Cash vs investing: stock market reigns supreme for getting rich slowly

31st May 2023 09:30

by Myron Jobson from interactive investor

The 12th consecutive interest rate hike puts the savings vs investing debate back in the spotlight.

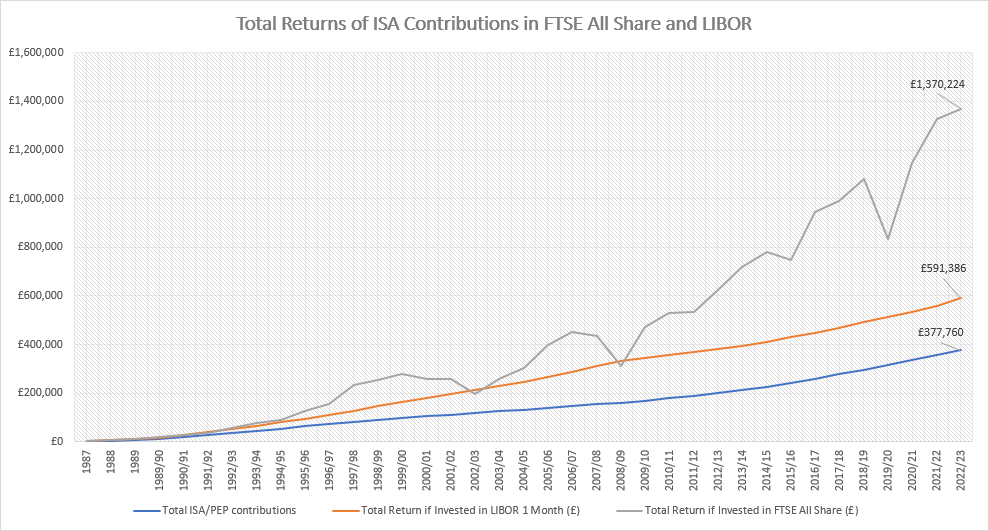

- Investing the full Personal Equity Plan (PEP) and ISA allowance since PEPs were launched in 1987, followed by ISAs in 1999, would have delivered an almost fourfold return of £1.37 million

- When you factor in interest compounded over the period, equities still return over twice as much as cash

The Bank of England’s decision to increase interest rates for the 12th consecutive time has put the savings versus investing debate back into the spotlight.

Savings rates have regained some lustre after a decade in the doldrums, so there are now more options open to savers and investors.

- Invest with ii: Open a Stocks & Shares ISA | ISA Investment Ideas | Transfer a Stocks & Shares ISA

When it comes to wealth generation and financial resilience, cash savings for emergency spending and investments for the longer term are both important and each has a role to play.

New research by interactive investor, the UK’s second-largest investment platform for private investors, illustrates the long-term potential of the stock market versus cash. The data covers a 35-year period in time where UK rates ranged as high as 13.88% and as low as 0.10%.

The platform looked at a scenario where the full annual PEP allowance had been invested annually since the launch of PEPs in 1987. This was then followed by the full annual ISA allowance each year since the launch of ISAs in 1999. It was assumed that the investment mirrored the return of the FTSE All-Share index over the past 35 years, with investments made on 6 April each year.

interactive investor found that the investment mirroring the performance of the FTSE All-Share would have would have delivered an almost fourfold return, making you a hypothetical millionaire, turning total contributions of £377,760 into £1,370,224. This compares to £591,386 had the same amount been invested in cash, using one-month LIBOR rate as a proxy, in a PEP and latter ISA tax wrapper. The data covers the past 35 years to 5 April 2023.

Investing through an ISA (and formerly PEP) wrapper means savings and investments do not incur capital gains tax when sold, and no further tax is payable on any income or interest paid.

Over the past 35 years, the government has regularly increased the annual ISA allowance from £2,400 in 1987 – the PEP allowance - to its current level (£20,000). In April 1999, Chancellor Gordon Brown introduced ISA's to replace PEPs with a limit of £7,000.

Get rich slow

This ‘get rich slow’ approach is not dissimilar to that taken by ii’s ISA millionaires, who at last count had an average age of 73, and most would have likely started their investing journey in PEPs before graduating over to ISAs.

The data is a thought-provoking illustration of the long-term potential of the stock market. And while it goes without saying that only the very fortunate few can afford to make full use of their ISA allowance, the data is still potentially inspiring for those with much smaller pot sizes.

Source: interactive investor/Morningstar. Total Returns (GBP). ICE Libor 1 Month TR GBP and FTSE All-Share TR GBP indexes. ISA and PEP allowances are sourced from ISACO. Past performance is not a guide to future performance).

Dzmitry Lipski, Head of Funds Research, interactive investor, says: “It is interesting to note that the gap between cash and investing returns grew more rapidly than ever following the credit crunch, record low interest rates and a phenomenal recovery in equity markets following the onset of the Covid-19 pandemic.

“Interest rates has risen significantly following 12 consecutive hikes to the Bank of England’s base rate, which has resulted in a notable reprieve in savings rates. Meanwhile, equities have become more volatile recently, and, at the very best, their upward momentum has slowed. There are never any guarantees, but investing in shares will more than likely continue to outperform cash over the long term.

“Apart from maintaining an emergency/rainy day pot, it makes sense for investors to allocate to cash savings as long as they earn positive real return (less inflation).

“Given current inflation rate is much higher than rates on offer from retail banks, it makes sense for long-term investors to favour investing over saving, even if it’s in simple index trackers, a so-called passive investing strategy.

“As we move into a more uncertain market environment, it makes sense for cautious investors - or someone approaching retirement - to focus on capital preservation and limit volatility by maintaining a reasonable cash buffer within a well-diversified portfolio. For those who can afford to keep their money tied up in investments for at least five years and are happy to tolerate inevitable stock market volatility, it is smart to keep money invested.”

Myron Jobson, Senior Personal Finance Analyst, interactive investor, says: “Cash is certainly back. There is no denying the allure of cash following a significant uptick in savings rates, but our research illustrates that over the long term, it is costly to ignore the stock market.

“There isn’t a binary answer in the savings versus investing debate. The answer is you should be doing both if you have the means to do so – whatever your goals and attitude to risk.

“Savings rates are attractive, with the top deals offering a rate of interest north of 4%. But it is unhelpful to view savings rates and investment returns in the same way because it creates an expectation of having a steady annual return when the reality is you could see a double-digit return in one year and a loss the next. The key is to give your money ample time in the market to smooth out the effects of weekly market ups and downs. And don’t forget that cash rates fluctuate too – there’s no telling if a good rate now will still be there in the future.

“While past performance is not indicator of future results, a look back at history shows that investing is king over the long term. The graph demonstrates the wonderful benefits of compounding; how an investor would have grown their assets over time if they had invested the full ISA and PEPs allowances since 1987.

“It is also important to bear in mind that savings rates remain in the doldrums in reals terms because of rampant inflation which remains in double-digits, meaning you'll be able to buy less with your money. In fact, the real value of cash savings has been eroded at an alarming rate in recent history.

“Cash savings is the way to go for short term savings goals – generally those less than five years away. It is also important to maintain a healthy rainy-day fund – three to six months’ salary worth is a good rule of thumb.”

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Important information: Please remember, investment values can go up or down and you could get back less than you invest. If you’re in any doubt about the suitability of a Stocks & Shares ISA, you should seek independent financial advice. The tax treatment of this product depends on your individual circumstances and may change in future. If you are uncertain about the tax treatment of the product you should contact HMRC or seek independent tax advice.