UK income investors short-changed despite the dividend boom

It's been a great year for dividends, but not for income fund investors. We explain why.

10th September 2019 09:26

by Kyle Caldwell from interactive investor

It's been a great year for dividends, but not for income fund investors. We explain why.

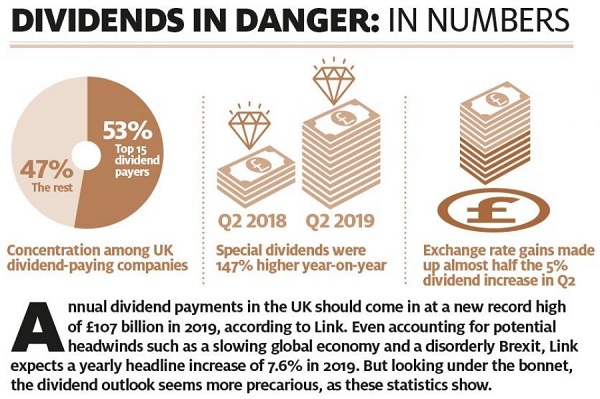

UK equity income investors should be popping the champagne corks. This year is set to be the third successive record-breaking year for dividend payments, which are expected to break the £100 billion barrier for the first time.

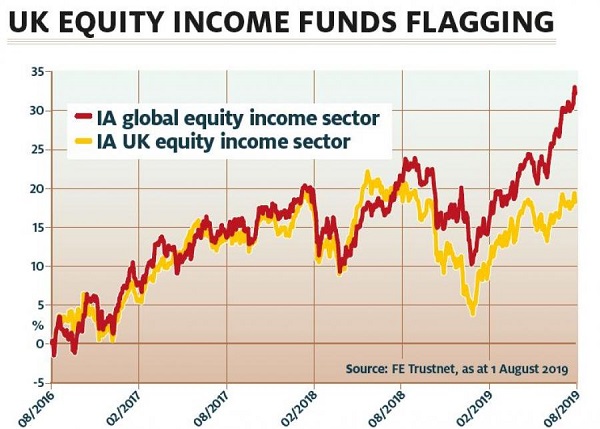

But fund investors have less to cheer about, as on the whole the performance of UK equity income funds since the Brexit vote has been nothing to get excited about. Over three years to the end of July, the average fund in the Investment Association (IA) UK equity income sector gained 18.1%.

In contrast, global income funds, which can spread their nets far and wide, have fared much better: the average fund in the IA global equity income sector returned 32.1%.

As a report published in June by Morningstar notes:

"The performance of these funds has been especially poor in recent years. Regardless of possible benefits, if returns are poor, investors will go elsewhere, which could explain why UK equity income funds have lost such large volumes of assets."

A staggering £15.3 billion was withdrawn from the sector between January 2016 and the end of April this year. Surprisingly, over this period it was not Neil Woodford who suffered the most: half of investor withdrawals, some £7.5 billion, leaked out of Invesco's equity income funds managed by Woodford's protégé Mark Barnett.

Despite poor investor sentiment and pedestrian performance from UK equity income funds, on various yardsticks of value the UK stock market looks attractive – particularly in regard to its dividend yield, with the FTSE 100 and FTSE All-Share indices yielding comfortably in excess of 4%. The yields on offer today are higher than they have been historically and are attractive relative to other developed markets, and indeed bonds, which should whet the appetites of income-seekers.

Backward step

According to RWC Partners' Ian Lance, negative sentiment and the shunning of the UK by overseas investors have pushed domestic equity valuations "back to the 1990s".

He says:

"UK equities are deeply, deeply out of favour today, despite the valuation of UK equities now standing at the biggest discount to the MSCI World index we have seen since the 1990s, while the gap between UK dividend yields and bond yields is as extreme as it has been since the First World War."

But investors should not be swayed by the market's high yield alone, warns Blake Hutchins, manager of Money Observer Rated Fund Investec UK Equity Income. He points out that the yield of the FTSE All-Share index is heavily influenced by its top 10 big names, so investors need to tread carefully.

Hutchins notes that the median average yield for the index is lower than 4% plus, at 3.2% . He says:

"The headline dividend yield for the market as a whole is optically very attractive. But investors need to take a step back and not just assume the market yielding more than 4% is a sign of unbelievable value."

Overseas shares that investors should learn to love

Indeed, he adds, high yields should be viewed with scepticism, as they are a sign that the share price of the company in question is out of favour for a particular reason. Therefore the high yield for the UK market as a whole is a reflection of the huge uncertainty about the form Brexit will take. The weak pound has also subdued sentiment and been a key reason why investors have been giving UK assets the thumbs down – although it has proved a boon for the more internationally focused businesses in the FTSE 100 index.

When examining the state of play of the UK dividend market, there is a noteworthy split between value shares and those that fit the quality description – a point Francis Brooke, manager of the Troy Income & Growth (LSE:TIGT), alludes to in our Money Maker interview. At the high-yielding end, offering yields of 7%-plus, are the more economically sensitive, domestically focused businesses, with housebuilders well represented.

In contrast, businesses viewed as being price-makers rather than price-takers and therefore able to continue to prosper come what may, such as Unilever (LSE:ULVR) and Diageo (LSE:DGE), are offering low yields of around 3%. Both companies have been strong performers since the financial crisis and investors continue to be attracted to these shares, despite them becoming increasingly expensive.

On the whole, fund managers in the IA UK equity income sector have been more drawn to the high-yielding end of the market, an approach that has not yet paid off. As Morningstar notes, the FTSE 250 index, which houses the domestically focused UK shares that fund managers have been viewing as value opportunities, has also performed poorly over the past three years. The value style of investing has also remained out of fashion with investors, which has not helped.

Domestic trouble

Ben Willis, head of portfolio management at Chase de Vere, says that to some extent fund managers tilting their portfolios towards domestically flavoured UK business, including Woodford, have been unfortunate.

He says: "Woodford's problems started because of his belief in undervalued UK companies, which he thought would perform well. He has been waiting for this, and in the meantime his performance has suffered. The uncertainties around Brexit added to his woes, as the UK stock market has been ignored by global investors."

Willis believes the approach of investing in domestic shares will eventually "come good", but suggests that a smarter tactic is to size up funds that strike a balance by holding a mixture of domestic UK shares and larger international UK companies that have performed well over the period. He picks out Schroder Income Growth (LSE:SCF) and Rathbone Income as two funds that are doing just that.

He adds: "Any Brexit outcome, preferably a deal of some kind, would be good news for UK shares. This would bring clarity to the UK economy and should provide the impetus for global investors to return to the UK stock market. At some point currently unloved UK companies should perform well and benefit investors. Investing based on attractive valuations in out-of-favour firms is usually a good approach to achieving long-term returns."

In a similar vein, Lance argues that domestic businesses themselves "are not doing badly". He adds:

"It is sentiment that has de-rated that subset of companies, which should be an opportunity for investors."

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.