Anglo American: The cheapest large-cap mining stock in town

Its shares have soared recently, but Anglo still trades at a massive discount to London-listed peers.

2nd April 2019 12:41

by Graeme Evans from interactive investor

Its share price has soared recently, but Anglo still trades at a massive discount to London-listed peers.

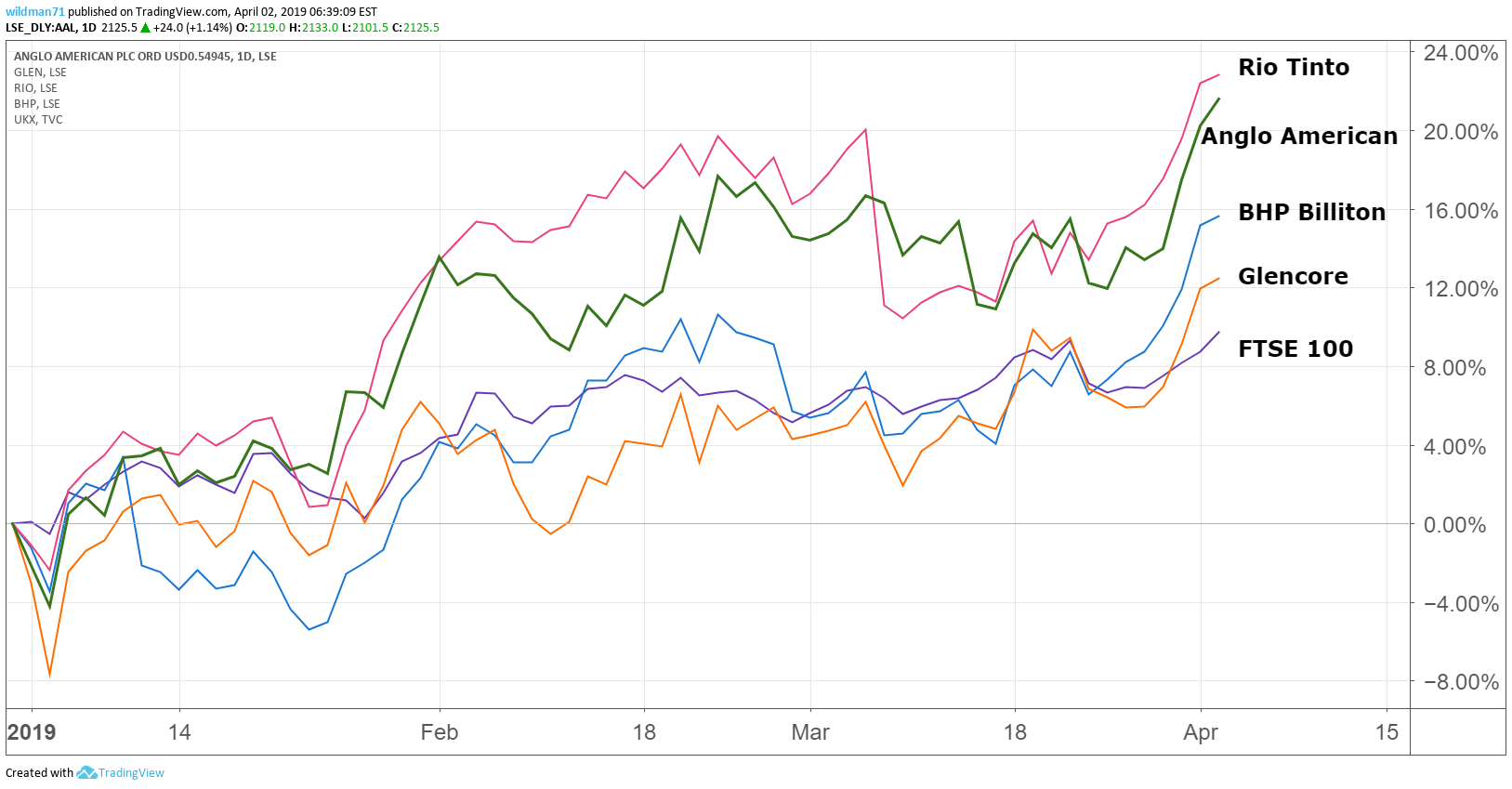

While Rio Tinto (LSE:RIO), BHP Group (LSE:BHP) and Glencore (LSE:GLEN) have grabbed the mining headlines with their recent bumper buy-backs and special dividends, Anglo American has so far resisted the temptation to splash the cash on behalf of shareholders.

Unsurprisingly, that's left the London and Johannesburg-listed miner as the cheapest among the sector's heavyweight stocks, trading at an average 25% discount to peers Rio and BHP. This underperformance is not unusual for Anglo over the past decade, with lower capital returns compounded by its higher exposure to emerging markets, particularly South Africa.

- Invest with ii: Top UK Shares | Share Tips & Ideas | Buy International Shares

However, a significant improvement in performance over the past three years has prompted two leading City firms to highlight Anglo's potential, even if the shares have already benefited from the mining sector's strong start to 2019 to reach a seven-year high at 2,100p.

Today, Deutsche Bank upgraded the stock to a 'buy' with a price target of 2,400p and a "blue-sky scenario" where the shares could reach 3,000p in the medium-term.

Source: TradingView Past performance is not a guide to future performance

The research comes a day after analysts at Jefferies valued Anglo at 2,500p and said that a buy-back may still be in the pipeline, possibly as soon as this August's interim results.

Jefferies said: "For investors looking for yield in mining, Anglo may not be the top of the list, but there are clearly other reasons to own Anglo shares for the long run, such as copper growth, valuation and break-up potential."

In light of bumper returns elsewhere, Anglo disappointed some investors in February when its dividend of US$0.51 a share stuck to a policy of paying a ratio of 40% of second half underlying earnings. The focus instead has been on growth projects and cutting debt, which fell 37% to $2.8 billion in 2018.

While Anglo's finance director Stephen Pearce has said he is open to considering buy-backs "at the right time", analysts at Deutsche Bank still think a total payout ratio of 60% is possible in 2019 and 2020, particularly given lower leverage levels and strong operating cash flows.

They add that Anglo has the "best and clearest growth strategy" of all the mining majors, with an enviable pipeline of opportunities in the copper division.

Deutsche said: "While all of the large caps are positioned to deliver strong cash flows in 2019 due to high iron ore and coal prices, Anglo has a wide range of value-accretive growth options to direct capital beyond shareholder returns."

By the end of 2022, Deutsche expects Anglo will be a business more exposed to mid-cycle commodities and less exposed to early-cycle iron ore and coal. They said: "As the company's cost of capital drops over time, we see a blue-sky de-risked scenario of £30 a share."

There are reasons to be cautious, however, with Jefferies noting risks including the impact of potential land reforms in South Africa and the ongoing correction in palladium and rhodium prices. The ramp-up of operations at the massive Minas Rio iron ore mine in Brazil is another uncertainty.

Liberum underlined the risks today by reiterating its 'sell’ rating at 1,200p.

However, Jefferies notes that if shares do not perform well, "a break-up of the company becomes a real possibility over the next two years, in which case the 34% upside to the sum of the total parts fair value becomes most relevant".

They described Anglo's distributions to shareholders as significant but nowhere near large enough on a yield basis to compete with Rio and BHP Billiton.

Following the sale of its US shales business, BHP Billiton recently returned $10.4 billion to shareholders through a buy-back and special dividend of $5.2 billion. Rio Tinto returned cash of $13.5 billion for 2018 through buy-backs and a special dividend following the sale of various assets, including the Grasberg copper mine in Indonesia.

And in February, Glencore announced a $2 billion buy-back for 2019 with the potential for up to $1 billion more based on non-core asset disposals.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.