This fast-growing "underdog" still yields 6%

29th May 2015 16:51

by Harriet Mann from interactive investor

Personal injury marketing firm has just celebrated its first year on AIM. And it's been quite a ride. The share price is up 50%, boosted by the acquisition of consumer legal marketing group Fitzalan, a cracking set of full-year results and expectations of sustainable double-digit profit growth. There's a knockout dividend yield, too.

Acting as the middle-man between personal injury claimants and a panel of 50 lawyers, enquiries from members of the public are the backbone to NAHL's success. Staff at the firm's call centre in Kettering dealt with 248,000 consumer contacts in 2014. Those were then whittled down to 83,000 enquiries suitable to pass onto its lawyers, up 15%. Of these, the company dealt with about 48,000 running cases.

And that stringent screening process is paying off, increasing the conversion rate of clean leads to enquiries to 75% last year, well above management's target of 70%.

Of the 1 million personal injury claims made in the UK each year, road traffic accidents (RTA) make up the bulk. But expansion in the once quieter areas of non-RTA and medical negligence is gathering pace, with market growth between 2011 and 2014 of 7% and 12%, respectively. NAHL's business model puts more emphasis on these typically higher-value claims, accounting for around three-quarters of enquiries. But with only a 4% share of the £3 billion personal injury market, NAHL has plenty of room to grow.

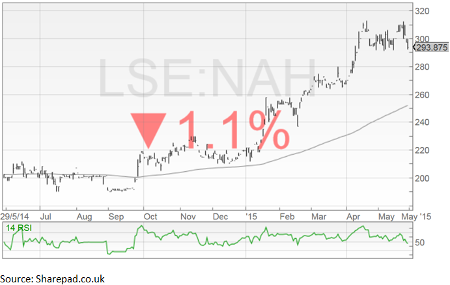

We expect the share price to settle nearer 350p over the course of 2015"Ben Thefaut, Arden Partners

Changes to the law in 2013 prohibited marketing companies from being paid by law firms for referrals. This has wiped out some of the market and forced NAHL to adapt - the panel law firms (PLFs) now pays a chunk of NAHL's outgoings, as well as an additional margin cost, accounting for 88% of revenue. Each member pays the billed amount within the month, making the group incredibly cash generative. Over 97% of operating profit was converted into cash last year.

This gives management the freedom to reward investors with generous dividends. Currently offering 6% dividend yield, management has promised to pay out two-thirds of retained earnings to shareholders.

(click to enlarge)

NAHL worked hard last year on new After the Event (ATE) insurance to fit in with new Legal Aid, Sentencing and Punishment of Offenders Act 2012 (LASPO) regulation. A medical negligence ATE was introduced in November and a new personal injury product will be launched next month. Along with new enhanced screening products and growth of rehab services, NAHL is focused on developing its product and brand.

After denouncing cold calling, management rely heavily on NAHL's brand image - the increasingly familiar Underdog character, created in 2010 for television and online marketing. The group has spent £23 million on day-time adverts and internet advertising last year, with 86% of claimants going online. And investment is paying off with a strengthened internet presence and 20 years of experience, which puts it ahead of smaller, lesser-known firms like InjuryLawyers4U, solicitors Irwin Mitchell and First4lawyers.

We believe the growth prospects remain very encouraging, both organically through increasing market share in the higher value areas of medical negligence and non-RTA and releasing the growth constraints of Fitzalan, as well as inorganically by acquiring in related areas"Investec Securities

Crucially, NAHL's balance sheet is strong enough to bankroll further acquisitions, too, supported by forecast year-end net cash of £1.4 million. The purchase of Fitzalan Partners underpins the City’s double-digit earnings forecasts and broadens NAHL's exposure.

This year has gone well, so far, and Arden Partners analyst Ben Thefaut has pencilled in sales growth of 12% to £49.2 million, driving adjusted pre-tax profit up by 14% to almost £13.9 million. Earnings growth of 29% last year is still a considerable 14.4% in 2015, according to Thefaut, then 10% in 2016. On these forecasts, NAHL trades on 11.2 times forward earnings, dropping to 10.1 times. That's undemanding, and there's a prospective yield of almost 6%.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.