MS International: Can the rebound last?

10th August 2018 15:32

by Richard Beddard from interactive investor

After four years of indifferent profitability, MS International surged in the year to April. Companies analyst Richard Beddard asks what's next for its disparate businesses.

To set this year's results from MS International into their historical context, I'm going to start not with revenue or profit growth, but with the profit margins of its four divisions. That’s because MSI is a conglomerate and to really understand its performance, we’ve got to get under its skin.

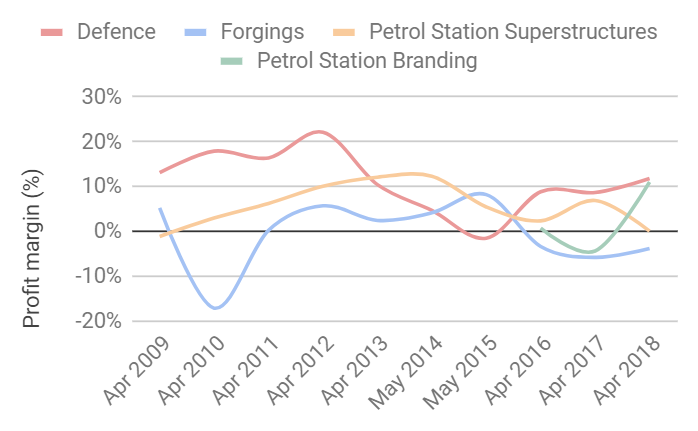

One chart to rule them all

Source: interactive investor

MS International's divisions manufacture, in the main, naval cannon ("Defence"), fork-arms for forklift trucks ("Forgings"), petrol station canopies ("Petrol Station Superstructures"), and, following the acquisition of Petrol Sign a couple of years ago, petrol station signage ("Petrol Station Branding"). Although the two petrol station businesses supply similar customers, the four divisions have little else in common.

Forgings is currently losing money, and it lost money in 2010 too. The newly acquired Petrol Station Branding business lost money last year, and MSI Defence lost money in 2015. Together, though, they are stronger because they are so different. That is probably why MSI collected them...

Scoring MSI

As usual I’m scoring MSI to determine whether it is profitable, adaptable, resilient, equitable, and cheap. Each criterion can achieve a maximum score of 2, and a minimum score of zero except the last one. The lowest score for companies trading at very high valuations is -2.

Profitable: Does it make good money?

Score: 1

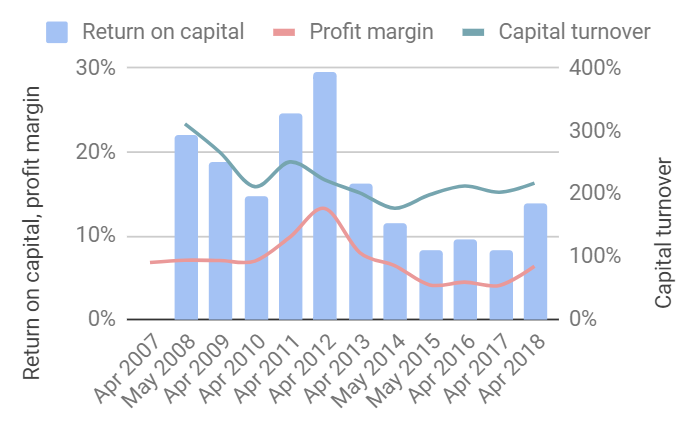

In 2011, when MS's biggest division, defence, was performing extremely well and its other two divisions at the time were performing adequately, the group as a whole was humming along. After-tax return on capital was 30% and after-tax profit margins were more than 10%.

Source: interactive investor

Even during the lean years from 2014 to 2017 return on capital didn’t fall below 8%, my rough and ready minimum for a decent business, although profit margins narrowed to 4%.

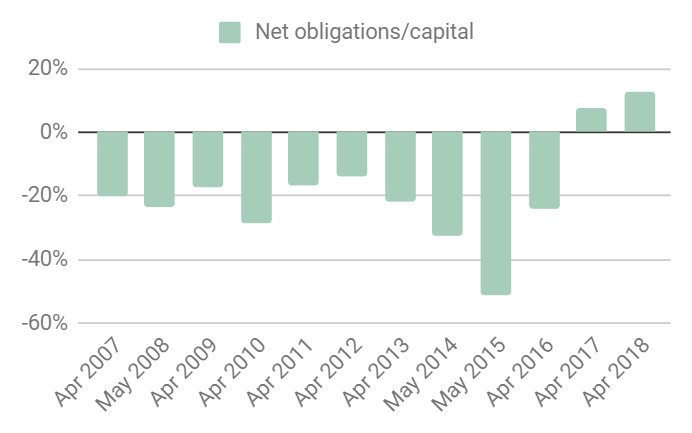

Today, return on capital is 14%, just below its long-term average, although the firm’s financial position has deteriorated slightly. For most of its recent history, MS International has run a cash surplus but it is now reliant on a small amount of external capital, probably due to increased lease obligations after the acquisition of Petrol Sign and the construction of a new Forgings factory in the United States.

Source: interactive investor

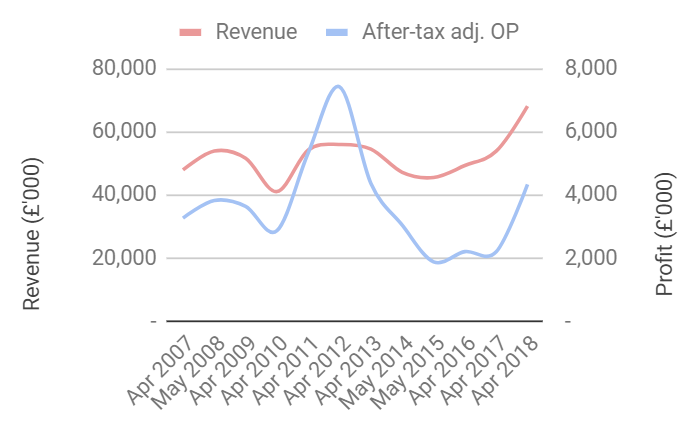

The upshot is, by the skin of its teeth, MS International has grown over the last decade, thanks to a sharp rise in revenue and a doubling of profit in 2018.

Source: interactive investor

The difference between this year and last year, was a dramatic improvement in the petrol station branding division. Revenue increased from £6.6 million to £19.6 million, almost as much as MSI Defence earned, and profit increased from a small loss in 2017 to over £2 million.

Adaptable: How will it make more money?

Score: 1

MSI claims two fundamental strengths: a policy of reviewing its capabilities and adapting them to changing market circumstances, and the diversity of its businesses.

Although each business experiences periods of low demand, the contributions of other business performing better reduces the strain on the conglomerate's finances.

In 2018, profitability improved in Defence as overseas customers responded to numerous new and unspecified product offerings developed in recent years. A constrained defence budget in the UK means the local market "lacks any reasonable element of clarity" though.

Forgings is only loss making because of the cost of building a new manufacturing facility in the USA (in addition to factories in the UK and Brazil). Excluding those costs it is breaking even, probably because many of its customers are miners, and low commodity prices have reduced investment generally.

MSI says it has a total commitment to efficient production, quality, and customer service, but whatever it does, the level of profitability it achieves depends on vacillating fortunes of its customers.

MSI is supplying fewer petrol station canopies and car washes because its customers, big oil companies, are selling their petrol stations to independent retailers, which means refurbishment and expansions plans are "in limbo".

Meanwhile, the forces depressing sales of petrol station superstructures have turbocharged sales in petrol station branding. When a petrol station changes owner, the fuel supplier may also change, which requires immediate rebranding.

It is difficult to determine what the company does particularly well, because the results of its various divisions are so inconsistent and it reveals little detail about their individual strategies.

In general, MSI says encouraging things about heavy investment in kit, product development, and people, owning "unquestionably" intellectual property rights to the products it develops, and relentlessly improving customer service. An average return on capital of 16% over the last 11 years suggests these efforts have borne fruit.

Resilient: What could go wrong?

Score: 0

Normally the principal risks section of a company's annual report is a dense table spanning a number of pages. MSI though confines itself to two principal risks.

It acknowledges customer demand fluctuates, which it seeks to minimise by doing a good job and flexing prices, and it says:

"The referendum on the UK’s membership of the EU increases economic and operational uncertainty."

Because defence budgets and commodity prices, the principal external drivers of profitability for MSI's defence and forgings businesses, are not correlated with each other or, necessarily, the wider economy, MSI's diversity has helped it weather difficult times.

Brexit could impact British manufacturers adversely in at least three ways, by weakening the UK economy, by worsening the terms of trade with EU members, and by worsening the terms of trade with non EU members that the EU currently has trade agreements with.

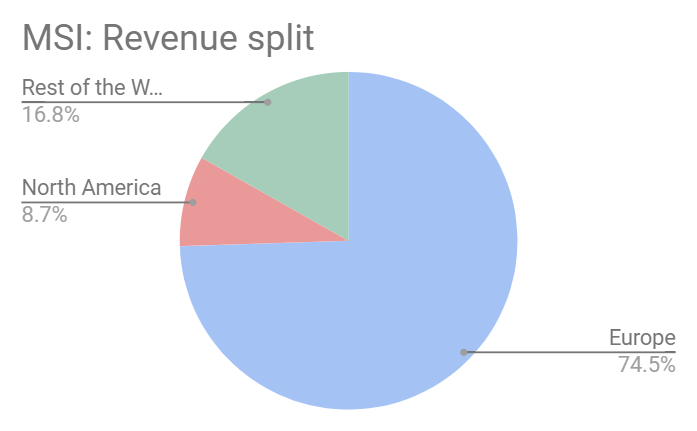

Companies with substantial dealings directly with EU countries are probably at most risk, MSI is in this bracket since 75% of revenue is from European customers, but it is not possible to tell the extent of exports to Europe as MSI does not divulge the UK component of European sales.

Source: interactive investor

I think there are also risks facing the petrol station businesses. The new independent owners of petrol stations will one day need to refurbish or add to their forecourts but MSI may find it more difficult winning business since the customers it knows best, the oil companies, are retreating, and the companies it must deal with, the independents, are new, and some of them are small.

The number of petrol stations has also been diminishing for decades as supermarkets have taken market share, encouraging people to drive further for cheaper fuel. It seems destined to fall even further as we wean ourselves off fossil fuels.

There's another risk, lurking in the notes. Nearly £15 million, 75%, of the revenue earned by the Petrol Station Branding business, the business largely responsible for this year’s turnaround, came from just one undisclosed customer.

Equitable: Will we all benefit?

Score: 1

The company says little about its culture, and I am not a fan of its remuneration policy. Basic salaries are high, and bonuses in the past have been excessive when the company has performed well.

The directors have a controlling interest in the company, which can be a good and a bad thing.

Cheap: Is the firm’s valuation modest?

Score: 2

The shares trade on a very modest valuation: about ten times adjusted profit.

Verdict: The future is unknowable

To return to my initial question, I don’t know what MS International's disparate businesses will do next. We can never know the future for sure, but MSI's future seems more than usually unknowable. That’s partly because the future of petrol stations is questionable. And it is partly because all of its businesses are highly susceptible to outside forces.

I wonder whether the forgings business is much of an asset at all. Even when it is profitable, margins are often pretty thin.

A score of 5/10 means that despite the low valuation and the potential for MSI's underperforming businesses to come good, I am not confident enough to recommend MS International to long-term investors.

Contact Richard Beddard by email: richard@beddard.net or on Twitter:@RichardBeddard

Richard owns shares in MS International.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.