Exchange-traded funds

Track the markets with exchange-traded funds (ETFs)

Discover why ETFs are a popular, cost-effective investment type. Review ideas and insights from our experts before choosing the ETFs to expand your portfolio.

Important information: As investment values can go down as well as up, you may not get back all of the money you invest. If you're unsure about investing, please speak to an authorised financial adviser. Please note images displayed are for illustrative purposes only.

What are ETFs?

Exchange-traded funds or ‘ETFs’ are investment funds that can be traded on a stock exchange in the same way as shares.

Trading in ETFs is a low-cost, easy way to track a broad basket of shares using an index, such as the FTSE 100 or S&P 500. You can also track a wide range of other types of investments, like bonds, property and currencies.

When it comes to tracking the performance of commodities, such as precious metals or energy, investors can buy a similar type of investment called exchange-traded commodities (ETCs).

Most popular ETFs

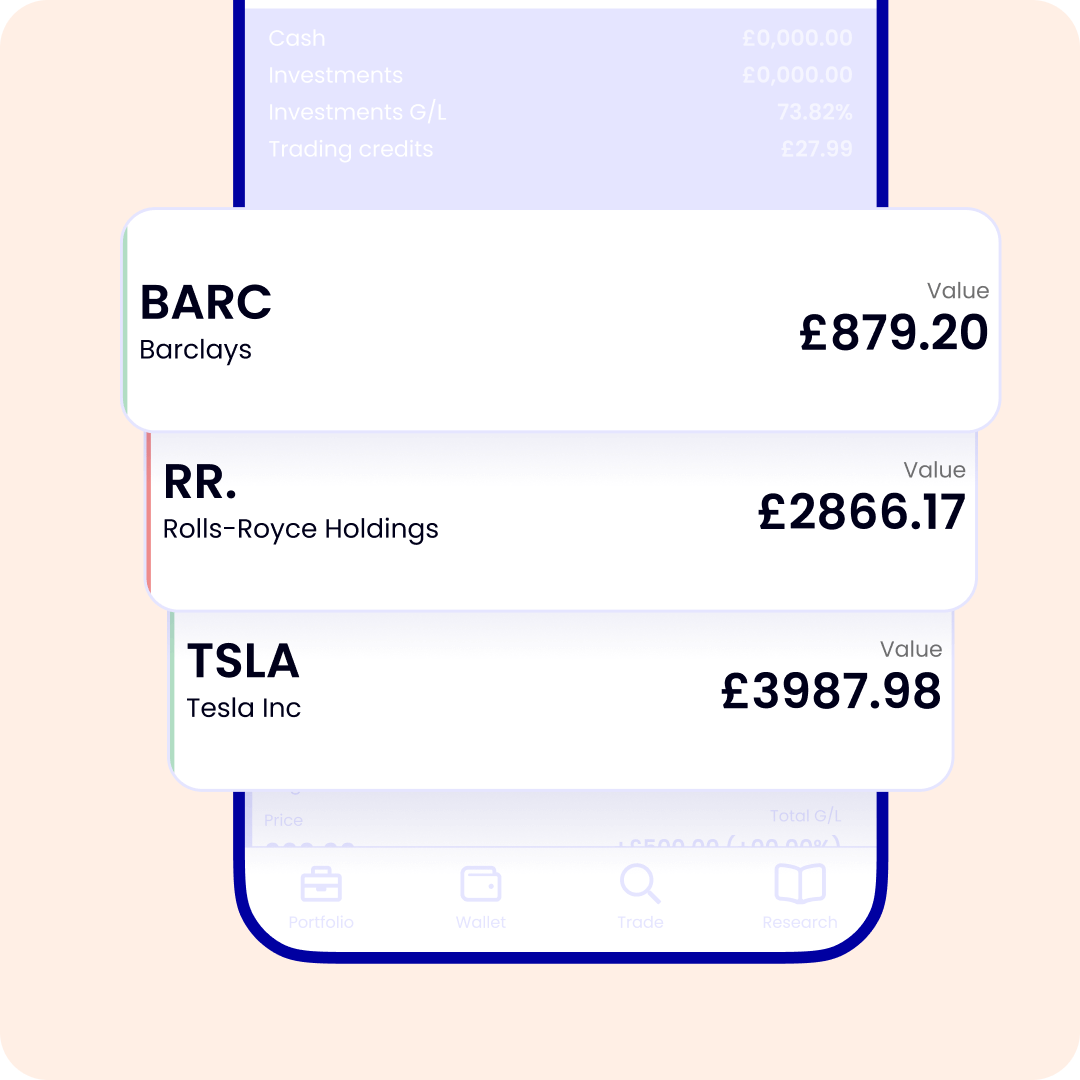

Want to see what other investors are buying? Here’s our list of the most-bought ETFs by ii customers over recent months. You can also see which ETFs are performing best on our top ETFs page.

Most-bought ETFs by ii investors

- Vanguard FTSE All-World ETF USD Acc GBP (LSE:VWRP)

- iShares Physical Gold ETC GBP (LSE:SGLN)

- Vanguard S&P 500 ETF USD Acc GBP (LSE:VUAG)

- Vanguard S&P 500 UCITS ETF GBP (LSE:VUSA)

- VanEck Semiconductor ETF GBP (LSE:SMGB)

- iShares Physical Silver ETC GBP (LSE:SSLN)

- iShares Core FTSE 100 ETF GBP Dist (LSE:ISF)

- iShares Core MSCI World ETF USD Acc GBP (LSE:SWDA)

- Vanguard FTSE All-World UCITS ETF GBP (LSE:VWRL)

- Invesco EQQQ NASDAQ-100 ETF GBP (LSE:EQQQ)

Source: interactive investor. Note: the top 10 is based on the number of purchases in real time between 1 April to 30 June 2026. Our most popular investments should not be taken as personal recommendations or advice on whether to buy or sell a particular investment.

Why invest in ETFs?

ETFs are a simple and popular way to invest in a wide range of companies without picking individual shares. Our Funds and Investment Editor, Kyle Caldwell, explains why.

“Unlike an active fund or investment trust, ETFs are usually passively managed. This approach means they track the performance of an index of stocks, rather than trying to ‘beat the market’. As a result, ETFs often come in at a lower cost that other funds or trusts.

Another benefit is that ETFs are traded on stock exchanges, meaning they can be bought and sold quickly throughout the day. Other types of funds can take longer to buy and sell.”

Helping you find your next investment

Take a look at our recommended investment lists and options to inspire your next move.

Highly Rated Funds

The Highly rated funds tool is a selection of funds, investment trusts and ETFs that hold strong analyst ratings from our Data provider, Morningstar.

Quick-start Funds

Get off the mark quickly, with one of these low-cost, multi-asset funds. A simple way to help you start investing.

Aberdeen funds and trusts

Take a look at the Aberdeen funds and investment trusts available on the ii platform.

ii’s investment trends and insights

Our market-leading team of experts regularly gather and review the investment trends of over 500,000 ii investors.

Discover the team’s latest insights to help build your knowledge as well as your portfolio.

Great choice, even greater value

Enjoy access to one of the widest ranges of ETFs on the market. Choose from our wide range of investments and even save on trading fees with our free regular investing service.

Expert lists and top trading tips

Our investment experts pour over the markets daily, so you don’t have to. Invest smarter with better insights, ideas and our most-traded lists of funds, ETFs and shares.

On-the-go investing made easy

Never miss an investment opportunity with our easy-to-use mobile app. Track the markets from your pocket and adjust your portfolio at the touch of a button.

Over 25,000 reasons to invest with ii...

Join over 500,000 investors, over 50% of whom have been with us for more than 10 years. See why Investors' Chronicle named us a 5-star platform and their Editor's Choice.

How to invest in ETFs with ii

To start buying ETFs with ii, you’ll first need to open an account. Choose from our Stocks & Shares ISA, Self-Invested Personal Pension (SIPP) or Trading Account.

You can open your account in just 10 minutes, either here on the website or through our mobile app.

You’ll need to add cash to your account to buy your ETFs. You can do this by making a one-off payment or setting up a monthly direct debit.

Research the ETFs you’re interested in and select those you want to invest in. If you need help choosing, remember to explore our expert insights and ideas.

When you know the ETFs you want, it’s time to buy.

With the cash ready in your account, you can place your order to buy your ETF. If you want to invest a little in the same ETF each month, remember you can always do this with our free regular investing service.

ETF FAQs

ETFs are traded on a stock exchange, just like shares. That means you can buy and sell them in the very same way - using an investment platform, like ii, and within trading hours.

You'll need to open an investment account first. Then, research and choose the ETFs you want to buy. Always remember to check the costs of investing, including trading fees and platform charges.

Though they’re called exchange-traded funds, ETFs work more like shares. You can trade them on an exchange which means you can buy and sell them throughout the day.

But ETFs do have similarities to traditional funds. ETFs invest in a range of underlying assets and will have a management charge attached to them too. The management charge of ETFs is usually lower than other types of funds, due to the fact that no one actively manages them. Instead, ETFs simply track the performance of their underlying basket of assets.

As ETFs track a collection of investments, you may not need to invest in many to achieve a well-balanced investment portfolio.

But it’s important to pay attention to your ETF's underlying investments, to ensure your overall portfolio includes a diverse range of sectors, themes and regions. This can help you manage your risk of loss.

The ETFs you choose to invest in should reflect your appetite for risk and form part of a well-balanced investment portfolio.

With ii, you have thousands of ETFs to choose from. If you’re not sure where to start, lean on our experts for some investing inspiration and ideas.

You can also see what other investors have been buying and the current best-performing ETFs on our top ETFs page.

Beginner investors may want to use ETFs to gain exposure to major stock market indices, such as the S&P 500 or FTSE All Share. Broad exposure to the major stock markets can play a core part in many beginner investor portfolios. And ETFs provide a relatively cheap and easy way to achieve this.

Some ETFs that hold stocks will pay dividends and distribute these to investors. In fact, a special type of ETF, known as high-dividend ETFs, focuses specifically on stocks that pay high dividend yields.

ETFs that pay dividends will usually pay investors on a quarterly basis. Investors can receive their share of the dividends as cash or additional units of the ETF.

Many investors choose to reinvest their dividends to compound the growth they see in their ETF investment.

ETFs come in all shapes and sizes. The most traditional are those that track established stock market indices, such as the FTSE 100 or NASDAQ. There are also those that track bond market indices and others that reflect the performance of baskets of commodities, property or currencies.

Many popular ETFs now track certain business sectors within a wider index - for example, those which track the finance businesses of the S&P 500.

Thematic ETFs are also widely available. For example, a popular theme in recent years has been computing. A computing ETF will usually track a computing index, comprised of - you guessed it - computing companies.

Another ETF option is known as ‘smart beta’ in industry jargon. These ETFs do not track shares by market capitalisation, as a fund tracking, say, the FTSE 100 index would. Instead, they decide which shares to track by targeting those that match certain goals. For example, some smart beta ETFs follow a basket of companies that are reliable dividend payers, while others target the highest-yielding shares on a particular index.

When you buy and sell ETFs with ii,you’ll usually pay a one-off trading fee. The amount depends on the type of investment and which price plan you're on. Please see our charges for details.

You can save on your trading charges if you use our free regular investing service when buying ETFs.

Even though ETFs trade on the stock market, you won’t pay any stamp duty when buying them. This is an important difference between ETFs and shares.

Keep up to date with our ii newsletter

The markets move fast. You can move faster. Keep your finger on the pulse with impartial, expert content from our award-winning investment journalists.