Reasons why the bear market is far from over

19th July 2022 12:21

by Kyle Caldwell from interactive investor

Professional investors are expecting further pain for stock markets over the summer, explains Kyle Caldwell.

‘Buy low, and sell high’ is one of the most famous investment mantras, but it is notoriously difficult to pull off.

However, following the steep declines for both shares and bonds year-to-date, investors have the opportunity to pick up cheaper prices and higher bond yields.

In terms of equities, US markets and smaller companies have been among the biggest losers year-to-date. The Dow Jones is down 14.5%, the S&P 500 by 20% and the Nasdaq by 27%. In the UK, the FTSE 100 has held up well, down just 2.5%. However, medium and smaller-sized companies have been out of favour, with the FTSE 250 Index and FTSE SmallCap Index down 19% and 16.5%.

The danger, of course, is the risk of moving too early and catching the proverbial falling knife.

Given the volatile market backdrop, some fund managers have been bargain hunting. As we reported yesterday, some have been moving to snap up tech shares on the grounds of their valuations becoming too compelling to ignore. Others have been making changes to their portfolios in response to both inflation and interest rates moving higher, including increasing exposure to banks, a sector that benefits from the current environment.

At such times, fund managers are expected to take advantage of more attractive prices in the hope that over, say, three to five years, their attempts at buying low will be rewarded in the event that market’s recover their poise. After all, history suggests that stock markets do eventually recover. The key is to be patient as any recovery will not happen overnight.

- Funds and trust four professional investors are buying and selling: Q3 2022

- Why these defensive investments will continue to deliver

- Investors ignore strong returns and dump British stocks for US rivals

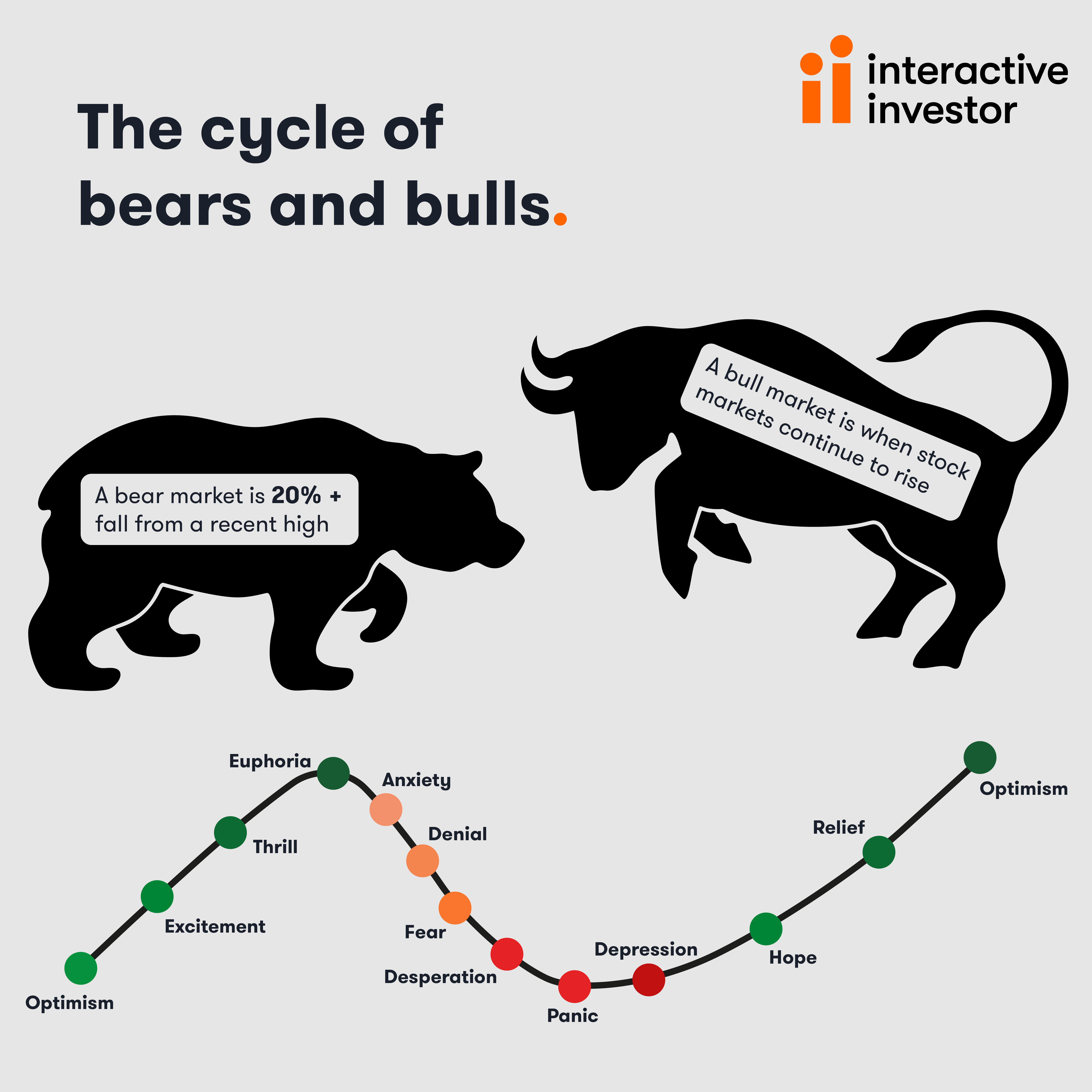

With the prospect of a recession becoming more likely, the bearish outlook is that it could be a challenging couple of years for investors.

Bear market is only ‘mid grizzle’

Duncan MacInnes, fund manager of Ruffer Investment Company (LSE:RICA), shared his latest views with investors this week. MacInnes described the bear market as being “only mid grizzle”.

He noted: “We have high conviction that the bear market is not over, and stocks are not (yet) a buying opportunity.”

MacInnes noted that central bankers have their hands tied, in not being able to act by cutting interest rates or reintroduce quantitative easing to support asset prices (stocks and bonds), due to red-hot inflation.

Over the past decade, both equities and bonds had been buoyed by accommodative monetary policy – low interest rates and quantitative easing (central banks purchasing bonds).

He said: “The old rules no longer apply. Now that the cost-of-living crisis is front-page news, the political imperative is to bring down inflation, not to support asset prices as in previous market sell-offs. Rather, we are in a negative feedback loop, where any bear market rally sows the seeds of its own demise by loosening financial conditions, which in turn forces central banks to counteract.”

MacInnes also expressed concerns that valuations are too high in not reflecting the prospect of a recession occurring. If a recession does play out, this could lead to a further sell-off for shares.

Valuations may not reflect reality

MacInnes said: “Valuations have come down to something more reasonable, but are based on earnings estimates that remain too optimistic, still forecasting growth when flat would be a good result.

“Valuations have fallen because bond yields have risen, not because the equity risk premium has widened.”

In response, he has cut the investment trust’s equity weighting to its lowest level in nearly 20 years, with 25% now held in shares.

Tom Becket, chief investment officer at Punter Southall Wealth, shares the view that the bear market is not over. He points out that the key focus for central bankers is “to try and get the inflation genie back into the bottle” rather than taking action to boost asset prices.

Becket also believes that analyst earnings estimates are “extremely optimistic”, and that bond default levels are “extremely low”.

“Despite the falls we have experienced in equity markets (and the broad and indiscriminate falls in assets in the last few months), the truth is that we haven’t yet seen any obvious reality appear in future earnings estimates, with expectations appearing extremely optimistic.

“This might have to change in the coming quarters and analysts’ enthusiastic expectations might have to be tempered aggressively. At the same time, defaults across corporate bonds could rise from extremely low levels and this could cause significant unease in corporate credit markets.”

Sebastain Lyon, fund manager of Personal Assets (LSE:PNL), which invests in the same cautious manner as Ruffer Investment Company, points out that central bankers’ belated attempts “to remove the punch bowl” by raising interest rates from record low levels and beginning quantitative tightening is “proving highly problematic for the valuations of asset prices, which had been predicated on (almost) free money”.

- Fund and trust ideas to income-boost portfolios to beat inflation

- Recessions are becoming more likely – here’s how to invest

- Scores on the door: the fund sector winners and losers so far in 2022

World’s biggest fund manager not buying the dip

BlackRock, the world’s biggest fund manager, is also adopting a glass half-empty stance. Last month, its BlackRock Investment Institute research team said it was passing on “buying the dip” because valuations had not improved, the US central bank could hike interest rates too aggressively, and corporate profit margins were coming under pressure.

In its latest update, BlackRock’s research team cautioned that “we are braving a new world of heightened macro-volatility –and higher risk premia for both bonds and equities”.

It said: “Central banks are rushing to raise rates to contain inflation that’s rooted in production constraints. They are not acknowledging the stark trade-off: crush economic growth or live with inflation.

“The Federal Reserve, for one, is likely to choke off the restart of economic activity, and only change course when the damage emerges. We see this driving high macro and market volatility, with short economic cycles.”

Tacking inflation will boost stock market confidence

In terms of catalysts that could provide a boost for stock markets in the months ahead, containing inflation is seen as key.

Stephen Anness, head of the global equities team at Invesco and fund manager of the Invesco Select Global Equity Income Share Portfolio (LSE:IVPG), says: “This bear market has been driven by increasing interest rates and, more recently, concerns about economic growth. For markets to recover, we are likely to need to see inflation expectations brought under control.

“Many companies that are exposed to housing and consumer spending have been hit hard along with semiconductors and certain areas of tech. If inflation expectations are tamed such that the market can price in peak interest rates, I would expect those sectors to perform well in a rebound.”

Key risks for markets in the months ahead

Based on the arguments above, the key risks are a prolonged recession, inflation remaining red-hot, and share price valuations being too optimistic.

In the months ahead, they will have a big bearing on whether already-battered stock markets will enter a full-blown crisis and plunge further – or recover their poise.

Becket’s view is that any impending recession “is unlikely to be broadly disastrous, unless we see asset prices collapse”.

But he urged investors to brace themselves for further short-term pain, saying: “We expect that future projections for corporate earnings will start to fall rapidly in the coming months, leading the markets to endure a volatile summer.

“However, assuming that we don’t see a prolonged economic slump, 2023 could see an improvement in the prospects for companies and a resumption of the positive trends in corporate profits.

“We fully expect corporate loan defaults to rise from a low base, but we do not currently believe that this dynamic will be sufficient to cause either a credit crisis or a seizure in the credit markets.”

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.