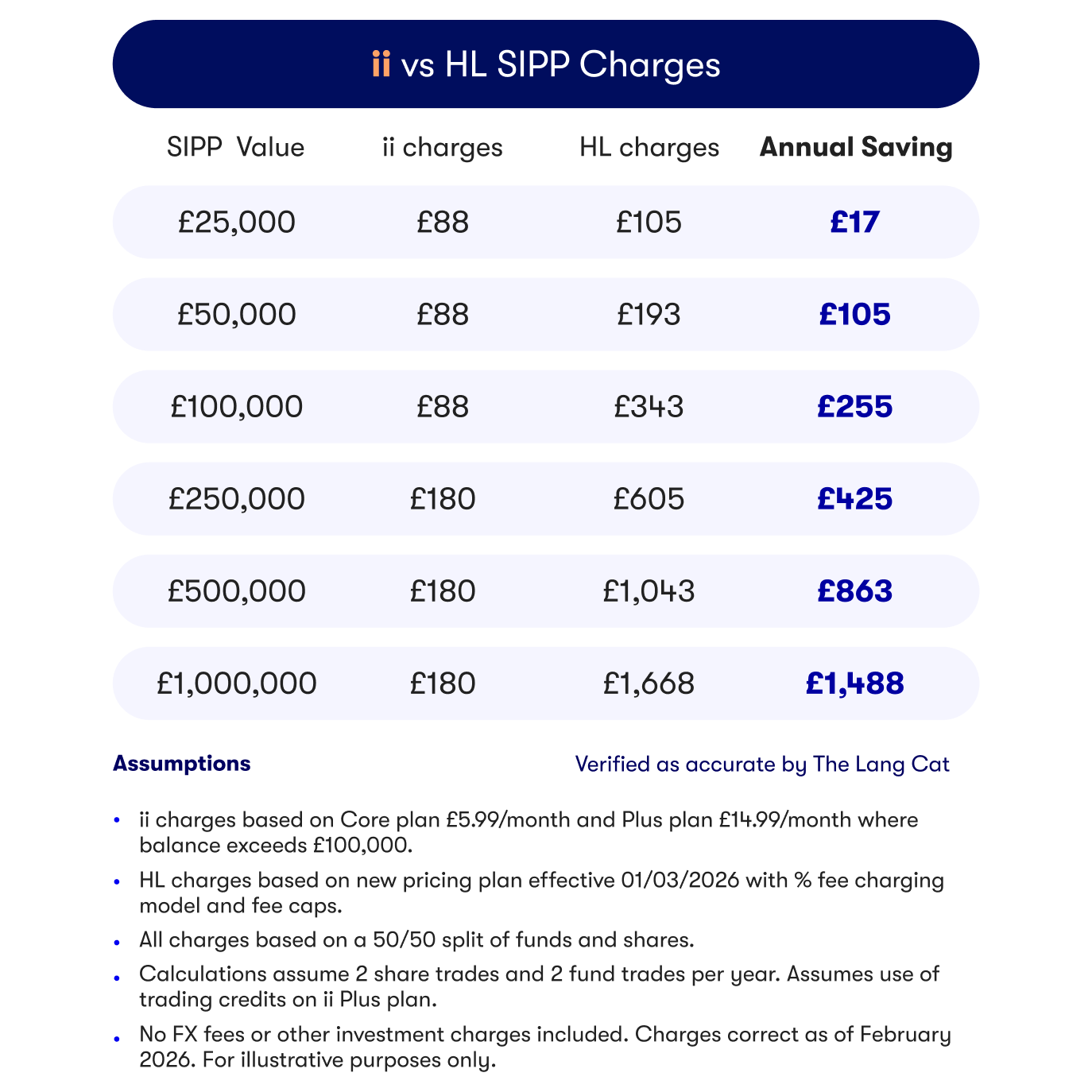

ii vs HL: SIPP charges compared

If your pension pot is larger than £20,000, ii may be cheaper than Hargreaves Lansdown.

ii charge a flat fee

Unlike percentage-based fees charged by many providers, with ii you only pay one low flat-fee for all your investment accounts: Personal Pension, Shares ISA and Trading Account. Our most popular plans are:

- Core: invest up to £100,000 across all ii accounts for £5.99 a month.

- Plus: no investment limit for £14.99 a month, with extra benefits, including free ii Family accounts and Junior ISAs.

Hargreaves Lansdown charge a percentage fee

Funds: Annual charge to hold funds is tiered and will increase until a value of £2m is reached:

- 0.35% on the first £250,000 of funds

- 0.25% on the value of funds between £250,000 and £1m

- 0.1% on the value of funds between £1m and £2m

- No charge on the value of funds over £2m

Shares: Annual charge to hold shares, bonds, investment trusts, ETFs:

- 0.35% (capped at £150 per annum)

What about trading charges?

With ii, trades usually cost £3.99. Plus plan members benefit from a reduced £1.49 trade fee for mutual funds and also get £3.99 in free trading credits each month. There are no trading charges for regular investing.

With Hargreaves Lansdown, trading charges start at £6.95 for shares, ETFs and other equities and can drop down to £3.95 for frequent traders (20+ trades made in the previous month). Fund trades are £1.95.

ii vs HL: taking money out of your pension

With ii, you can withdraw cash from your pension without any additional charges using tax-free cash, drawdown & lump sums.

With Hargreaves Lansdown, there are no additional charges - as long as you aren't planning to move only some of your SIPP into drawdown - read on to find out more.

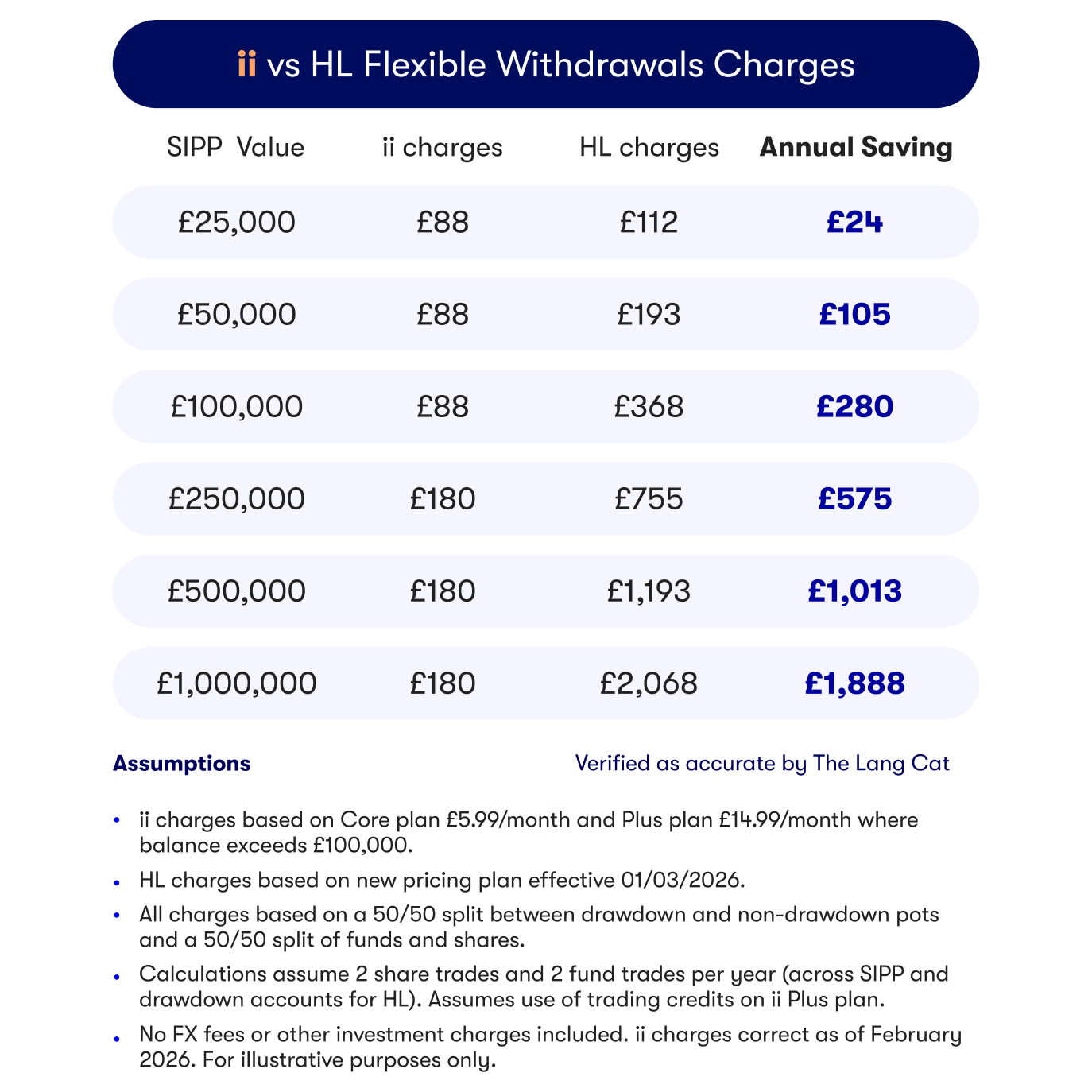

ii vs HL: Flexible pension withdrawals

One of the key benefits of a SIPP is the flexibility it gives you when you need to take money out of your pension. For example, many SIPP investors choose to move only part of their SIPP into drawdown, take a small amount of tax-free cash or blend both drawdown and lump-sum withdrawals.

With ii, there are no additional fees when splitting your SIPP into drawdown and non-drawdown pots. It's all included in the same flat fee and the investments are simply allocated proportionally to the amount of pension you choose to hold in each pot.

With Hargreaves Lansdown, if you need this flexibility, drawdown and non-drawdown pots will need to be managed using two separate accounts, each of which will be charged separately.

This could mean increased charges due to HL's percentage-based fees applying to both pots. In some cases, the charges could increase by as much as 100%. By using two accounts, the investments are also held and managed separately.

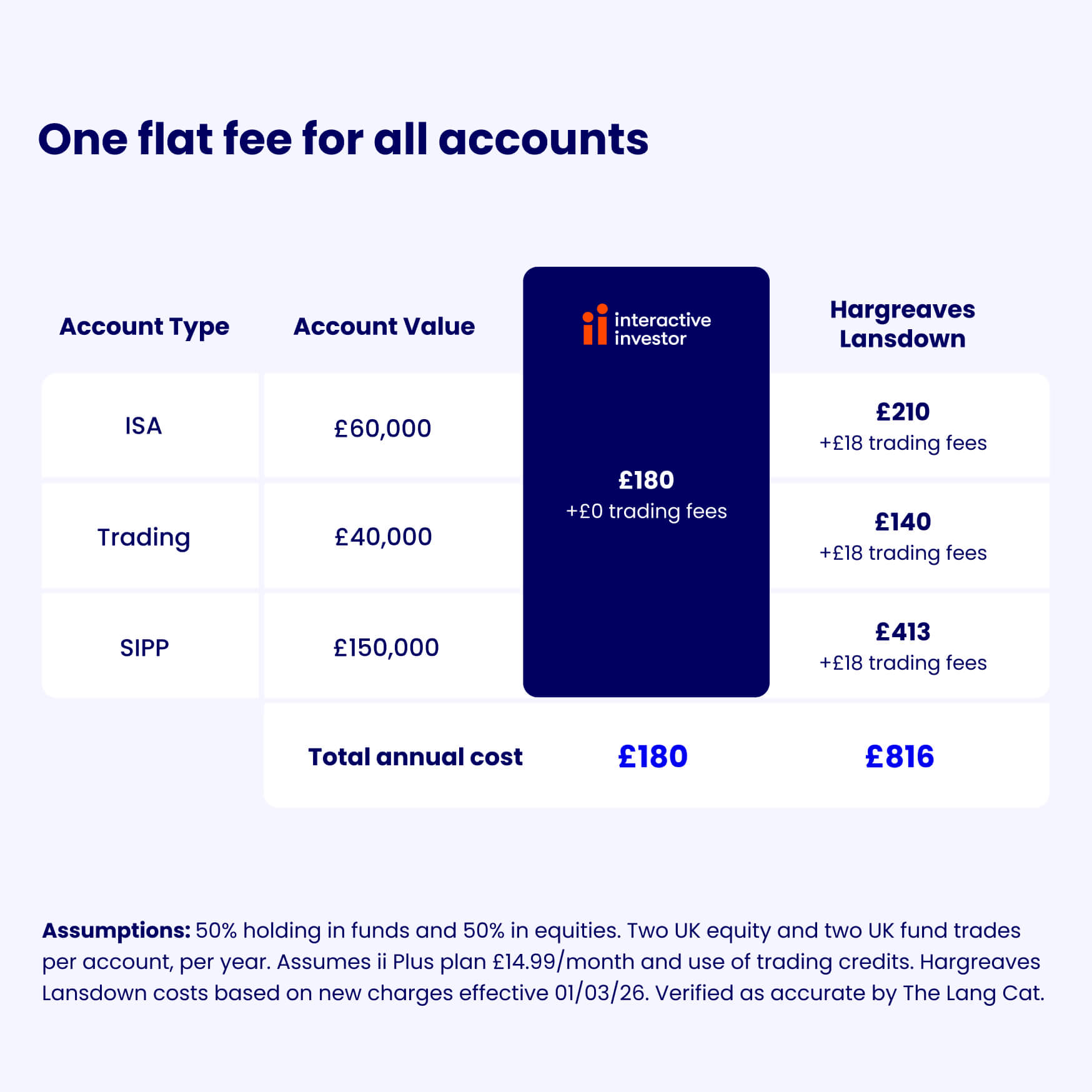

Even better when you consolidate all of your accounts to ii

The flat-fee savings only get better if you consolidate your investments with us. Most platforms charge on a percentage basis, meaning the more you invest the more you pay.

We're different. Our one flat fee for all of your accounts means that the more you keep with us, the more you save.

Whether you are looking for an ISA, Junior ISA, Trading Account or a SIPP, we’ve got you covered.

Why Jerome transferred from Hargreaves Lansdown to ii

“I looked at the fees that were provided from my previous provider, Hargreaves Lansdown. ii has a flat fee you pay once a month, so in terms of understanding what the costs are, it's transparent. That's why I'm with ii.”

Jerome was with Hargreaves Lansdown. He wanted his pension on one platform to make retirement planning simpler. For him, our flat fee model was easy to understand and transparent.

Investing should feel rewarding

Start investing with ii and give your savings more time to grow this summer.

Open an ii Personal Pension (SIPP) and enjoy £200 cashback when you deposit or transfer a minimum of £20,000. See more details on this offer.

Offer ends 31 July 2026. New customers only. Terms and fees apply.

Important information: It’s important to take your time before transferring your pension. Make sure to consider what the best option is for you. Don’t transfer just to qualify for the offer, and don't rush any decision to meet the offer deadline. We periodically run offers, and there will likely be other opportunities in the future.

Before transferring your pension, check if you’ll be charged any exit fees and make sure you don't lose any valuable benefits such as, guaranteed annuity rates, lower protected pension age or matching employer contributions.

How to transfer from HL to ii

Every year, thousands of people transfer their pensions from HL to ii looking for lower charges and wider investment options.

Follow our step-by-step guide to start your transfer online in minutes.

Before you transfer your pension

Transferring a pension to a SIPP can be a great choice for many reasons. It can save you money, improve your investment options and give you greater flexibility at retirement. But there are some important things to check and consider before you make your move.

Check 1: Will it cost you anything to transfer?

It’s always free to transfer with ii from our side, and Hargreaves Lansdown don't charge exit fees either.

Check 2: Will you lose any benefits if you transfer?

Some pensions have special guarantees and benefits. Before transferring, make sure you won't lose any of the following:

- Guaranteed annuity rates

- Lower protected pension age

- Matching employer contributions

Check 3: Should you take pension advice before transferring?

If you’re unsure about transferring your pension(s), please speak to an authorised financial adviser who specialises in pensions. And if you’re over 50 and thinking about retiring soon, you can also book a free and impartial guidance session with Pension Wise, part of the government’s MoneyHelper service. They can help you understand your options and decide whether a transfer is right for you.

ii vs HL SIPP FAQs

Yes, you can usually transfer all or some of your pension investments from HL to the ii SIPP with ease using our online transfer process.

You can transfer cash or investments directly - this means you won't have to sell your investments and re-purchase them when you make your transfer. If the investments you wish to transfer are not available on the interactive investor platform you can choose to sell these investments and transfer as cash.

Yes, you can transfer pensions in drawdown to the ii SIPP with ease.

Please note you may not be able to take an income from your pension during your transfer. As well, if you plan to hold both drawdown and non-drawdown pots in your ii SIPP, you cannot allocate specific investments to each pot separately. This means that the value of each pot will change in line with the overall performance of all the investments held in your SIPP. Learn more about how we split your drawdown and non-drawdown pots.

Pension drawdown pots must be transferred in full. Partial transfers of drawdown (crystalised) funds are not permitted. If you hold both a drawdown (crystallised) pot and an non-drawdown (uncrystallised) pot, you can transfer these to interactive investor.

Transferring a pension usually takes 2 to 6 weeks to complete for a cash transfer, going up to 8 to 12 weeks if you’re transferring your investments.

We will keep you updated throughout with regular emails, and you can always reach out if you have any questions about how the transfer is going.

There’s no charge to transfer either stock or cash from Hargreaves Lansdown to interactive investor and we do not charge for the transfer process.

We will send you regular updates on how your transfer is progressing. You can keep track of your transfer in your account, just log in and go to Track my transfers. If you have any questions during the course of the transfer, you can always get in touch with our UK customer service team.

You can easily get in touch with our team for any questions you have. If you're already a customer, feel free to send a secure message from your account page.

The best number to reach us on is 0345 607 6001. Or, if you’re calling from abroad, +44 113 346 2370. Our lines are open 7.45am to 5.30pm (GMT), Monday to Friday.