Why the ‘direction of travel’ bodes well for India’s economy

We consider why policy directionality and geopolitical trends bode well for India’s long term outlook.

4th September 2023 10:31

Key Highlights

Considering the directionality of key policies can help assess a country’s long-term economic outlook…

…India is ticking several boxes on this front, but we think the following policy areas will be especially important:

- competitive federalism

- increasing digitalisation

- the push for less carbon-intensive growth

Geopolitically, India looks well placed to benefit from the intensifying US-China rivalry, which will likely drive closer US-India alignment and cooperation in multiple spheres.

India can also look to capitalise on global companies’ increasing efforts to reduce supply-chain reliance on China.

The directionality of these key factors should help drive growth and create investment opportunities in India for the next decade and beyond.

A country’s long-term economic outlook depends on many diverse factors. However, arguably the single most important determinant is sound policymaking. In this respect, while perfection is impossible, what matters most is ensuring incremental progress by having the right direction of travel in as many key areas as possible. With this in mind, few would doubt that over the past decade or so India passes the overall directionality test.

We think a handful of standout policy factors will be pivotal to India’s growth outlook. These include the policy of competitive federalism, progress towards a comprehensive new digital eco-system, and the push for more renewable energy sources. While these are all domestic policy factors, external geopolitical trends are also looking increasingly favourable for India.

The importance of policymaking and policy directionality

According to standard economic theory, long-term economic growth boils down in large part to improvements in labour productivity. Other factors, such as labour availability and the labour participation rate, also matter. Nonetheless, as Paul Krugman noted, “productivity isn’t everything, but in the long run, it is almost everything.” When we drill down further into what drives productivity, three key factors emerge: physical capital, human capital, and technological change. Crucially, policymaking influences all these elements.

Theory aside, we believe good policymaking is the most important factor that elevates emerging economies to developed nation levels. Clearly, sound polices also need to be combined with good implementation, which in turn links to factors such as the rule of law, institutional strength and the quality of political leadership.

When it comes to policymaking, the list of areas for further improvement in India (such as labour and land reforms) is long. However, significant progress elsewhere means the overall direction of travel on policy is good. Among the oft-cited reforms are the easing of restrictions on foreign investment and stronger bankruptcy laws. The move to a new tax regime in 2017, which included the introduction of a Goods and Services Tax across all states, was also a success. This resulted in drastic tax simplification, effectively creating a ‘common market’ across all 36 union states. The policy greatly enhanced internal trade efficiency, supporting revenue growth and fiscal consolidation.

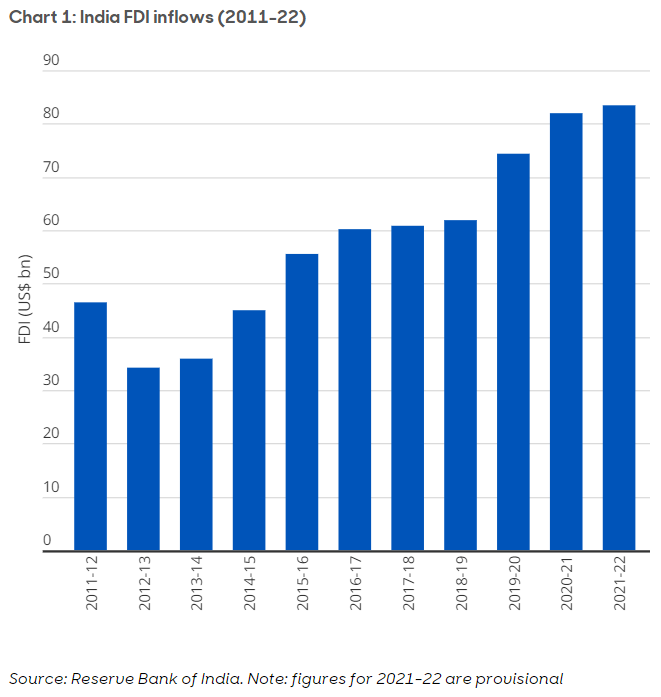

Such progress has certainly helped India’s business climate. Over the last decade, we’ve seen a rise in foreign direct investment (FDI) (Chart 1) and strong average real GDP growth.

The challenge for India will be ensuring the overall direction of travel remains positive in most key areas. In this respect, we think four factors could have a big impact…

Competitive federalism

An important driver of India’s ongoing development journey, and one which perhaps does not receive much credit, is the policy of state empowerment. Before 2014, Indian economic policymaking was largely promulgated through a centralised Planning Commission which, much like in China, would dictate 5-year national development plans. However, it was recognised that such a one-size-fits-all approach was ill-suited to a diverse country like India, with its distinct regional strengths and weaknesses and varying levels of economic development.

In 2015, Narendra Modi’s government replaced the old top-down model with a bottom-up approach. State governments were given much greater autonomy, backed by rising fiscal allocations. Importantly, individual states were given more license to compete with each other. This was a key stated objective of the National Institution for Transforming India (NITI Aayog), the apex public policy body which replaced the Planning Commission. Rather than dictating policies, NITI Aayog plays a facilitatory role, including encouraging best practice and assessing and ranking states across key development metrics.

The rationale of competitive federalism is an acknowledgement that individual states are best placed to make policies that are aligned locally. States competing stimulates efforts to improve local business conditions to attract investment and boost growth. At the same time, more focus on local competitive advantages reduces waste and improves resource allocation.

For competitive federalism to work, it’s essential that states are empowered over time. This is partly reflected in Indian states’ share of central revenues, which climbed from 32% in 2015/16 to 42% in 2021/22. That said, the policy of competitive federalism is still in its infancy, with significant potential for further autonomy and interstate competition in the coming years.

Digitalisation – driving efficiency and growth

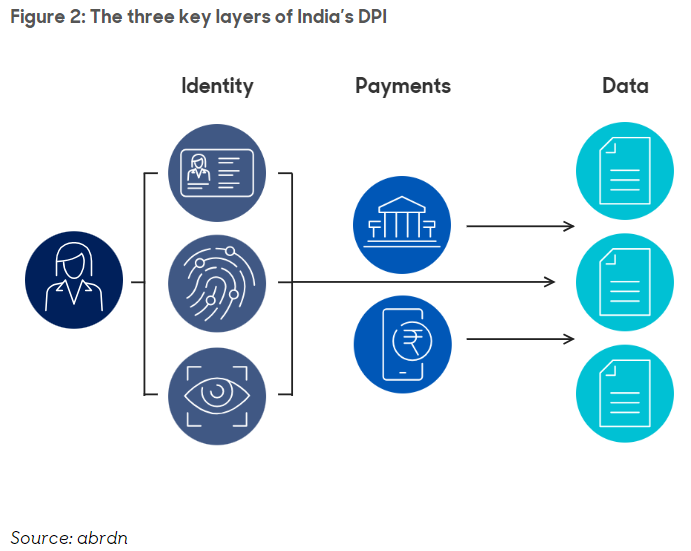

Arguably, India’s most fruitful policy over the past decade has been the ongoing drive to build a comprehensive new digital eco-system. Once known as ‘India stack’ and later rebranded as ‘Digital Public infrastructure’ (DPI), this refers to the collection of public-facing digital platforms that are having a major impact on many sectors of the economy.

India’s DPI is essentially based on the three ‘layers’: identity, payments and data management. The most critical foundational element is ‘Aadhaar’, a biometric digital identity system, that now covers virtually all of India’s 1.4 billion (bn) people. The data management layer, known as ‘Digilocker’, uses the unique 12-digit Aadhaar ID system to give citizens government-guaranteed secure online access to key documents, such as tax papers and vaccination certificates. The digital payments layer, called the ‘Unified Payments Interface’ (UPI), enables mobile payments.

In short, DPI allows citizens verify their ID, get key documents and make payments via personal phones easily and securely.

As with most forms of physical public infrastructure, the responsibility for the key building blocks of DPI lies with the government. This makes sense given public benefits, such as the efficient processing of direct social transfers and aiding the implementation of sustainable development objectives. The IMF estimates that shifting welfare benefits payments to Aadhaar-linked bank accounts cut losses from corruption by US$34bn, or over 1% of India’s GDP, between 2013 and 2021 (1).

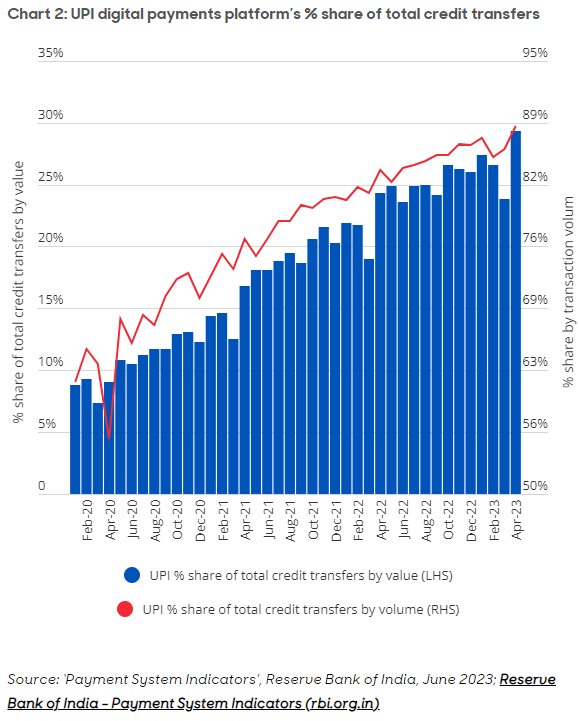

However, the benefits of India’s DPI extend beyond the public realm, driving areas such as ecommerce, banking and credit access, and innovation. A remarkable sign of this is how a country once renowned for the dominance of informal, cash transactions is rapidly embracing digital payments. Indeed, Chart 2 shows that in April 2023, in volume terms, the UPI platform accounted for 88% of all non-cash payments in India’s retail sector, up from 56% in April 2020. Likewise, the Aadhaar system is a stunning cost-benefit example in the private sector. It’s reduced ‘know your customer’ due diligence costs for banks from as high as INR700 to just INR3 per application, helping cut loan processing costs by almost 75% (2).

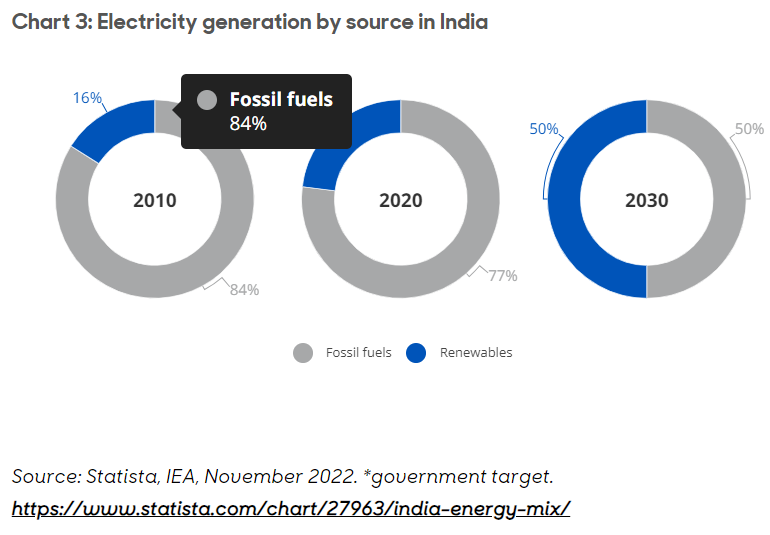

Energy transition – driving opportunity and growth

One of the Indian government’s top policy objectives is to pursue a cleaner and less carbon-intensive model of economic development. A notable target is ensuring 50% of electricity needs are generated from renewable energy sources by 2030 (see Chart 3). Numerous indicators suggest India is heading in the right direction in its energy-transition journey. For example, it recently claimed the global fourth spot in terms of installed renewable energy capacity (after China, the US and Germany). Still, India’s sheer size and room for growth imply a growing appetite for energy, as seen in the addition of 50 million new home electricity connections every year (on average) in the past decade.

The broad elements of India’s energy transition aspirations are clear. This includes pursuing increased electrification, greater penetration of cleaner fuels in the energy mix, accelerated adoption of energy-efficient technologies, and improved material efficiency. Of course, all of this will require huge investments at both the federal and state level, as well as from the private sector.

The International Energy Agency (IEA) estimates that India will need an annual average investment of US$160bn (around 4.7% of GDP) between now and 2030 alone if it’s to achieve its target of net zero emissions by 2070 – three times the level of recent years (3). The sizeable outlays India needs for its energy transition should be a major driver of both investment opportunities and economic growth for years to come.

Geopolitical tailwind

While policymaking is necessarily endogenous, other key directionality factors can be more exogenous. For India, this includes geopolitics. In particular, the intensifying rivalry between the world’s number one and number two economies, the US and China respectively. In this climate, India seems an ideal strategic ally for the US. After all, it’s the ‘world’s biggest democracy’ and fifth largest economy, with a huge land border with China.

As Prime Minister Narendra Modi’s high-profile state visit to the US in June 2023 illustrated, India’s partnership with the US appears to be moving into a higher gear. Indeed, in the effusive words of the new US-India Global and Strategic Partnership agreement, ‘no corner of human enterprise is untouched between the two great countries’. Among the notable areas of cooperation highlighted in the joint communique were technology and the transition to clean energy – both key growth drivers for India, where it can look to leverage the vast know-how, capital strength and direct patronage of the US.

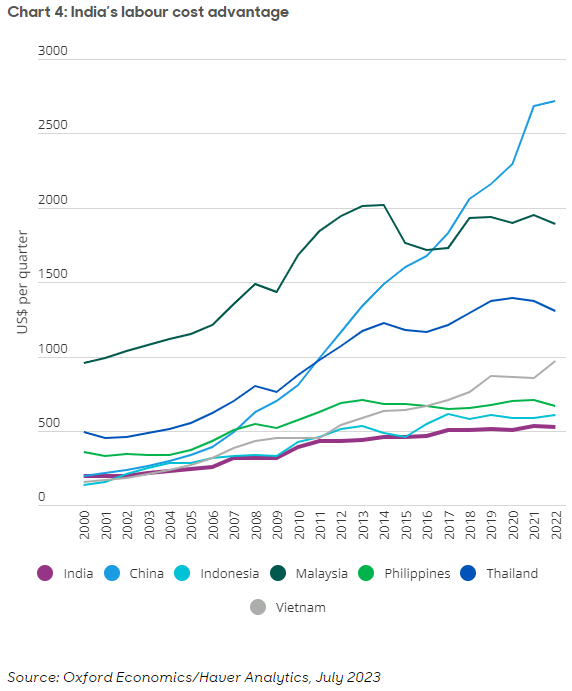

A major consequence of increasing US-China trade tensions has been global multinational companies seeking to lessen their supply chain reliance on China. This is an area where India, helped by its regional labour cost advantage (Chart 4), can look to fill the gap. Given a 260% surge in Indian electronics exports to the US between 2018-22, directionality on this front may already seem good. However, in reality, India's overall market share in US electronics imports remains tiny, at less than 1% (4). As such, amid increasing talk of ‘China-plus X’ strategies, there’s a real opportunity for India to harness geopolitical trends and local reforms to address its historic ‘weak link’ of manufacturing.

Investment implications

We think the directionality of key economic reforms, coupled with geopolitical trends, are highly supportive of India’s long-term growth and investment outlook. On the equities side, the push for clean energy means India is home to some of the world’s biggest renewable energy projects, helping the likes of Renew Power, the country’s largest ‘decarbonisation solutions company’, and Suzlon Energy, its biggest wind turbine producer. At the same time, the digital infrastructure revolution, combined with improving physical infrastructure (including internet connectivity), is fuelling a boom in ecommerce, helping companies such as online shopping giant Flipkart, the insurance company PolicyBazaar and the online recruitment company InfoEdge.

Policy directionality also supports the country’s ‘Make in India’ (MII) initiative, which seeks to encourage and incentivise companies to develop, manufacture and assemble products within India. As MII initiatives across 25 economic sectors develop, we expect to see a rise in investment opportunities, job creation and corporate earnings. It should also enhance India’s economic self-sufficiency.

On the bond side, the strengthening Indian economy and ongoing reforms have supported key credit fundamentals. These include tax intake relative to GDP and FX reserves, as well as enhanced local currency stability. The latter is important as it facilitates trade and capital flows. It also reduces the additional risk premium that global investors seek to compensate for currency risks. At the same time, India’s growing confidence in its ability to manage key risks is enabling a receptive environment for foreign investors. Indian bond markets are more accessible to foreign investors than ever before. A particularly important driver (and key reform in itself) of this was the launch of the ‘Fully Accessible Route’ (FAR) in 2020, which enabled foreign investors to buy designated government bond securities on a restriction-free basis (5).

The pool of index-eligible FAR securities is now approaching US$400bn, constituting over 30% of the government bond market. The overall market is over US$2 trillion and offers good liquidity. The argument for India’s inclusion into global bond indices is therefore strong. To better reflect the improved accessibility of the market, we also think an increased weighting in existing Asian local currency bond indices is overdue. Investors currently own less than 2% of the domestic bond market, which barely features in global portfolios. This suggests there’s plenty of room for allocations to grow in the years ahead. For investors, improved accessibility means the chance to enhance diversification and gain exposure to a relatively stable, high-yielding and large bond market of a major fast-growing country that has consistently outperformed for many years.

Putting everything together

When assessing the long-term outlook for any country, looking at the directionality of key policy factors can be useful. While this is necessarily a continuous process, with many areas for further improvement, India is ticking many boxes on this front. Highlights include the policy of ‘competitive federalism’, the expanding national digital eco-system, and efforts to secure India’s energy transition.

At the same time, India looks well placed to gain from the intensifying US-China rivalry. The country can also look to capitalise on global companies’ increasing efforts to reduce supply-chain reliance on China.

These factors should help drive investment opportunities and growth in India for decades. Most importantly, robust and sustained investment and growth should benefit the lives of India’s 1.4bn citizens, lifting millions more out of poverty.

- The Economist, June 2023. How India is using digital technology to project power (economist.com)

- https://www.thehindubusinessline.com/economy/aadhaar-brought-down-kyc-cost-to-3-from-as-high-as-700-says-nirmala-sitharaman/article66740192.ece, April 2023

- India’s clean energy transition is rapidly underway, benefiting the entire world – Analysis - IEA, January 2022

- 'India: How the “China plus X” strategy may benefit manufacturing’ – Oxford Economics, April 2023

- Following the launch of the Fully Accessible Route (FAR) in 2020, a growing number of Indian government bonds were designated as FAR securities, meaning they could be purchased by foreign investor without any of the previous quota restrictions. Before this, Foreign Portfolio Investors (FPIs) – i.e. those with foreign investor licences, still needed to get government or corporate bond quotas to be able to buy the respective bonds and these quotas also had various other restrictions associated with them (like maturity and exposure restrictions). Today however, once foreign investors have a FAR licence, they are free to buy FA-designated government bonds without any restrictions.

Ken Akintewe, Head of Asian Sovereign Debt - Fixed Income - Asia, and Ray Sharma-Ong, Investment Director.

ii is an abrdn business.

abrdn is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.