ii SIPP

Important information: The ii SIPP is for people who want to make their own decisions when investing for retirement. As investment values can go down as well as up, you may end up with a retirement fund that’s worth less than what you invested. Usually, you won’t be able to withdraw your money until age 55 (57 from 2028). Before transferring your pension, check if you’ll be charged any exit fees and make sure you don't lose any valuable benefits such as guaranteed annuity rates, lower protected pension age or matching employer contributions. If you’re unsure about opening a SIPP or transferring your pension(s), please speak to an authorised financial adviser.

Important information on pension withdrawals

Once a request to make a withdrawal from a pension has been made it cannot be cancelled. This means Tax Treatment & Pension Allowances changes cannot be reversed. If you are unsure do not request a withdrawal. We recommend speaking to an authorised financial adviser or seeking guidance from the Government’s Pensionwise Service.

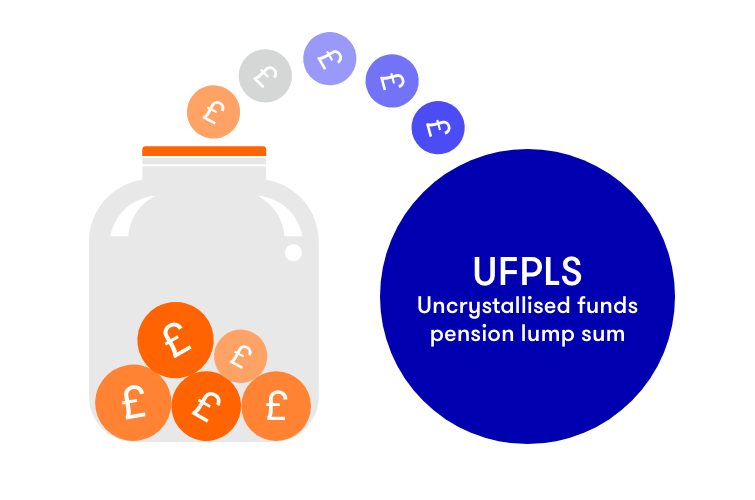

What is UFPLS?

UFPLS – or Uncrystallised Funds Pension Lump Sum to give it its full name – is a flexible way to take a lump sum from your pension.

It might sound confusing – and impossible to pronounce – but it’s actually quite straightforward.

Its flexibility means an UFPLS may be worth considering if you need access to a lump sum but you haven’t yet decided how you’d like to access your pension in the long term. It can also be an option if you have a small pension pot, especially where it might not be worth buying an annuity or setting up drawdown.

How does UFPLS work?

You decide how much you want to take each time. The first 25% of each amount is tax-free, subject to a maximum of £268,275, and the rest is taxed as income.

You don’t have to take your whole pension this way. You could also take some of your pension using drawdown and/or as an annuity.

UFPLS: a simple example

John has a pension worth £600,000. He decides to take a £30,000 UFPLS lump sum, leaving £570,000 in his pension.

- The first 25% (£7,500) of this lump sum is tax-free.

- The remaining £22,500 is taxed like normal income.

John can take another lump sum at any time - or choose an alternative option, such as drawdown or an annuity.

How to take UFPLS from your ii SIPP

There are no charges for taking a lump sum UFPLS payment with ii. It's all covered by your monthly SIPP fee.

- You can now take a lump sum UFPLS payment using your online account.

- You’ll need to follow the process every time you want to take a lump sum.

- The process should take around 30 minutes. It usually takes no more than 10 working days after this to receive your payment.

- Click here for a step-by-step guide on how to take an UFPLS lump sum payment online.

How is UFPLS taxed?

The first 25% of each UFPLS payment is tax-free, subject to a maximum of £268,275. The remaining amount is taxed like normal income:

- If you have no income from any other sources, the first £12,570 is tax-free.

- 20% on income between £12,570 and £50,270.

- 40% on income between £50,270 to £125,140.

- 45% on income above £125,140.

Tax on your first UFPLS

When you first take an UFPLS, you will usually be given an emergency tax code, unless your pension provider holds an up-to-date tax code for you.

This emergency tax code will treat the UFPLS as an income that will continue to be paid each month. This means it is likely to result in an overpayment of tax when you make this first withdrawal.

If this happens, you can claim back the overpaid tax from HMRC.

Learn more:Emergency Tax on Pensions

UFPLS FAQs

Getting financial advice

The way you access your pension could affect your standard of living during retirement so we recommend seeking professional financial advice. An independent financial adviser will be able to assess your circumstances and recommend the most appropriate action to achieve your goals.

How can Pension Wise help?

If you have a defined contribution pension scheme and are 50 or over, then you can access free, impartial guidance on your pension options by booking a face to face or telephone appointment with Pension Wise, a service from MoneyHelper.

If you are under 50, you can still access free, impartial help and information about your pensions from MoneyHelper.

What are the alternatives to UFPLS?

There are two other ways you could take an income from your pension.

Drawdown

Allows you to take up to 25% of your pension tax-free (subject to a maximum of £268,275), and set up regular or one-off income payments for the rest. Learn more.

Annuity

Gives you a guaranteed income in return for some or all of your pension. Learn more.

You are free to use one of more of these options when accessing your pension, with choices determined by factors such as the size of your pension, income requirements and your tax position.