Global Economic Outlook: of resilience and recessions

22nd March 2023 12:07

by abrdn Research Institute from Aberdeen

The resilience of economic activity and the strength of underlying inflation at the start of 2023 imply that central bank policy rates – especially the Fed funds rate – need to rise higher.

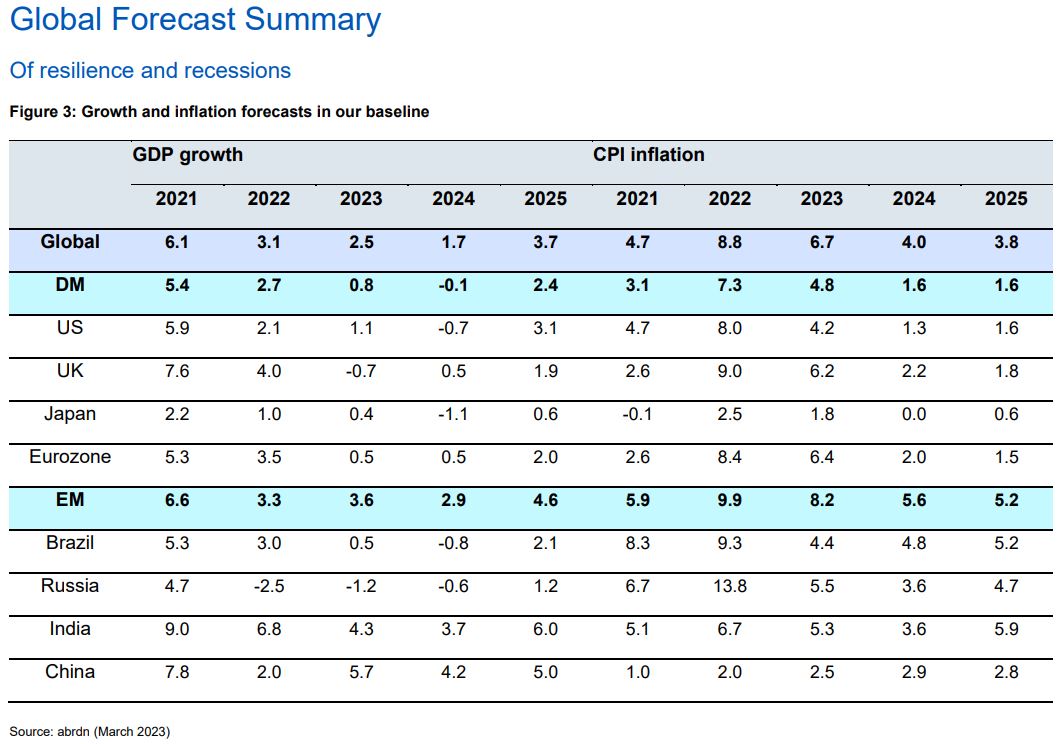

Global economic activity and underlying inflation have been resilient at the start of this year.

However, rather than undermining our forecast for an eventual US (and broader developed market) recession, we continue to think one is necessary to correct this overheating.

Moreover, we think that the size of the rate-hiking cycle will be sufficient to generate this recession. Recent financial stability concerns add to the evidence that one will occur.

Markets have partially come round to our view that a sharp interest-rate cutting cycle will begin later this year. But we think the scale of these cuts is still not fully appreciated.

By contrast, China’s economy is rebounding fast, and it has spare capacity to sustain strong growth throughout our forecast period. Indeed, we see growth in China exceeding consensus expectations this year.

While the spill overs from a strong China into broader emerging markets will be more moderate than usual, all this adds up to economies with increasingly diverging trajectories.

Recession’s necessary

We think a US recession is necessary to tackle overheating in the US labour market and to bring underlying inflation back to levels more in line with the Federal Reserve’s (Fed) target.

The US economy suffers from excess demand, amid very low unemployment that’s below the natural jobless rate. In our baseline, or most likely, scenario we don’t think that correcting this imbalance can occur in a benign way (e.g., via fewer job vacancies).

Instead, a more painful rebalancing must occur through higher unemployment. Moreover, we believe that the Fed would be willing to inflict this as the cost of restoring price stability. This has long been the thinking behind our ‘Fed kills the cycle’ call.

Resilient US (and global) economic data and persistent inflation at first appear to be at odds with a US recession forecast. However, the latest economic numbers increase our conviction in the necessity of an eventual recession because they add to the evidence of overheating.

More signs of overheating

The strength of incoming activity data is clearest in the global composite Purchasing Managers’ Index (PMI), which rose to 52.1 in February – putting it back into expansionary territory for the first time in eight months.

In the US, the PMI business survey also returned to expansion in February, while the alternative Institute for Supply Management (ISM) survey paints a similar picture.

US personal consumption was also strong at the start of 2023, while the labour market has added a large number of jobs. Even industrial production, goods orders and homebuilder confidence were a little better. This improvement, in part, reflects seasonal distortions. But it’s clear the US economy has picked up pace.

Better activity data is leading to persistent inflation. Revisions to the US Consumer Price Index (CPI) series mean that what had previously looked like a gradual cooling in core inflation over 2022 is now much less convincing.

Meanwhile, core Personal Consumption Expenditures (CPE) inflation rose to 4.7% in January. Stripping out falling energy prices and globally-generated goods disinflation, services inflation remains far too hot.

Financial stability concerns

A fresh concern during March has been the failure of a mid-sized US bank and worries about the health of the broader banking sector. Rate-hiking cycles are the proverbial 'tide going out', and they have a way of exposing hidden vulnerabilities in the financial system.

While policymakers will try to contain the negative spill overs, we think this makes the US recession we are forecasting even more likely.

It increases the probability that there's sufficient monetary-policy tightening working its way through the system and starting to exert a drag on demand. It's also causing a broad tightening in financial conditions, which will weigh on the real economy.

Elsewhere in the world…

The Eurozone economy has also proven relatively resilient. It has avoided a deep winter recession, while the composite PMI rose to 52.3 last month. This improved picture reflects the sharp fall in gas prices. However, core inflation is still rising, hitting 5.6% in February – an all-time high.

Meanwhile, China’s re-opening rebound is gathering pace. Despite the lack of hard data at the start of this year, other sources of information point to a sizeable recovery, and our activity index is strengthening. This is consistent with a V-shaped growth surge driven by consumption and services.

We’re a bit more cautious as to the extent of any stimulus policies above and beyond re-opening itself. The spill over effects of Chinese growth into emerging markets (EMs) should also be weaker than before, given the services-led nature of this rebound.

But we’re above consensus on Chinese gross domestic product (GDP) growth in 2023 and we think it will comfortably exceed the 5%-target policymakers have set.

Central banks in focus…

Central banks have the unenviable task of navigating both the eruption of financial stability concerns, and the unfinished business of taming inflation.

While market pricing has been very volatile, our view is that there are still further rate hikes to come. In the US, we're expecting a terminal fed funds rate of 5.5%. We think the European Central Bank (ECB) will hike to 3.75%, with the Bank of England raising rates to 4.5%.

However, our stronger conviction is that the large rate-hiking cycles that have occurred over the past 18 months will soon exert a big drag on economies. History suggests that hard landings follow on from rate hikes.

…in Japan

Near-term monetary policy in Japan is also uncertain. There has been substantial market pressure on the Bank of Japan’s (BoJ) yield curve control (YCC) framework amid speculation over its end.

We’re not convinced about the fundamental macroeconomic need for tighter monetary policy in Japan. However, market distortions there are so large that incoming Governor Kazuo Ueda may use a narrow window of opportunity to change the policy.

Our baseline scenario is for a widening of the tolerance band on 10-year Japanese government bond yields to +/-75 basis points. Abandoning YCC is unlikely but possible, especially if any tweaks aren’t seen as credible by financial markets. Either way, BoJ monetary policy is also set to tighten in practice.

…in EMs

The EM-rate cycle is close to a turning point, given that hiking generally began sooner and core inflation is coming off the boil.

But the credibility of policy pivots varies considerably. The most credible EM central banks include Brazil, Chile and Czechia. They are the most likely to follow the Fed in cutting this year.

The likes of Mexico, the Philippines and India could face currency pressures if they pause too early, given the persistence of their underlying inflation.

Underlying inflation pressures are still very strong in much of Eastern Europe, especially Poland and Hungary, where we expect more rate hikes.

What will recession look like?

We’ve pushed back our forecast start date for a US recession by three months to the third quarter. But we’re still expecting a contraction that takes some 2% off US GDP.

Adjusted for lower-trend growth, this is at the milder end of US recessions. But it’s still a meaningful shock, with negative global spill overs.

Based on our forecasts, the Eurozone, UK, Japan, Brazil and Russia will also fall into recession either this year or in 2024.

That said, we wouldn’t characterise the outlook as a global recession given the strength of China and the divergence between developed markets and parts of the EM world.

What’s more, by mid-2024 and into 2025, we would expect global growth to be very strong coming out of earlier weakness.

When rates fall…

Headline inflation is already falling almost everywhere and should continue to decline this year on weaker energy prices.

However, it’s recession and the associated rise in unemployment, that ultimately bring down underlying inflation to (and even below) central bank targets.

We think central bank-rate cuts are likely later in 2023 and throughout 2024. Indeed, while market pricing has moved to incorporate a cutting cycle, we hold the non-consensus view that the Fed could go all the way back to the effective lower bound.

A cutting cycle of this size would be in line with historical responses to recessions. Interest rates around the lower bound are also what a variety of policy rules suggest as appropriate given our growth and inflation projections.

That said, we expect the cutting cycles to be slightly less deep in the Eurozone, UK and many EMs.

No more soft landing?

We’ve just described our base case scenario but it’s only one of several plausible outcomes. We’ve dubbed our most likely alternative scenario ‘Fed walks the tightrope’ – a form of soft landing. A lot would have to go right for the Fed to pull off a soft landing, and it would buck historical precedent.

Nevertheless, during a period of below-trend but above-zero US growth, the labour market adjustment that occurs through fewer job vacancies (rather than higher unemployment), and a continuation of the recent moderation in wage growth, could make this scenario possible.

Another important scenario is what many in financial markets are calling a ‘no landing’. Both growth and inflation could remain elevated for longer. This would mean even larger interest-rate hikes, with the fed funds rate potentially rising above 7%. Eventually the economy would come back down to earth with a thud.

abrdn's Research Institute produces original research at the intersection of economics, policy and markets.

ii is an abrdn business.

abrdn is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.