The rates reset…where next for UK investors?

UK advisers and wealth managers are seeking alternatives to cash and liquidity holdings.

29th August 2025 09:03

by Adam Dmochowski from Aberdeen

Since 2022, global interest rates have been high. This has facilitated flows to cash and liquidity funds.

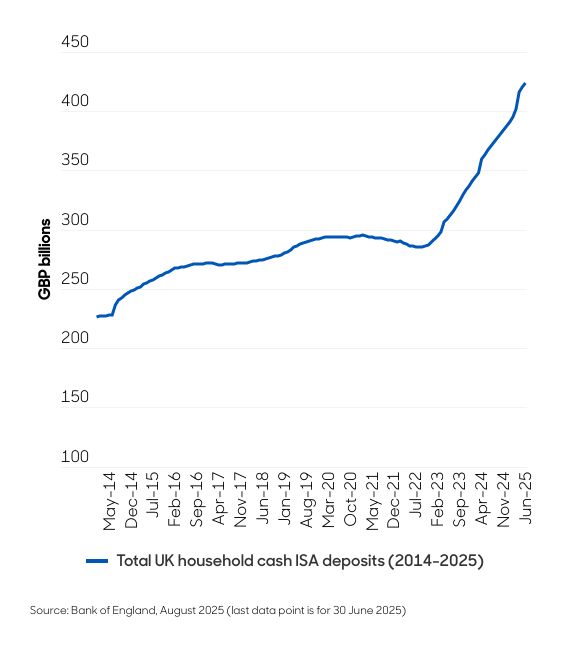

In fact, over the last two years, cash and liquidity funds as a portion of investor allocations for advisers and wealth managers in the UK has grown by a notable 44% [1]. As shown below, the increasing allocation to cash is also evidenced by the pronounced growth of cash ISA holdings in recent years.

Chart 1: Total UK household cash ISA deposits (2014-2025)

However, UK interest rates are now on a clear downward path, with the current 4% level being the lowest since March 2023. At Aberdeen, our team of economists are forecasting another 0.25% cut this year, with a further 1% of cuts in 2026, which would leave the Bank Rate at 2.75% [2].

What’s the impact on UK investors?

With inflation expected to stay above 3.0% for this year, this poses a problem for advisers and their clients. What to do with cash allocations as rates come down? As we know, falling rates erode the real income clients can generate from cash, which can be particularly problematic for retirees in the decumulation phase who rely on regular withdrawals.

This is especially relevant to the UK where the retirement market is significant. Defined contribution (DC) assets have grown by almost 30% since 2019, with the DC market estimated at £1.9 trillion and £220 billion in drawdown at the end of 2023 [3]. With the FCA increasingly focusing on firms demonstrating how their retirement income strategies can meet their clients’ needs [4], we think now could be an opportune time for advisers to review the options available.

Financial Adviser Retirement Investment Strategies

| Approach / Investment Strategy | Definition |

| Annuity | Insurance contract that pays out a guaranteed income for life or for a fixed period. |

| Blended / Hybrid annuity | A blended approach where a portion of a pension is used to purchase an annuity and the remainder balance remains invested. |

| Bucket approach | Splitting an investment portfolio into buckets (~2-3) and drawing income from the cash / short-term pot, and then replenishing this from other buckets. |

| Natural yield | Meeting income requirements from the natural yield on investments thereby not selling capital down. |

| Proportional withdrawal | Generating an income by selling a proportion of each investment across the model or selling units in a fund to generate income. |

| Smoothed funds | Funds designed to smooth the market volatility and target long-term steady growth. |

| Bespoke | Individual approach to managing portfolios and to deriving income. |

As show above, advisers have multiple retirement strategies available to them. Firms deploying strategies such as ‘Natural yield’, ‘Smoothed funds’, ‘Bespoke’ or the ‘Bucket approach’, may wish to read on…

A viable alternative asset class

For advisers, declining rates create a need to find low-volatility, income-generating solutions that can reliably preserve capital while delivering a sustainable yield. We think an asset class that looks well-suited in this respect is investment-grade short-dated credit. In particular, we think it offers the best balance in terms of yield enhancement above cash and stability, which is facilitated by the key features of low credit risk and low duration.

With regards to stability, as shown below, it is worth noting that the BofA 1-3 Year Global Corporate Index recorded just one negative total return over the last 28 calendar years. The year 2022 was one of historic negative returns across fixed income; however, even then, short-dated credit still convincingly outperformed all maturity indices, such as the Bloomberg Global Aggregate - Corporates Index, which was down over 14% [5].

Chart 2: Global corporate short-dated index annual total returns (1997-2024)

Introducing our Short Dated Enhanced Income strategy

In response to client demand, we have designed a strategy within the short-dated credit space that is expressly intended to be an all-weather type of ‘step out of cash’ solution. Our active abrdn Short Dated Enhanced Income (SDEI) strategy aims to provide an attractive yield and a total return of +1.75% above cash, over the long term, while limiting volatility and drawdowns.

Crucially, the strategy's portfolio of global short-dated corporate bonds offers quick access for investors with T+1 settlement. Stability is ensured by only investing in high-quality securities that result in at least an average portfolio credit rating of A-, and duration of less than 2 years. In addition to this, we believe the strategy offers three key differentiating factors that should appeal to advisers:

1) A clear outcome focus: The strategy has been specifically designed to deliver the outcome of yield enhancement over cash, coupled with low volatility and minimal drawdowns. This differs from traditional short-dated credit funds, which are more typically constrained by being managed relative to benchmarks.

2) A blend of money market features and short-dated credit: The strategy will always have a significant allocation to bonds maturing within one year — currently around 35%. Currently, we believe this segment offers some of the best risk-adjusted yields. However, this portion, which behaves more like money market assets and exhibits extremely low volatility, is not included in traditional short-dated benchmarks.

3) A genuinely global and diversified approach: Most money market funds today tend to be limited by region-specificity (e.g. sterling or euro). However, the SDEI strategy has a genuinely global remit for which it leverages Aberdeen’s global research platform to construct a portfolio of high-quality assets with attractive yields.

Financial Clarity, IA Sector Class: Cash and Liquidity June 2025

Aberdeen Global Macro Research team forecasts, August 2025

Investment Management in the UK 2023-2024: The Investment Association Annual Survey

Alpha FMC, Decumulation – it requires a different approach, Independent Report commissioned by Charles Stanley, 2025, p.24

Bloomberg, August 2025

Adam Dmochowski is a senior investment specialist at Aberdeen.

ii is an Aberdeen business.

Aberdeen is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.