UK real estate market outlook Q1 2024

UK inflation is set to fall further over the next few months and interest-rate cuts are expected around the summer.

23rd February 2024 09:16

by David Scott from Aberdeen

Key highlights

With inflation falling and likely to continue to do so, a rate-cutting cycle commencing in the second half of 2024 looks more likely.

Capital value declines have moderated and shown tentative signs of stabilisation for the most favoured sectors.

Anticipating interest rate cuts in 2024, there's an expected improvement in the performance of UK real estate, leading to a higher 3-year annualised average total return of 6.7%, with variations across sectors.

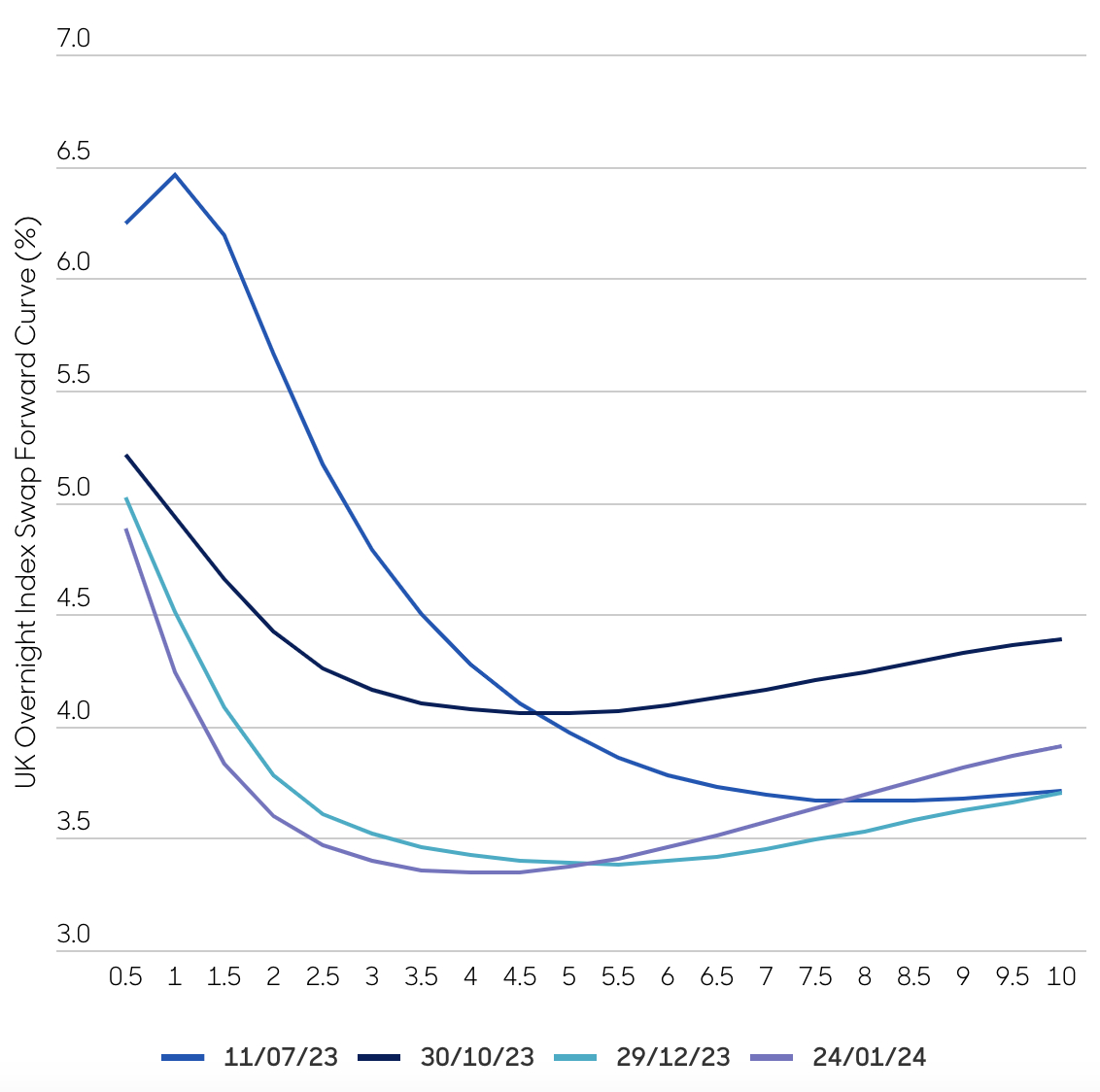

UK overnight index swap forward curve

Source: Bank of England, Bloomberg, abrdn January 2024. Forecasts are offered as opinion and are not reflective of potential performance. Forecasts are not guaranteed, and actual events or results may differ materially.

UK economic outlook

Activity

UK gross domestic product (GDP) growth rebounded in November, expanding 0.3% month-on-month, which was slightly better than the consensus of 0.2%. Services activity was the main contributor. The Office for National Statistics also noted that fewer strikes in November helped boost growth. Meanwhile, construction activity was weak, in part because of the weather. The monthly profile of GDP remains extremely volatile after a contraction of 0.3% in October. The broad trend remains one of sustained stagnation. Recession-like conditions look set to continue in 2024, but the prospect of further fiscal easing to be announced in March should help to limit the extent of the downturn.

Inflation

UK inflation unexpectedly ticked higher in December, with the headline consumer price index (CPI) rate increasing from 3.9% year-on-year to 4%. The consensus was for UK headline inflation to drop to 3.8% in December. The rise was largely driven by an increase in tobacco duty, while food prices were once again a drag on inflation. Underlying inflation pressures were also slightly stronger than expected. Core inflation was flat at 5.1% year-on-year. Inflation may move higher again in January, following a slight uptick in the Ofgem price cap. However, the bigger picture is that headline inflation is still set to fall further over the next few months. It could easily be below 2% by the second quarter of 2024, aided by favourable base effects. Meanwhile, cooling wage growth should also help bring underlying inflation pressure down.

Policy

At the Bank of England’s (BoE) December meeting, there was a concerted effort to push back against recent market pricing for an earlier rate-cutting cycle. Indeed, the policy communication and voting pattern suggest the BoE wants to keep alive the possibility of further rate hikes. This signalling is not surprising as the combination of elevated wage growth and modest fiscal stimulus means policymakers are particularly sensitive to an easing in financial conditions. However, a ‘Table Mountain’ profile for rates is unlikely to prove sustainable, as headwinds mount and underlying inflation pressures fade. We expect rate cuts to start in June.

UK economic outlook

| (%) | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|---|

| GDP | -11.0 | 7.60 | 4.10 | 0.40 | 0.00 | 1.50 |

| CPI | 0.90 | 2.60 | 9.10 | 7.30 | 2.70 | 2.20 |

| Policy Rate | 0.10 | 0.25 | 3.50 | 5.25 | 4.00 | 2.50 |

Source: abrdn December 2023. Forecasts are offered as opinion and are not reflective of potential performance. Forecasts are not guaranteed, and actual events or results may differ materially.

UK real estate market overview

While UK real estate capital values declined over the course of 2023, the pace of decline has moderated. There are tentative signs of stabilisation for some sectors but not all. There is a risk that further price discovery in the first half of 2024 will result in softer pricing, particularly for out-of-favour sectors. Performance has varied across sectors, with those benefiting from structural and thematic tailwinds proving more resilient in the face of a weaker macroeconomic environment. The logistics and living sectors are a clear example of this trend, both of which outperformed the wider market over the course of 2023.

UK real estate capital values fell by 2.6% in the fourth quarter of 2023. This resulted in value declines of 5.6% for the year, according to the MSCI Monthly Index. In line with our expectations, the living and logistics sectors outperformed the wider market, with capital value growth of 1.9% and 0.1% during 2023. The office sector remains the laggard. It recorded a capital decline of 16.6% over the same period, as the sector struggles with changing working habits, higher financing costs, and weak investor sentiment.

At the All-Property level, total returns for the calendar year 2023 were -0.1%. The largest negative contributor to performance was the office sector, which returned -11.9%. The residential sector was once again the strongest performing sector, returning 8.2%. The industrial sector returned 5.1% over the same period.

UK real estate investment volumes for the calendar year 2023 reached £34.3 billion, according to Real Capital Analytics. This represents a year-on-year decline of 47% and means that 2023 was the weakest year for investment activity since 2009. The investment market has been affected by a significant gap between buyer and seller aspirations across several sectors. The buyer pool for UK real estate was thin in 2023 and we expect this to be the case in the first half of 2024. While we expect greater liquidity to return to the market in 2024, this will be driven, in part, by buyer and seller expectations becoming more closely aligned.

The UK real estate listed sector ended the year on a high, with the FTSE EPRA Nareit UK Index posting a total return of 18.9% in the final quarter of 2023. It significantly outperformed the FTSE All-Share Index, which recorded a total return of 3.2% over the same period. The recovery in UK REIT (real estate investment trust) performance in the fourth quarter of 2023 was driven by the market pricing-in an increased probability of rate cuts in the second half of 2024. This is mainly because of better inflation data and the expectation that peak rates have been reached. This was clearly illustrated by the UK interest rate swap market, with the five-year swap reaching lows of around 3.3% by the year-end. This was considerably lower than the peak of around 5.3% that was reached in July 2023. The UK listed real estate index has historically led the UK direct real estate sector by six-to-nine months, which adds weight to the argument that the that the fortunes for the latter will improve over the course of 2024.

UK real estate market trends

Offices

Sentiment towards the office sector remains very weak, as the sector grapples with new working habits and a weaker economic backdrop. Investment volumes reached £8.5 billion in 2023, a 54% drop on 2022 levels. It was the weakest year for investment on record, according to Real Capital Analytics. Overseas investors were the most active source of capital for the sector over the course of 2023, followed closely by private investors. Institutional investors were the largest net sellers of office stock.

The most recent data indicates that vacancy rates across all major office sub-markets have started to plateau, but at elevated levels compared with historical averages. This is being driven by the availability of ‘grey’ or second-hand space, as occupiers rationalise their estates because of a fundamental shift in working habits. We’ve seen a consistent improvement in office occupancy rates across the UK in 2023. However, it’s unlikely this will translate into any meaningful improvement in the vacancy rate, as businesses become more selective about the quality of office stock they want to occupy.

The availability of truly ‘best-in-class; office accommodation remains in short supply. This is creating a two-tier market, which is helping to support prices and rents for prime office assets. We expect headline rents for ‘best-in-class’ office space to move higher from here, as a lack of suitable product and continued strong demand place further upward pressure on rents. Any office stock that falls outside this definition will see further pressure on rents and yields.

Industrial and logistics

The fundamentals for the industrial and logistics sector remain well placed to support the UK occupational market. While the vacancy rate continues to edge up – reaching approximately 4% at the end of 2023, according to CoStar data – it remains below the historical average of 5%. The same can be said for the availability of second-hand space. Construction starts have slowed materially, driven by more punitive financing costs, higher construction costs, and a lack of suitable sites. This is supporting rental value growth for the sector.

Over the course of 2023, industrial and logistics yields remained largely flat following a steep correction in the second half of 2022. Investor sentiment towards the sector remains positive, but there’s a clear polarisation in demand for ‘best-in-class’ ESG (environmental, social and governance) stock. Demand for shorter-let stock also remains strong, with investors eager to acquire assets that allow them to capture any potential rental reversion.

We remain positive on the longer-term outlook for the industrial and logistics sector, supported by structural and thematic growth drivers. Online retailing now accounts for approximately 30% of total UK retail sales. This is lower than the peak reached during the pandemic, but considerably higher than pre-pandemic levels. Additionally, shortening supply chains, onshoring, and a shift from just-in-time to just-in-case facility requirements, will help support tenant demand.

Retail

The retail sector faced a challenging year in 2023, with consumer confidence creating a significant headwind for the sector. Month-on-month retail sales volumes fell by 3.2% in December 2023, according to the Office for National Statistics (ONS). Retail sales were down 2.4% compared with December 2022. Black Friday tempted some consumers to bring forward their spending to November, which partly explains the slowdown in December’s retail sales. This is supported by the ONS’s public opinion and social trends analysis. It reported that 46% of adults had or were planning to spend less on Christmas food or presents, with 39% buying food or presents earlier to spread the cost.

The retail warehouse sector continues to garner strong investor interest. The vacancy rate for retail warehouses remains markedly lower than shopping centres or high street shops in the UK. Additionally, footfall has been more resilient than other areas of the retail sector, particularly for schemes with a more discount-oriented line-up. Occupationally, the supermarket sector remains well placed. UK operators experienced their busiest Christmas since before the pandemic, according to Kantar. Polarisation by operator remains a key theme for the sector, with Lidl and Aldi continuing to win market share from the big four supermarkets.

Real wages are now positive, driven by a fall in inflation, which has the potential to provide some support for the sector. However, we don’t expect this to materially alter the fortunes for the sector this year, given the number of mortgages that are due to be refinanced and the ongoing cost-of-living pressures

Living

The living sector is benefiting from structural and demographic growth drivers. This is clearly illustrated in the build-to-rent (BtR) sector, where a significant supply-and-demand imbalance is supporting robust levels of rental value growth across the UK. Prime yields for BtR in London and regional cities moved out marginally in December, according to CBRE, but this is largely being offset by rental value growth. Rents in the UK increased by approximately 9% in the 12 months to November 2023 and 20% over two years. We believe rental growth will remain positive for the sector, but it will moderate from record highs given affordability constraints in some markets.

Transaction volumes for the BtR sector reached £4.3 billion in 2023, surpassing 2022 levels by 10%, according to CBRE. Single-family housing, a large growth area for the BtR sector in the UK, accounted for close to half of all investment volumes for the sector over the course of 2023. Housebuilders are adapting their business models to include single-family housing in their pipeline. This should increase sales volumes, given a slowdown in the wider residential-for-sale market.

The living sector outperformed the wider market over the course of 2023, and it’s forecast to return positive performance over the course of 2024. This will largely be driven by continued positive rental value growth and a stabilisation in yields.

Outlook for risk and performance

Monetary policy and the wider macroeconomic backdrop were in the driving seat in 2023 and we believe this will continue in 2024. Towards the end of 2023, market expectations for interest-rate cuts picked up pace (see chart 1), as underlying inflation pressures eased. Softer economic data added weight to the argument that the BoE’s ‘Table Mountain’ profile was unsustainable. Despite the outlook for monetary policy becoming more positive from this point, an improvement in UK real estate performance is not expected until the second half of 2024. The abrdn Global Macro Research team expects the BoE to begin its rate-cutting cycle at this point.

While the macro environment will continue to dominate as we move through 2024, sector allocation will remain crucial. Polarisation in performance from both a sector- and asset-quality perspective will remain a key differentiator for performance. Real estate refinancing poses a risk to our outlook in 2024. But we believe the risk is more heavily skewed towards offices, given the amount of outstanding debt and lack of appetite for lending in the sector.

A UK general election is mandated to occur no later than 28 January 2025. Ultimately, the prime minister decides on the date of the election, but a date in November 2024 looks most likely at this stage. The Labour party has opened-up a 20-point lead in the polls, relative to the Conservative party. At this stage, it appears likely there will be a change of government in the UK over the next 12 months.

With the increased prospect of interest-rate cuts in 2024, we expect an improvement in UK real estate performance as we move through 2024. This will be driven primarily by improved investor confidence and greater market liquidity. The downside risk to our forecasts remains elevated, given weaker economic growth prospects and the potential uncertainty created by the upcoming UK election.

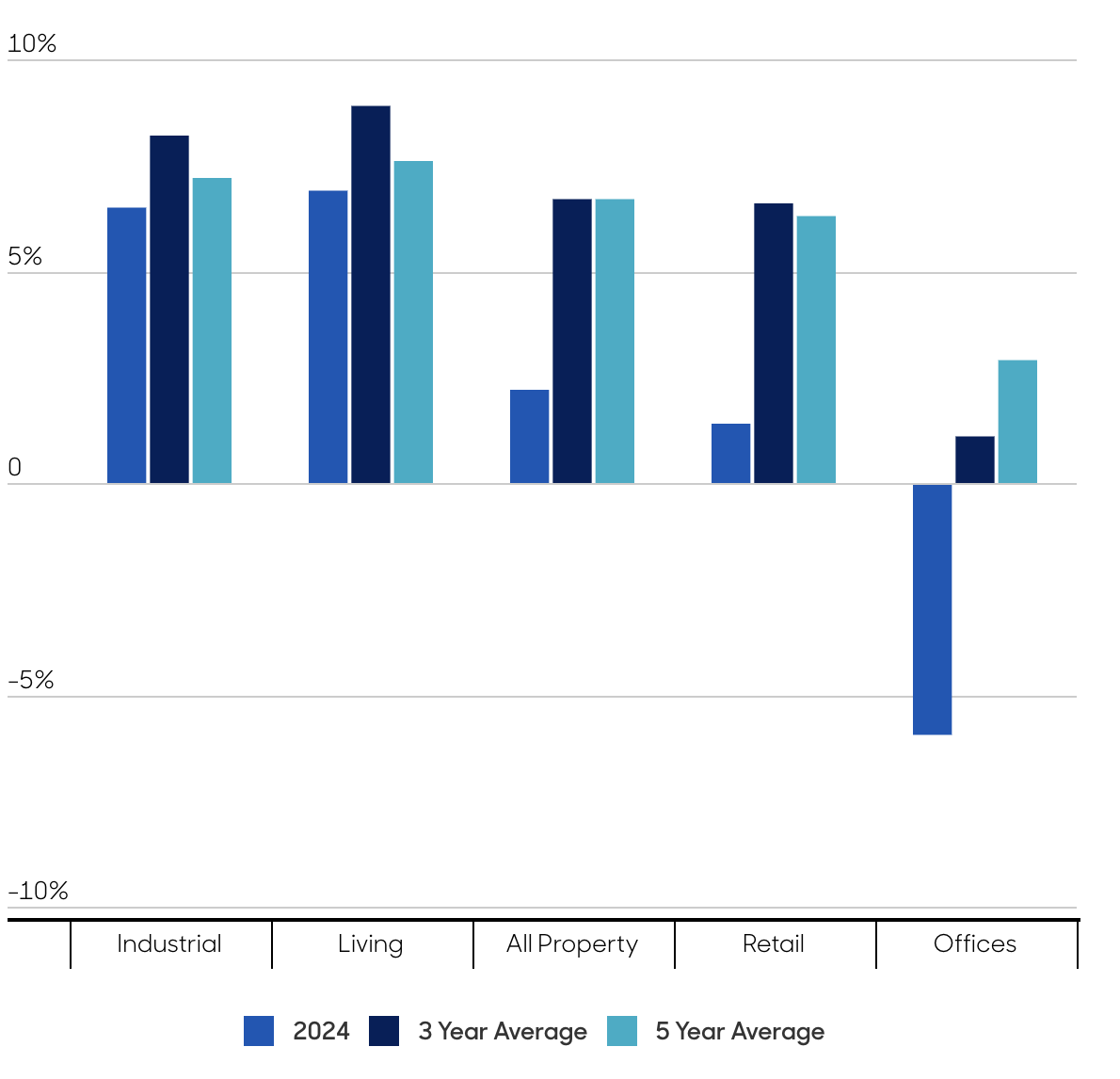

UK total return forecasts from January 2024

Source: abrdn, January 2024. Forecasts are offered as opinion and are not reflective of potential performance. Forecasts are not guaranteed, and actual events or results may differ materially.

David Scott is head of UK investment research, real estate, at abrdn.

ii is an abrdn business.

abrdn is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.