How long will luck last for Centrica's 13% dividend yield?

Times are hard and the yield screams danger, but Centrica has not cut the payout. Next results are key.

13th May 2019 11:28

by Lee Wild from interactive investor

Times are hard and the yield screams danger, but Centrica has not cut the payout. Next results are key.

The weekend press was awash with stories predicting a nasty cut to Vodafone (LSE:VOD) dividend when it publishes full-year results tomorrow. Few would be surprised. But BT (LSE:BT.A) kept shareholders on side last week by committing to its generous payout, and today, Centrica (LSE:CNA), one of the highest yields available anywhere, did the same.

Centrica's trading updates are typically quite dry, with the focus often very much on the number of customers switching their accounts elsewhere. Often, this is for good reason – the British Gas arm lost another 234,000 customer accounts already this year - but that's not Centrica's only problem, and that it has managed to maintain its dividend at 12p per share since 2016 is nothing short of miraculous.

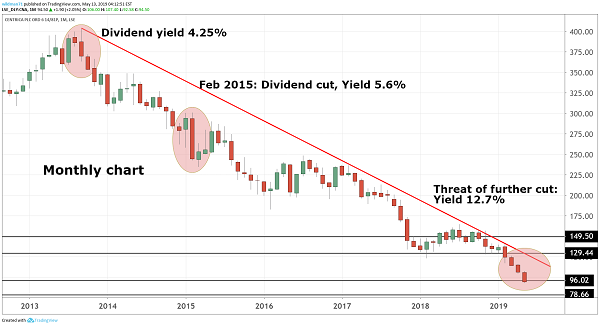

Currently, with the share price at around 94p, Centrica shares yield 12.7%. In the not so distant past, a yield of 6% or more for any company's share would have raised an eyebrow. Not these days. Firms that already paid attractive dividends have seen yields rocket as difficult market conditions feed through to much weaker share prices.

Indeed, the chart below demonstrates how Centrica's yield has increased over the past few years, reflecting the decline in prosperity. However, in its favour Centrica has at least spelled out under what precise circumstances it can afford the dividend.

Source: TradingView Past performance is not a guide to future performance

As long as net debt stays below £3.25 billion and the company keeps operating cash flow within its target of £1.8 billion-£2.0 billion range, shareholders should be okay. Any shortfall will likely trigger a cut to the dividend, which currently costs Centrica almost £700 million every year.

And, once again, the latest trading statements appears to suggest that Centrica can still afford the payout based on those metrics. Chief executive Iain Conn says:

"We continue to focus on those things we can control and as a result we expect to achieve our 2019 cash flow and net debt targets."

After just four months of 2019, Conn is still happy with existing forecasts for adjusted operating cash flow, predicting net debt of between £3 billion and £3.5 billion. However, a very modest uptick in the share price suggests a lack of confidence among investors.

And there's a good reason for that. Conn said back in February that operating cash flow was "under some pressure", and nothing has changed. The UK default tariff cap - a limit on household energy bills in the UK - introduced on 1 January, was part of the reason for a reduction in Centrica's cash flow target from last year's £2.1 billion-£2.3 billion. Meanwhile, warm weather and falling UK natural gas prices are causing problems, and outages are hitting nuclear volumes.

Centrica is still cutting costs heavily - £58 million in the past four months - but we're warned that there will be an impact on first-half numbers, and it’s only the promise of greater cost cuts in the second half – the bulk of the £250 million planned for 2019 - that full-year guidance is being maintained.

We'll get a much better picture of what's going on under the bonnet when Centrica makes public its half-year results on 30 July.

Crucially, Conn promises a strategic update which will include "reflections on the current business portfolio, updated future expectations for the customer-facing divisions and an update to the group's financial framework."

His future as CEO may very much depend on what emerges then. There's a growing fear in the City that the annual dividend cannot survive at 12p. For the record, analysts at UBS predict a 50% cut to just 6p for this year. At current prices, that would still put Centrica on a yield of 6.4%.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.