Trading Strategies: the outlook for BP shares

Is a top-down or bottom-up approach best for equity investing? Analyst Robert Stephens combines them both, explaining major changes to the outlook for equities and studying the financial position of this popular FTSE 100 company.

27th November 2023 10:29

by Robert Stephens from interactive investor

Stock market investors are generally more interested in the future than the past. Therefore, share prices often rise in anticipation of an economic boom and fall before the very worst of a recession is felt by businesses and consumers. Indeed, it is not unheard of for a bull market to be in full swing while economic data remains dire.

Investors are currently looking ahead to the potential for improved GDP growth following a continued fall in the annual inflation rate. It declined from 6.7% in September to 4.6% in October, and is now materially lower than the 41-year high of 11.1% posted 12 months earlier. While it still stands at more than twice the Bank of England’s 2% target, investors are already beginning to anticipate that falling inflation will allow interest rate cuts to be implemented in response to the UK’s ongoing weak GDP growth rate.

- Invest with ii: Top UK Shares | Share Tips & Ideas | Open a Trading Account

In fact, the UK economy produced zero growth in the third quarter, according to preliminary estimates by the Office for National Statistics (ONS). With the full impact of previous interest rate rises yet to be felt due to the existence of time lags, it seems likely that monetary policy will need to become substantially more accommodative as inflation falls. Otherwise, a much-anticipated recession may come to fruition.

Short-term uncertainty

Similarly, interest rate cuts are being mooted in the US, with the Federal Funds Rate forecast to fall from its current level of 5.25-5.5% to 2.9% over the next three years. The US annual inflation rate of 3.2% is even closer to the central bank’s 2% target than it is in the UK, which suggests the Federal Reserve has scope to slash interest rates over the coming months.

However, with the US unemployment rate being relatively low by historical standards, and the US economy growing at an annualised rate of 4.9% in the third quarter, policymakers appear to have less incentive to cut rates than their UK counterparts. The prospect of an overheating US economy may, in fact, encourage them to maintain a hawkish monetary policy for longer than stock market investors are currently anticipating.

As such, the near-term prospects for US and global equities remain highly uncertain. Although the S&P 500 and the FTSE All-Share Index have risen by 11% and 4%, respectively, over the past month as investors have become increasingly optimistic about the potential for interest rate cuts, volatility could remain elevated.

The Vix volatility index, also known as Wall Street’s “fear gauge”, has returned to its pre-pandemic levels after spiking during September and October, thereby suggesting increased optimism among investors. But it could easily surge higher if inflation proves to be stickier than stock market investors presently anticipate. After all, this would be highly likely to cause a delay in the implementation of interest rate cuts and could prompt a more subdued economic outlook.

Long-term return potential

While the timing of lower inflation and a more accommodative monetary policy remains uncertain, the stock market continues to offer a highly favourable long-term outlook.

Ultimately, interest rate rises are set to end and be replaced by monetary policy easing as inflation falls towards its 2% target. Productivity issues and demographic changes across the developed world mean pre-pandemic interest rates could even be on the long-term horizon. Looser monetary policy is extremely likely to have a more positive impact on equities than other assets, notably fixed income, due to the capacity for interest rate cuts to catalyse earnings growth, dividend rises and investor risk appetite.

Exactly when equity markets will produce a sustained rise remains unclear. Moreover, the path to lower inflation and monetary policy easing is likely to be anything but smooth. Fortunately, the low share prices of a relatively large number of listed companies fully compensate investors for the prospect of heightened near-term volatility. As a result, they offer stunning long-term capital growth potential that can be accessed by any investor willing to accept a period of amplified uncertainty over the short run.

A fundamentally sound business

Company | Price | Market cap (m) | Shares in 2023 (%) | Shares in 2022 (%) | One-year performance (%) | Current dividend yield (%) | Forward dividend yield (%) | Forward PE |

BP | 472.225p | £80,041 | -0.56 | 43.7 | -3.30 | 4.2 | 4.7 | 7.1 |

Shell | 2,562.75p | £168,437 | 10.2 | 43.4 | 8.27 | 3.3 | 3.9 | 7.8 |

Source SharePad. Data as at 27 November 2023.

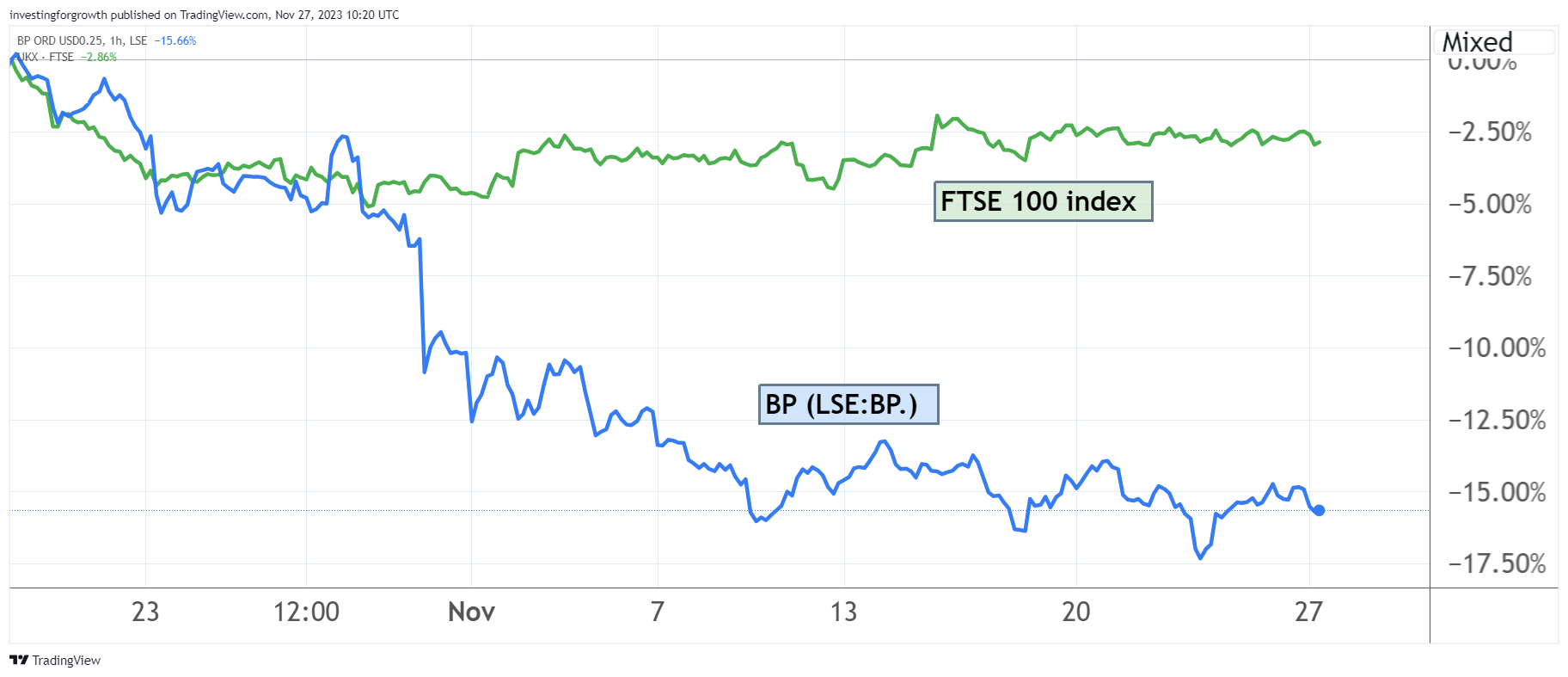

Shares in FTSE 100-listed oil and gas company BP (LSE:BP.) have fallen heavily over recent weeks. They now trade just 5% above their one-year low of 447p and have a prospective earnings multiple of 7.1.

Crucially, the firm is fundamentally sound. Its recently released third-quarter results showed that its net debt-to-equity ratio currently stands at 26%, while finance costs were covered nine times by operating profit in the first nine months of the year. This highlights its capacity to service what are relatively manageable debt levels even if oil and gas prices come under sustained pressure and negatively affect profitability.

- Stockwatch: what I’d do next with this successful share tip

- Mark Slater: the beaten-up UK growth shares we are buying

The company’s strong cash flow means that its planned share buybacks of $4 billion per annum are likely to prove highly affordable. They should help to support its share price during the current period of elevated global economic uncertainty. Its forecast capital expenditure of $16 billion in the current year highlights its capacity to invest heavily for long-term growth.

Dividends per share, meanwhile, are currently covered around 2.6 times by underlying earnings per share. This means they are highly affordable at current levels, which further enhances the stock’s income appeal while it trades on a dividend yield of 4.7%. Since inflation is set to decline, the company’s expected 4% annual rise in dividends is likely to equate to a positive real-terms increase for investors over the long run.

Source: TradingView. Past performance is not a guide to future performance.

Strategy shift

BP is in the midst of searching for a new CEO, with incumbent Murray Auchincloss currently acting in an interim capacity. Although it is impossible to determine what the firm’s long-term strategy will be until a new management team is in place, it would be wholly unsurprising for them to persist with the company’s recent trend of retracement from renewables in favour of oil and gas investment.

The firm was previously aiming to cut oil and gas production by 35% from 2019 levels by 2030, but reduced that figure to 20% earlier this year. Since fossil fuels currently offer higher return potential than renewables, and are still expected to represent 60% of the world’s energy mix by 2050 according to the International Energy Agency, a pivot to oil and gas assets would be likely to act as a positive catalyst on the firm’s financial performance.

- Outlook for oil prices and energy sector

- Insider: heavy buying at two FTSE 100 companies and this small-cap

Clearly, oil and gas prices are highly changeable and will have a direct impact on BP’s bottom line. In the short run, sluggish economic activity levels could weigh on their performance due to reduced demand. However, on a long-term view, they are likely to rise in tandem with an improving global economic outlook that is spurred on by the return of more modest levels of inflation and interest rate cuts.

A patient approach

Investors in BP, of course, must be willing to adopt a patient approach. While some investors may view the company’s recent share price decline as an opportunity to make a “quick buck”, in reality investor sentiment could worsen before it improves. After all, the company’s short-term performance is dependent on inflation and economic data, as well as the decisions made by central banks, which remain known unknowns.

But with a solid financial position, a strategy that is increasingly focused on delivering value for money, and a wide margin of safety, the firm has significant investment potential.

Robert Stephens is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.