Global Economic Outlook: Rolling on or rolling over?

The US economy continues to be resilient. Europe is staring at recession. China faces headwinds, while other EMs diverge. Global economies present a mixed picture. Read on to find out more…

21st September 2023 09:59

by abrdn Research Institute from Aberdeen

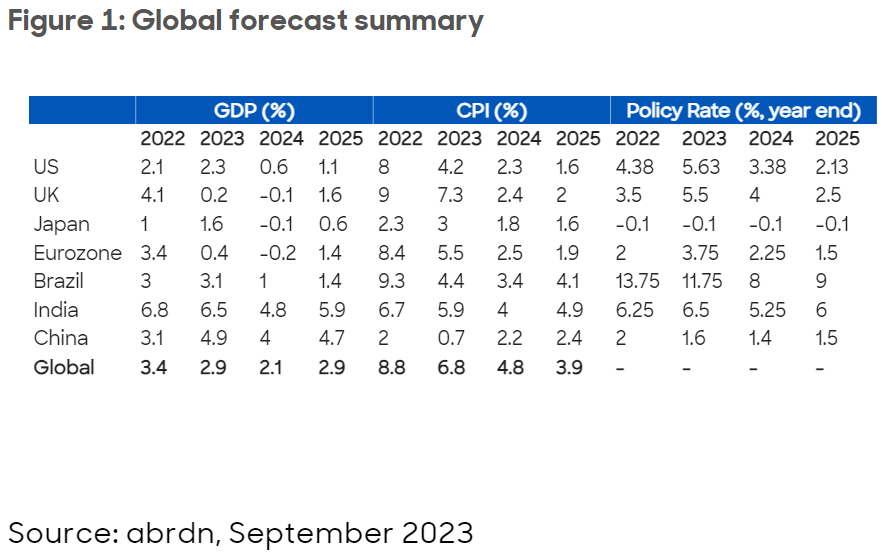

The US economy may continue to demonstrate resilience. Alongside moderating inflation, this increases the probability of an economic soft landing. But we think a mild recession is just about more likely than not.

By contrast, the Eurozone and UK economies are at risk of imminent downturns. Developed market central banks still have work to do taming inflation pressures, but 2024 should see the start of easing cycles.

Meanwhile, Chinese growth will continue to face headwinds, but the policy response there is ramping up and should prevent a hard landing for the country’s economy.

Emerging markets elsewhere are benefiting from moderating inflation and will soon enter a cycle of monetary-policy easing.

US – Close to peak rates

The US economy remains remarkably resilient, with the pace of growth seemingly accelerating over the summer months in the northern hemisphere. Robust consumer and business balance sheets and a strong labour market can extend this expansion into 2024.

Moreover, headline and core inflation have slowed significantly, with further disinflationary pressures on the way from weaker goods and shelter prices, even if more recent energy-price developments may slow this dynamic.

That said, in our baseline forecasts, we still expect a US recession beginning around the middle of next year. The moderation in inflation is flattered by methodology issues and volatile components used in calculations.

With wage growth still elevated, a more pronounced slowing in the labour market is still probably necessary to fully restore price stability. Moreover, bank credit conditions have tightened to levels consistent with a recessionary catalyst, industrial surveys point to weaker activity and labour demand is slowing.

All this reflects a growing drag effect from earlier Federal Reserve (Fed) tightening, which will continue to grow, especially as household-savings buffers erode.

In the near term, a combination of strong activity data and soft inflation should allow the Fed to leave rates on hold in September. There’s a good chance of a final rate hike in November given the strength of economic activity and the Fed’s desire to avoid putting at risk the progress made on inflation.

But the bigger picture is that the hiking cycle is ending and there will be a pause in higher rates for a while. However, we think the Fed will start cutting interest rates from mid-2024, potentially to as low as 2% by 2025 – a level below the neutral rate.

Beyond the baseline scenario, the combination of strong growth and a seemingly ‘immaculate disinflation’ this year has increased the chances of a US soft landing. This is the biggest upside risk to the global economy and would see interest rates remaining higher for longer.

Europe – Embracing recession

By contrast, the Eurozone economy is either very close to, or already in, recession. This is due to monetary policy tightening by the European Central Bank (ECB), an incomplete recovery from last year’s energy price shock, and the weak global industrial cycle that’s hurting European exporters.

Indeed, Germany’s energy-intensive, goods-exporting, China-orientated growth model is under an enormous amount of pressure, with recent industrial production data consistent with a significant economic contraction.

Both headline and core Eurozone inflation should continue to fall further as the economy cools and energy base effects remain favourable. We therefore think the ECB is done, or very close to done, raising rates. While the ECB, and indeed all developed market central banks, will signal an extended period of tight policy to keep a handle on financial conditions, we ultimately expect an easing cycle next year.

The UK economy is also facing mounting headwinds, as the Bank of England’s interest-rate hikes start to weigh heavily on activity. Economic growth seems to have slowed sharply over the northern-hemisphere summer, with the labour market starting to crack and house prices falling more rapidly. We anticipate the start of a recession later this year.

However, the UK’s unique series of negative supply-side shocks means that, even with growth weak, underlying inflation will remain stickier than elsewhere. After a final rate hike in September, we expect rates to be on hold for some time. However, by the middle of next year, progress on returning inflation to target and broader economic weakness should allow for a sustained easing cycle to begin, albeit a slower one than in other economies.

China – Only certainty is uncertainty

Chinese growth will continue to face headwinds from subdued consumer confidence, a contracting global industrial cycle and, most of all, a beleaguered real estate sector.

More substantial policy easing is now starting to come through, including real-estate stimulus, and additional easing is likely. In our baseline scenario, this stimulus prevents a hard landing, with growth only slightly below target in 2023, weakening further in 2024.

However, there are substantial upside and downside risks in China, with both a huge stimulus boost and a much more severe balance-sheet recession possible. Overall, we think the balance of probabilities is skewed negatively.

EMs – At the vanguard of easing

Across other emerging market (EM) economies, the cautious monetary easing begun by a handful of EM central banks is likely to broaden out during 2024.

Admittedly, concerns around foreign exchange pressures, the Fed’s policy path, commodity-price uncertainties and still high inflation expectations in some economies, will keep many EM central banks on the sidelines for now. But those markets offering higher real yields are already starting to ease substantially.

Latin America is at the forefront of this turn in policy, with Brazil and Chile already cutting interest rates by more than expected. We expect central banks in that region to continue cutting rates amid moderating inflation and some growth weakness.

Interest rates across Asia Pacific will largely be on hold for now, as central banks there observe the effects of earlier policy tightening but also remain alert to the risks of higher food prices from El Niño effects, before cutting more next year.

In central and eastern Europe, ingrained underlying inflation pressures will create the largest challenge to a sustained cutting cycle by central banks there.

abrdn's Research Institute produces original research at the intersection of economics, policy and markets.

ii is an abrdn business.

abrdn is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.