Taking an UFPLS lump sum payment

You can now take an UFPLS lump sum from your pension online.

- The process should take around 30 minutes. It usually takes no more than 10 working days after this to receive your lump sum payment.

- An Uncrystallised Funds Pension Lump Sum (or UFPLS for short) is a flexible way to take a lump sum from your pension. You decide how much you want to take each time. The first 25% of each amount is tax-free, subject to a maximum of £268,275, and the rest is taxed as income. You don’t have to take your whole pension this way. You could also take some of your pension using drawdown and/or as an annuity.

Important information on pension withdrawals

Once a request to make a withdrawal from a pension has been made it cannot be cancelled. This means Tax Treatment & Pension Allowances changes cannot be reversed. If you are unsure do not request a withdrawal. We recommend speaking to an authorised financial adviser or seeking guidance from the Government’s Pensionwise Service.

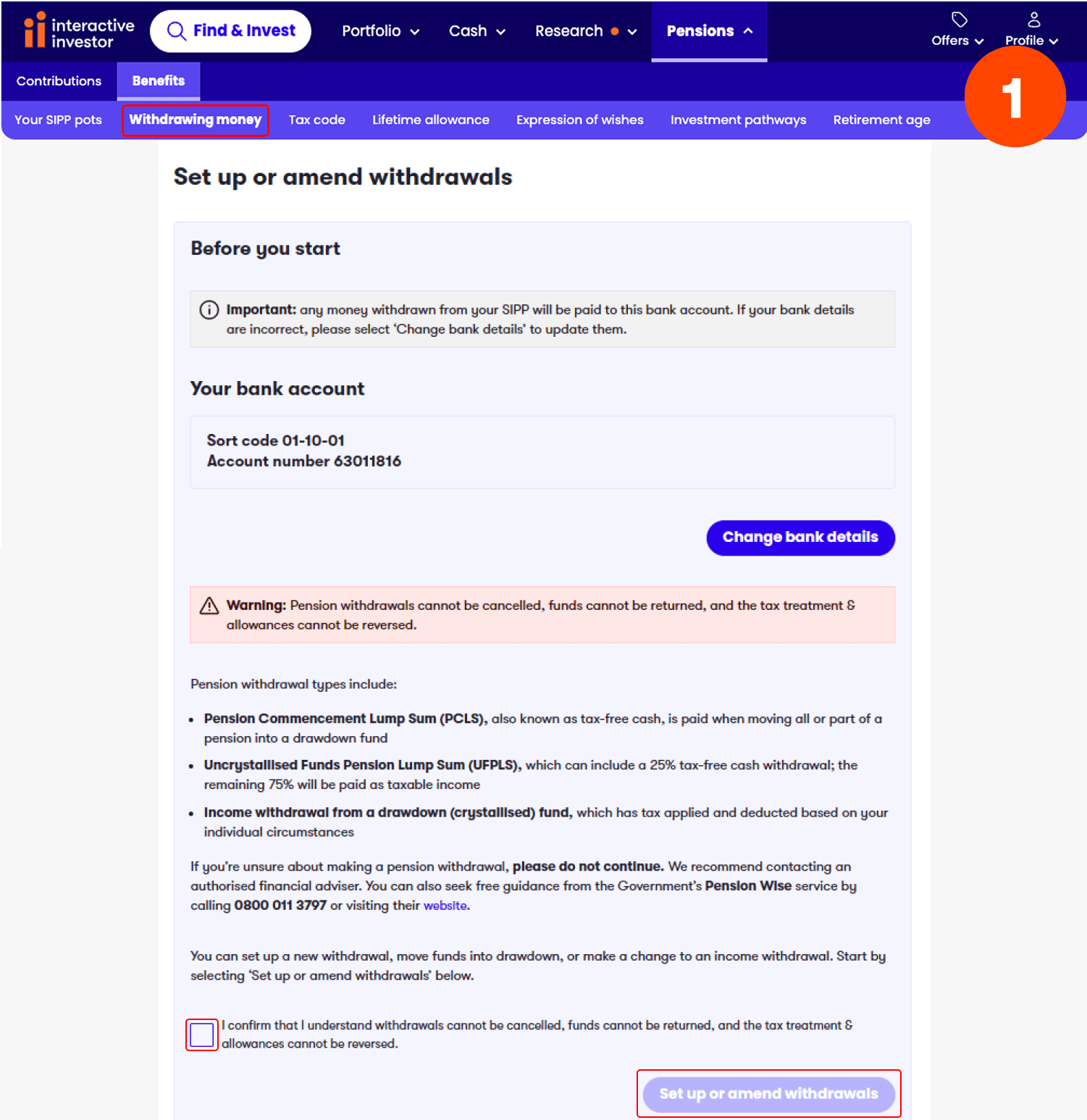

Step-by-step

Step 1.

From the 'Pension/Benefits' menu in your online account, select 'Withdrawing money'.

If you haven't done so already, you will need to add a bank account before you can continue.

Confirm that you understand that requests cannot be cancelled and the tax treatment cannot be reversed.

Then select 'Set up or amend withdrawals'.

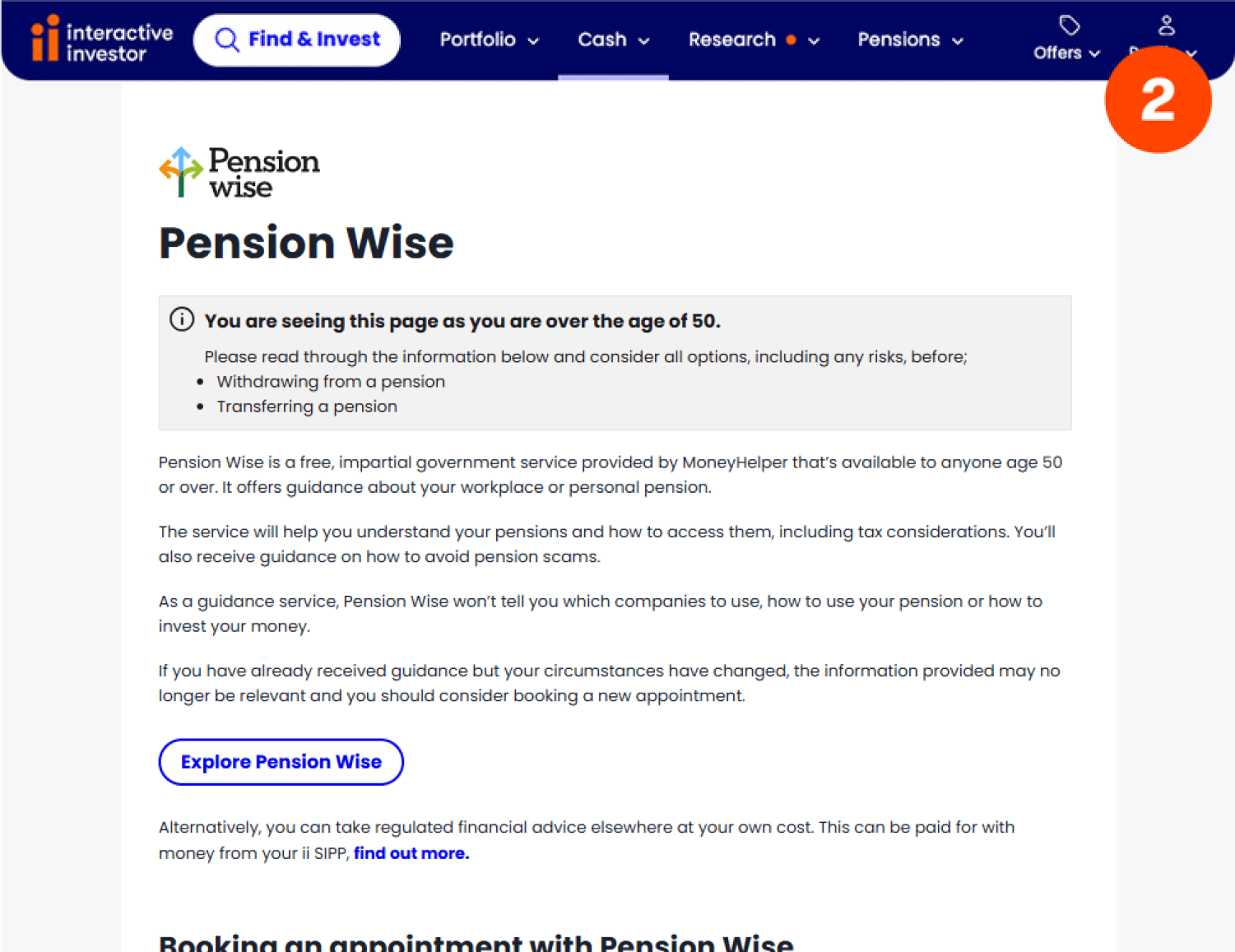

Step 2.

You will then see a page with information about taking guidance from Pension Wise before withdrawing from your pension. From here you can either choose to book an appointment with Pension Wise, let us know that you’ve already had an appointment or confirm that you wish to proceed without having an appointment.

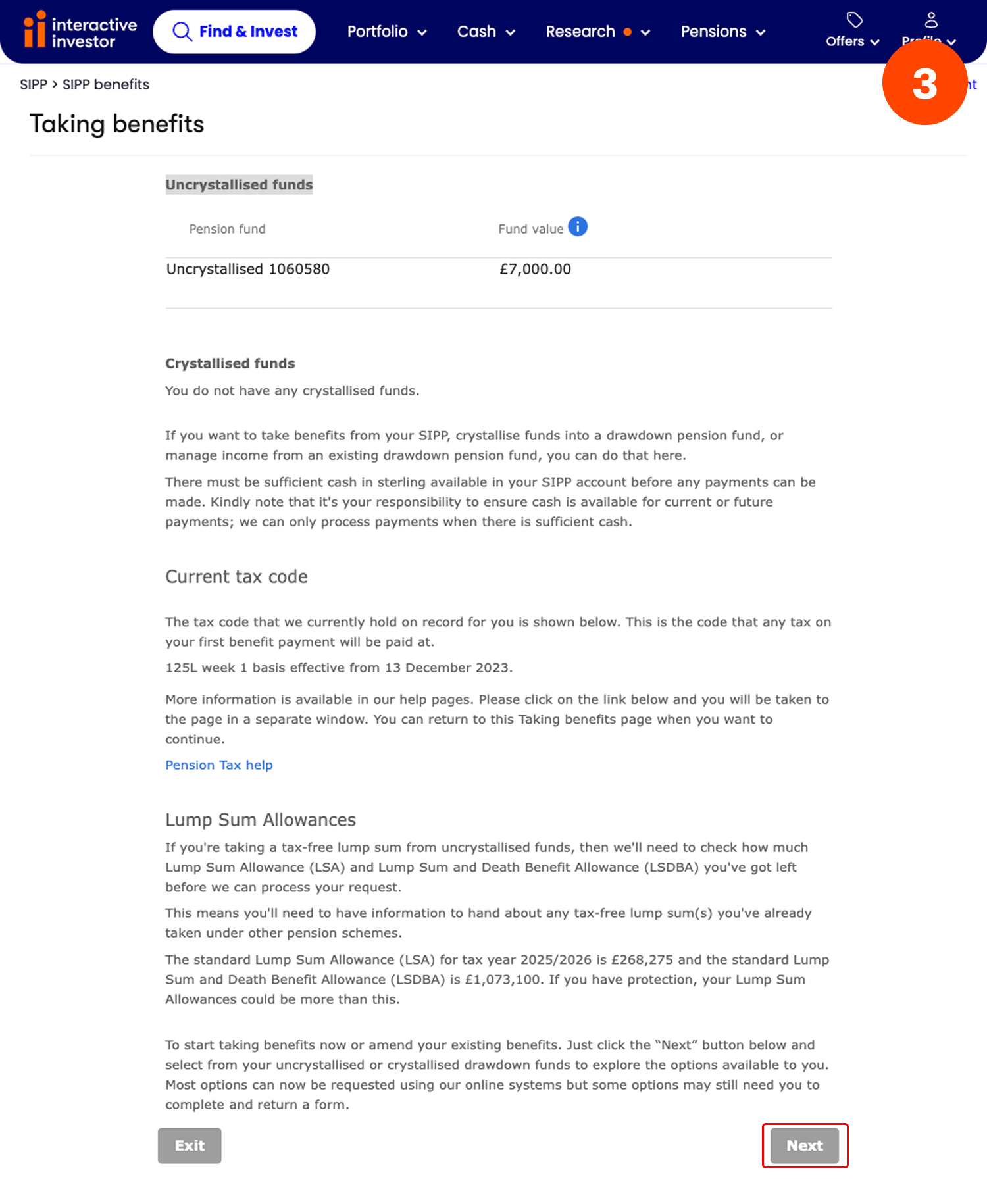

Step 3.

You will then see a summary of your available pension funds. Scroll to the bottom of the page and click ‘Next’.

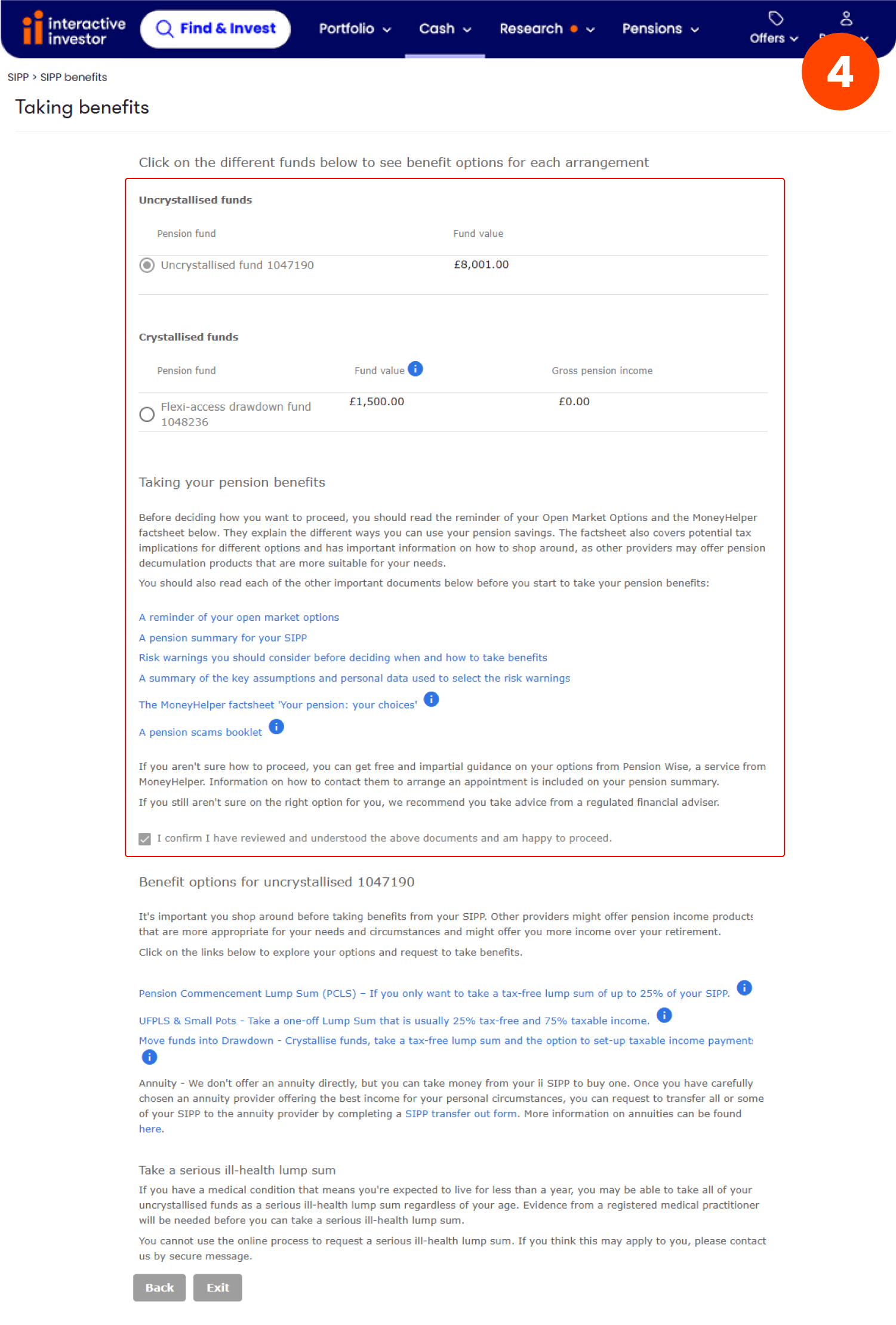

Step 4.

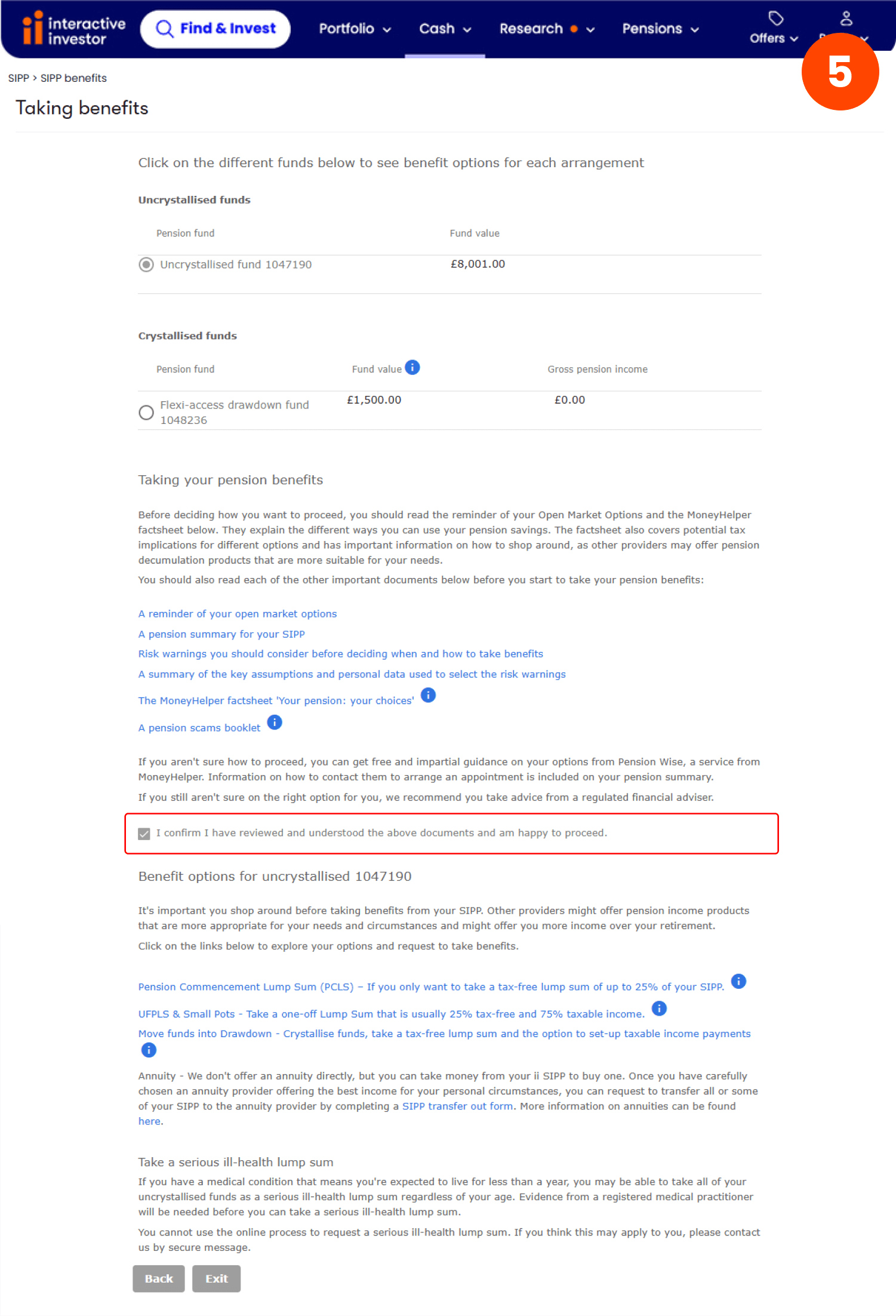

Select your uncrystallised fund (this simply means funds you haven't moved into drawdown yet).

Take time to read the six documents under ‘Taking your pension benefits’.

Doing this will allow you to proceed to the next step.

Step 5.

Tick to confirm you have read the documents and select ‘UFPLS & Small Pots - Take a one off Lump Sum that is usually 25% tax-free and 75% taxable income’.

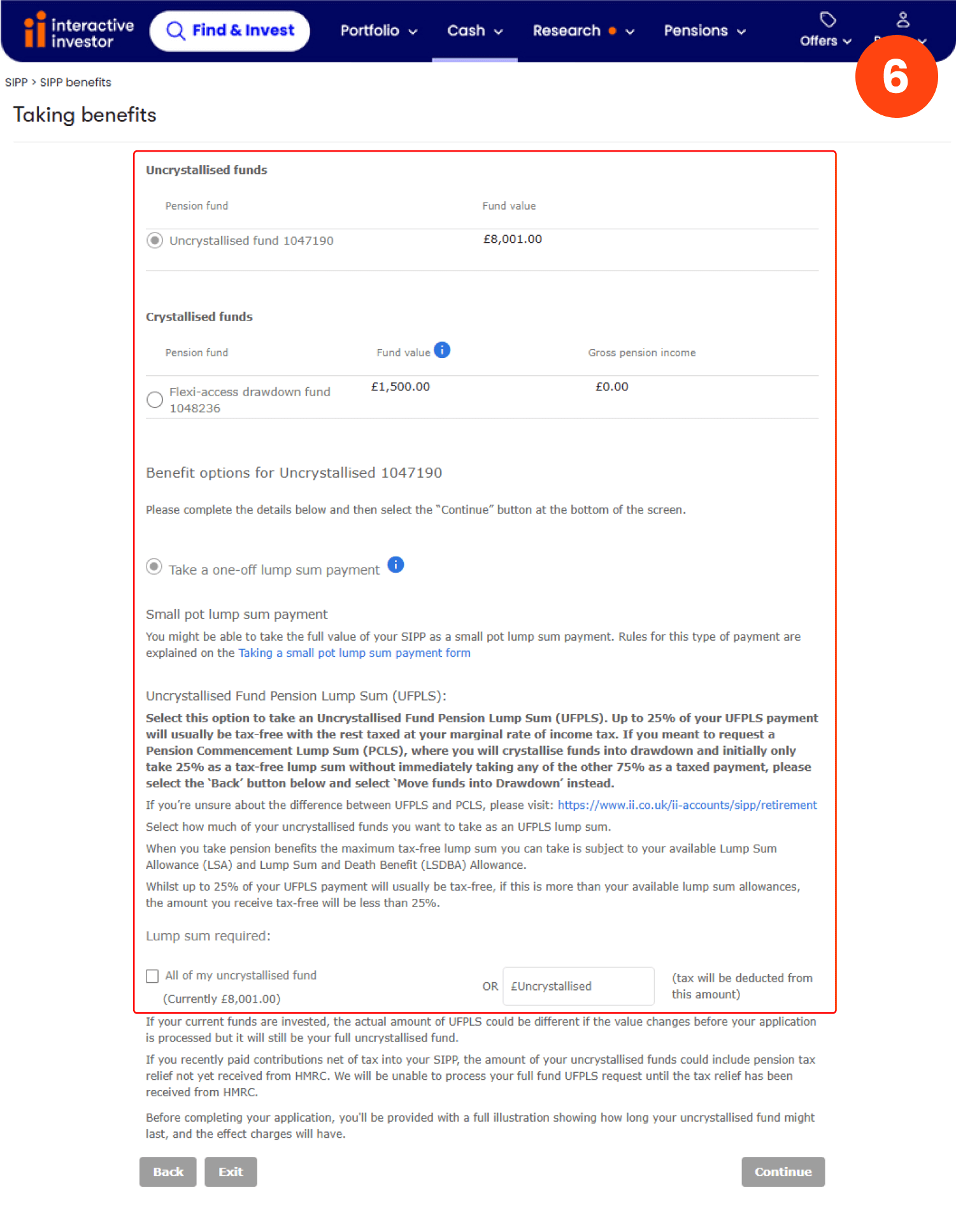

Step 6.

Choose the amount you want to take as an UFPLS lump sum. Select ‘All of my uncrystallised fund’ or enter the amount you wish to take.

The minimum lump sum that you can request is £1,000.

Step 7.

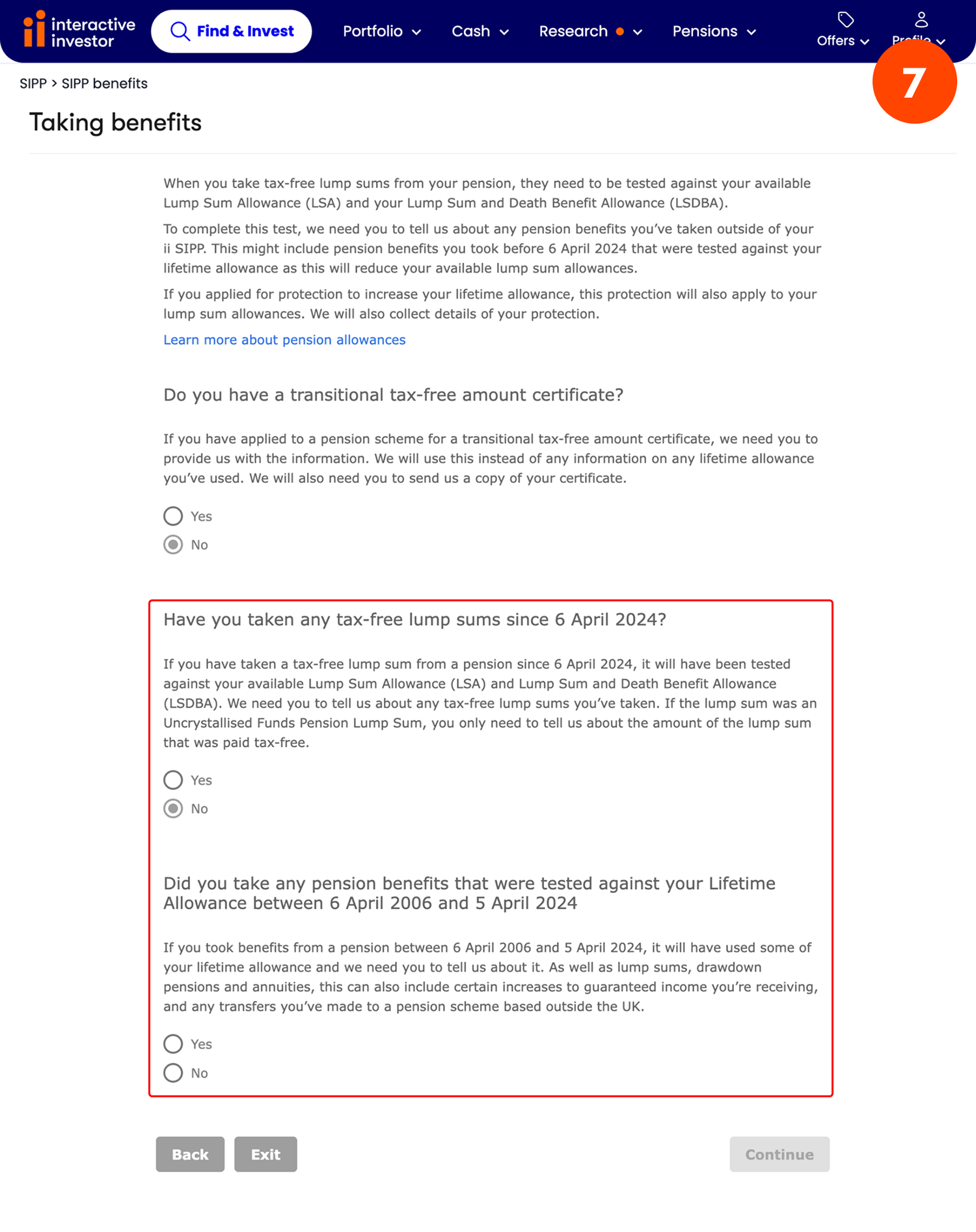

Taking a lump sum payment will count towards your Lump Sum Allowance (LSA) and Lump sum and Death Benefit Allowance (LSDBA). Please select whether you have taken any tax-free lump sums from a pension on or after 6 April 2024.

Taking benefits from a pension (withdrawing money) before 6 April 2024 will have counted towards your Lifetime Allowance (LTA). Please select whether you took any benefits from a pension (withdrew money) between 6 April 2006 and 5 April 2024.

Then select whether you took any benefits from a pension (withdrew money) before 6 April 2006.

Step 8.

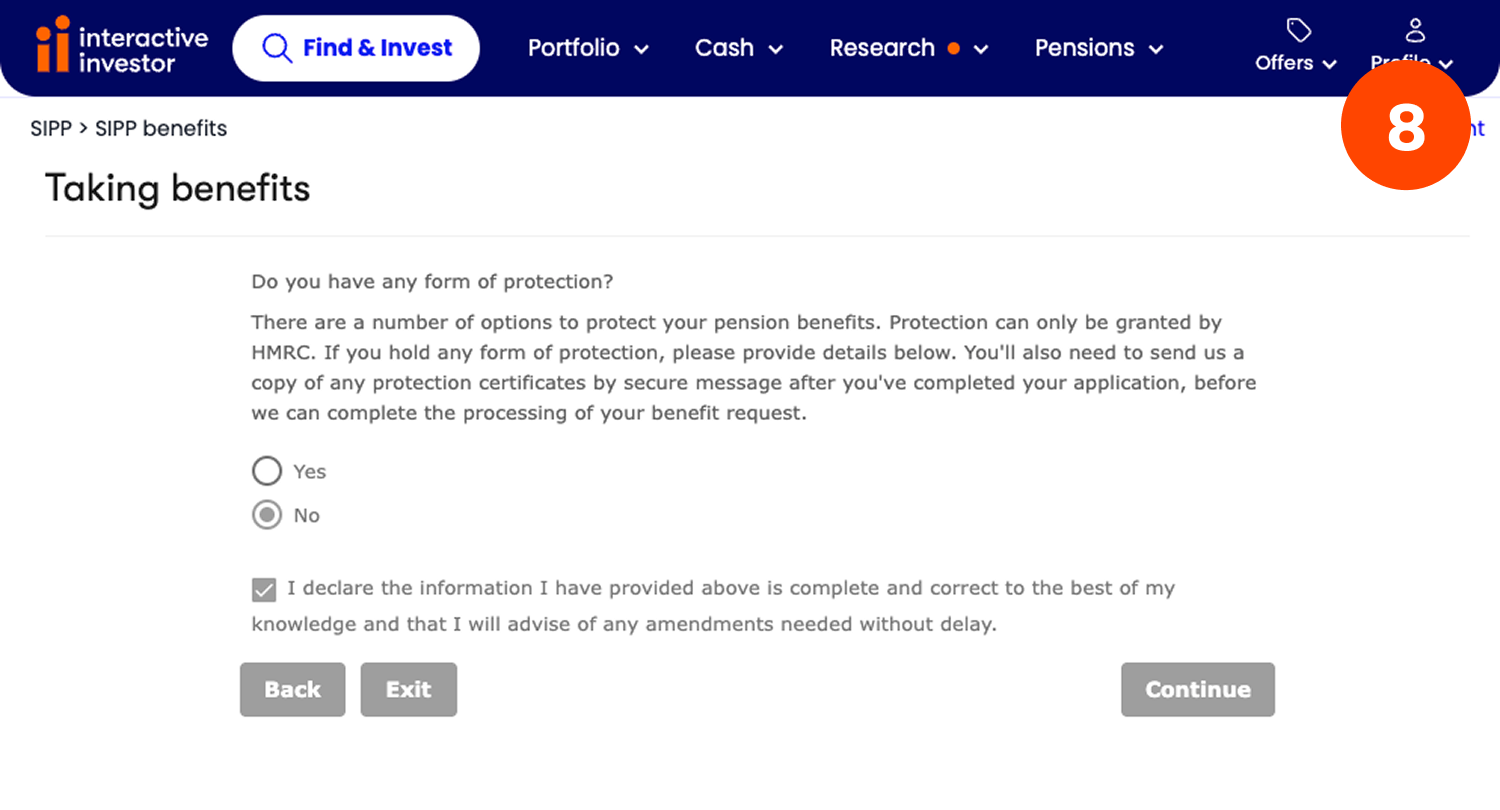

Then confirm whether you have any form of Lifetime Allowance protection.

If you have any Lifetime Allowance protection, we will need a copy of any protection certificates before we can set up your benefits.

- Please send us a secure message from your online account and attach the document(s).

- Or you can post the documents to: Pensions Team, interactive investor, 4th Floor, 3 South Brook Street, Leeds LS10 1FT.

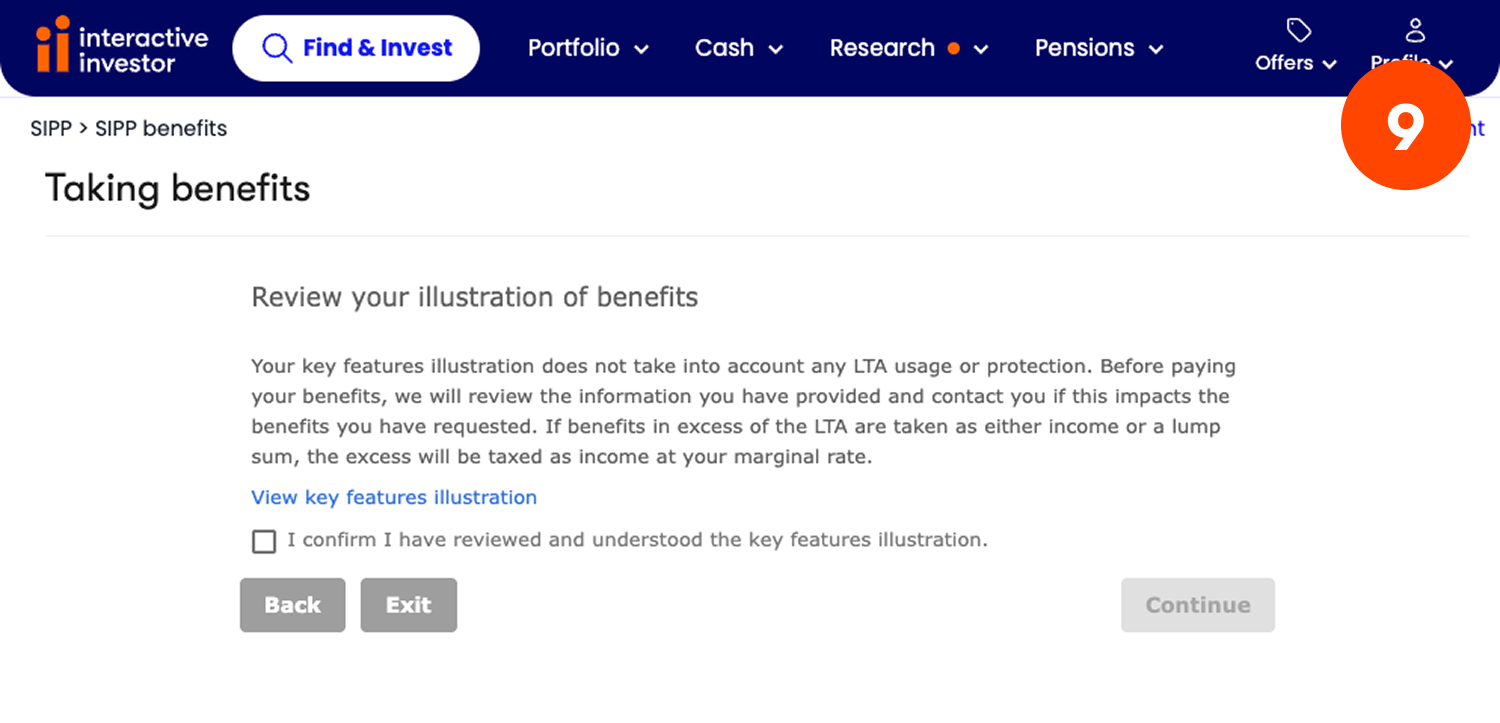

Step 9.

We will then ask you to review your illustration of benefits.

Click 'View key feature illustration' to see a breakdown of your drawdown arrangements.

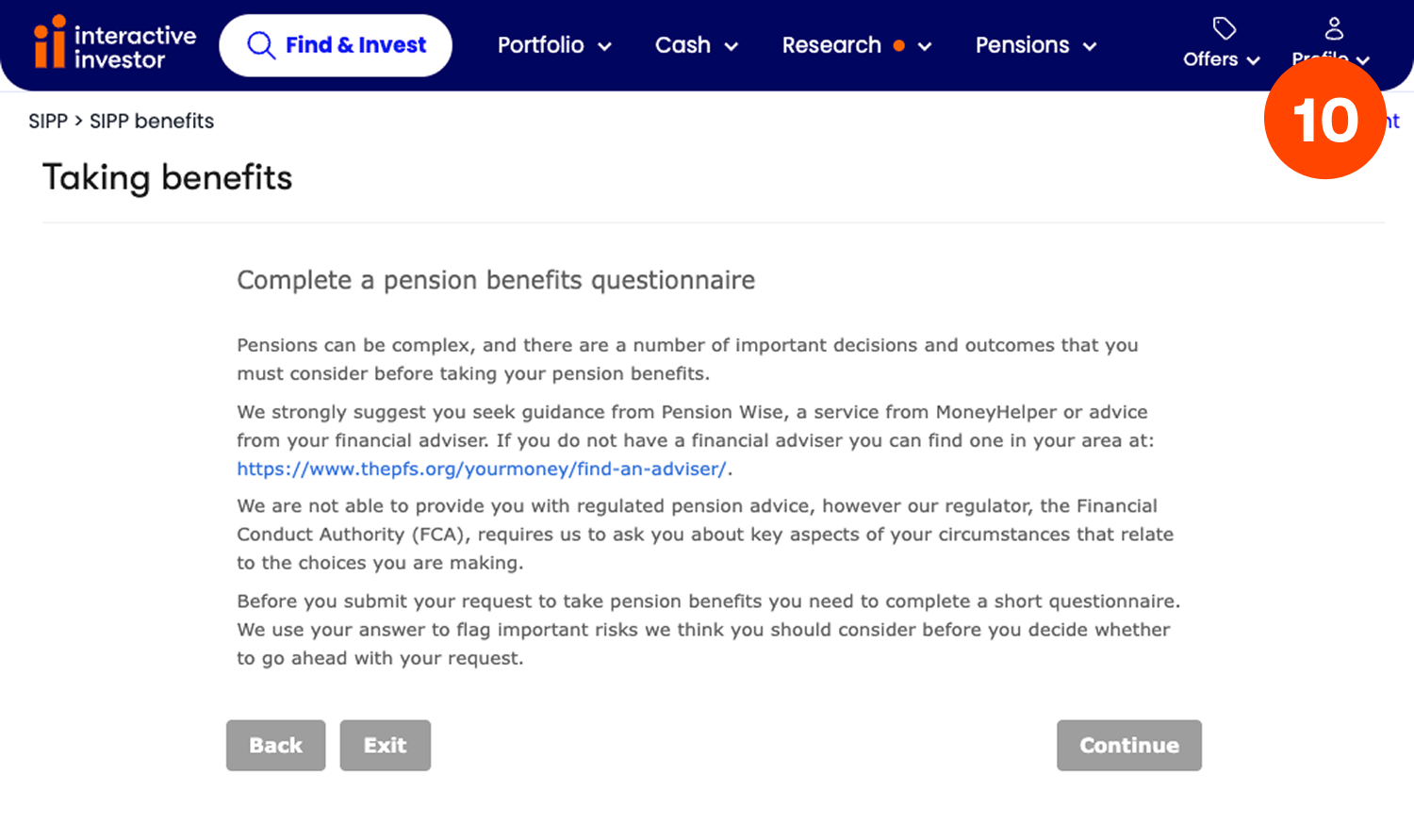

Step 10.

You will then be asked to complete a pension benefits questionnaire. Your answers will flag the important risks you should consider before taking benefits.

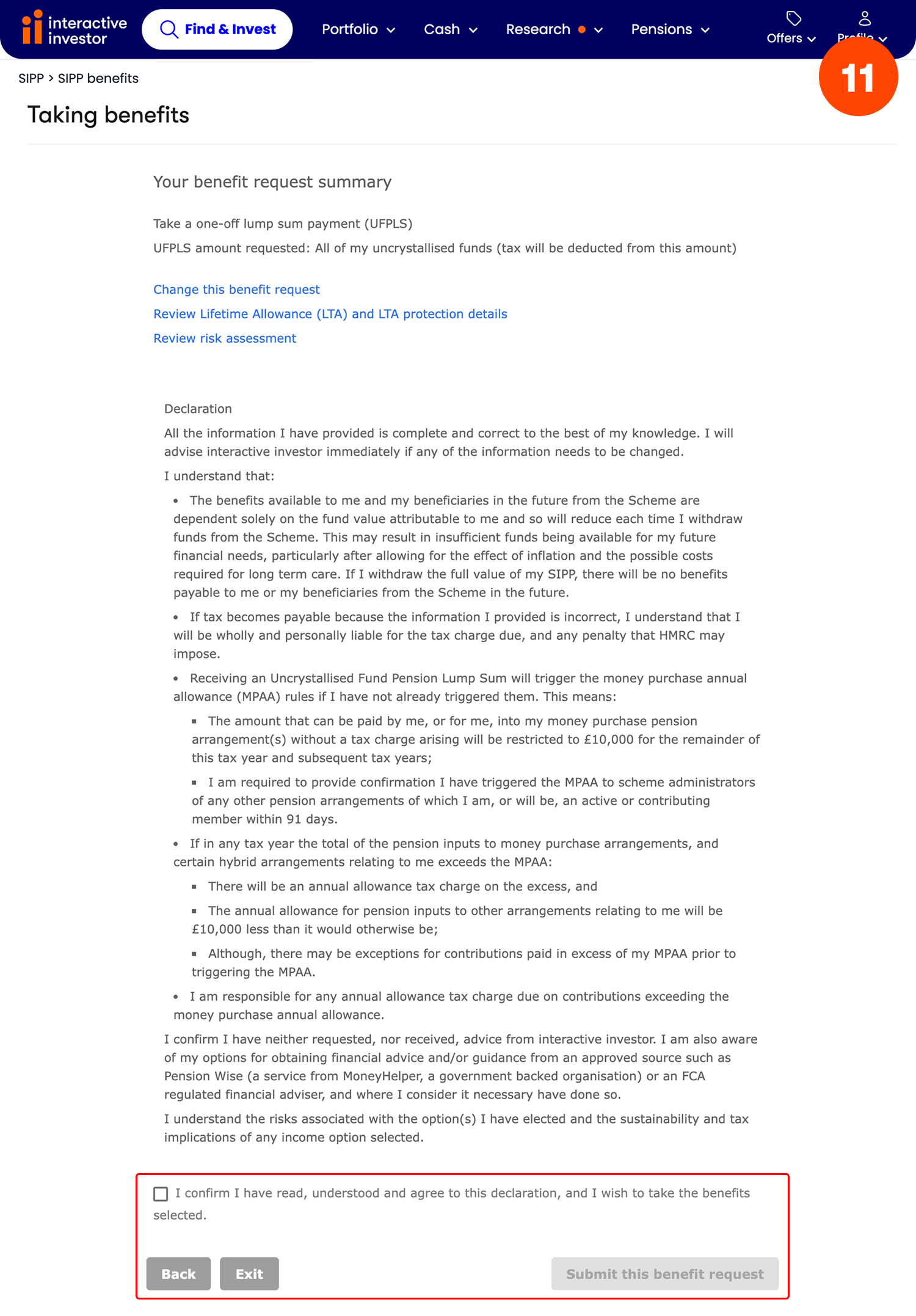

Step 11.

Check your benefit request summary and make sure it is accurate.

Once you have read through the declaration, click ‘Submit this benefit request’.

What’s next?

- It usually takes no more than 10 working days to set up your benefits.

- If you choose to take a taxable income payment as well as your tax free lump sum and if this is your first income withdrawal from your SIPP, you may be charged an emergency tax rate if we have not received confirmation of your tax code from HMRC.

The emergency tax code assumes that you will carry on receiving the same amount each month even if the money you are taking is a one-off withdrawal. On an emergency tax code, you will also only receive 1/12th of your tax-free personal allowance. This may mean you pay more tax than is actually due. You can reclaim emergency tax on pensions by contacting HMRC directly.

How can Pension Wise help?

If you have a defined contribution pension scheme and are 50 or over, then you can access free, impartial guidance on your pension options by booking a face to face or telephone appointment with Pension Wise, a service from MoneyHelper.

If you are under 50, you can still access free, impartial help and information about your pensions from MoneyHelper.