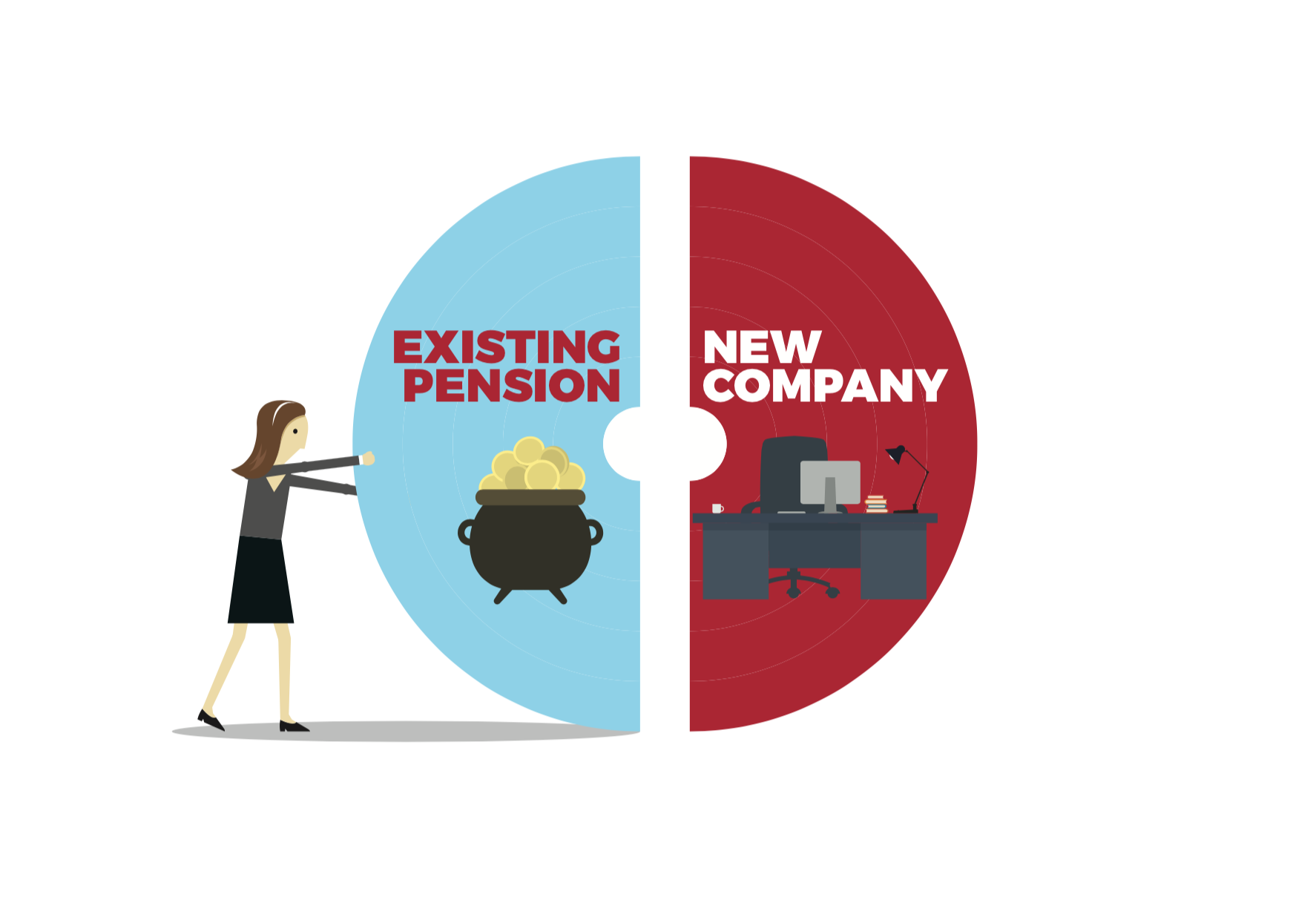

New job, old pension? It’s time to review the situation

6th March 2019 11:27

by Lily Canter from interactive investor

Evaluating your pension may be the last thing on your mind when changing jobs. But new schemes can offer both opportunities and drawbacks. Here are the key questions to ask yourself and your new employer.

Getting a new job is the ideal time to take stock of your existing pensions to see what investment you already have and to gain a clear idea of where you are going.

“It is not something we like to look at, as we think of pensions as being at the end of our lives. But it is a good opportunity to think about the kind of income we would like in retirement,” says Melinda Riley, head of policy pensions guidance at the Single Financial Guidance Body.

The first few weeks of a new job is the best time to get your pension savings in order before you let things slip.

- Discover how to: Open a SIPP | Best SIPP Investments | SIPP Withdrawal Rules

“No one jumps out of bed in the morning because they want to sort out admin. It makes sense, then, to deal with it in the first week in a new job before the real work starts and when you’re already handling admin with your new employer,” advises Ed Monk, associate director for personal investing at Fidelity International.

What scheme do I currently have?

First of all, check whether you have a workplace pension with your previous employer, as you may have been automatically enrolled in one when your started working for them.

When you leave, you should be sent a statement of benefits. If it doesn’t turn up within a couple of weeks, ask for one. The statement should include a current value of the account and the transfer value. Find out if there are any penalties for transferring the pension to a new scheme or any additional charges.

Work out whether you hve a scheme that pays a guaranteed income based on your salary or one that pays out based on the overall contributions made by you and your employer (so defined benefit or defined contribution). Also make sure your pension provider has up-to-date contact details, especially your address. The same applies if you have a personal pension.

What are my new pension arrangements?

The law requires every employer to automatically enrol UK workers into a workplace pension scheme if they are at least 22 years old, under state pension age and earn a minimum of £10,000 a year. The scheme may be referred to as a company or occupational pension.

Find out from your new employer what the arrangements are, as you may have to buy into the scheme if you want to transfer your existing pension across.

Some schemes also have restrictions, which mean you have limited time to transfer a pension into the new scheme – often a year.

“For your new pension, most employers these days have clear guidance on what you need to do and a process to help you set up contributions, increase them over time and select investment choices for your money,” says Mr Monk.

“These will include default choices if you don’t feel confident making investment decisions, so you don’t have to worry about making any big mistakes. Bear in mind that some schemes have a window for you to set contributions and investment choices – miss it and you might have to wait for next year.”

Should I leave or transfer it?

There are generally three pension options when you change jobs. You can leave your old pension where it is, move it to your new employer’s workplace pension scheme or transfer it into a personal pension arrangement.

“Transferring it might not always be in your best interest, particularly if it is a defined benefit scheme with a guaranteed final salary income,” says Andrew McCombe, independent financial adviser (IFA) of Go IFA.

You can have as many pensions as you like, so you can freeze your old pension and join another scheme with your new employer.

Equally, a pension can follow you throughout your career and you can transfer it as many times as you move jobs although there may be costs for moving your money.

“It’s also really important that you don’t give up valuable features of an old scheme, such as a guaranteed annuiy rate which would allow you to buy a higher level of income when it comes time to retirement. But if your new scheme is offering better terms – similar or the same investments for a lower annual charge, and without giving up valuable benefits – then you may wish to transfer your money to your new scheme if this is possible,” Mr McCombe adds.

If you have a large pension that comes close to the lifetime allowance of £1.03 million, it can be advantageous to have access to separate pensions containing less than £10,000 because these can be accessed without triggering a potential tax charge.

Do I need to increase my contributions?

Benefits within pensions are so varied that it can be difficult to compare like for like and to know if you are moving from a better to a worse scheme, but it is always advisable to contribute more if you can.

“If you have been promoted, you should think about contributing more to your pension scheme. That way, you don’t notice that you are missing it. Your employers may match these contributions too,” says Ms Riley.

You should always aim to maximise pension benefits particularly the amount an employer will match.

“It’s normal for employers to match your contributions up to a certain level, so make sure you contribute at least enough to max out their contribution, and more if you can afford it,” says Mr Monk.

Should I have multiple pension pots?

You may be someone who prefers to track all of their money in one place and have one pension, but there is also no harm in hedging your bets and having several schemes.

“As long as you know where they are and what charges are on them, there is nothing wrong with having several pensions,” says Ms Riley.

Alternatively, you can bring old work pensions together in your own Self-Invested Personal Pension (Sipp). By doing this, you will be able to see all your pensions in one place, which means you are less likely to lose track of your savings and will be encouraged to increase contributions when you can.

How is my short-term health?

An important consideration is your health and family circumstances, particularly if you are concerned about dying before retirement.

Make sure you understand how much your scheme will pay out on your death as this may affect whether you transfer it or not.

Defined benefit schemes are much reduced on your death as you are no longer paying into the pension whereas defined contribution, workplace or personal pensions may pay out more to your family.

Personal pensions can be passed down the generations and are generally not subject to inheritance tax so are a good way of securing your family’s financial future. Make sure your expression of wishes nomination form is up to date, so the correct person/people receive any death benefits.

Do I need financial advice?

As a starting point, talk to your company’s HR department if they have one and also contact your current pension provider, so it can talk you through your annual pension statement.

Never accept advice from a cold-caller as cold-calling about pensions is now illegal. If you receive an unwanted call from an unknown caller about your pension, get as much information you can and report it to the Information Commissioner’s Office.

The Pensions Advisory Service offers free and independent advice (see box left for details) and you can find a useful tool to trace lost pensions at Gov.uk/find-pension-contact-details

An independent financial adviser can also talk through your best options, understand your schemes in detail and spot ways of maximising contributions to gain tax relief.

In order to transfer a defined benefits pension with a value over £30,000, you must take advice from a financial adviser. Before contacting them, make sure they are registered with the Financial Conduct Authority.

“It’s such a small amount that I’ll take a lump sum once I’m 55”

Software engineer Alistair Stead, age 41, (pictured) did not start saving for a pension until he was auto-enrolled on his workplace pension in his mid-30s.

When he eventually left his job to become a chief technology officer at a larger company, he said it was unclear what would happen to his workplace pension.

“It took about four to six months for the paperwork to come. I automatically assumed the pension would just transfer. I thought there would be a simple form to fill in rather than me taking on the relationship with the pension provider.”

Alistair, from Market Harborough, in Leicestershire, eventually discovered that he had three options: transfer the pension to his new provider, extract the pension as a cash lump sum or leave it in the existing scheme. He says: “I left it. It’s such a small amount that it wouldn’t make a lot of difference to my new pension if I transferred it. At some point [after age 55], I’ll take the lump sum and use it for the house or the kids.”

“I missed the deadline to transfer my pension”

Hilary Scott (pictured) was caught out by time restrictions when she changed careers, which meant she couldn’t transfer one pension pot to another.

The 48-year-old from Northampton left her job on newspapers to become a university lecturer in her late 30s.

“I had a pension for about 13 years with my previous employer but I got really confused because I was also in a sharesave scheme and would get lots of letters about both the savings and the pension after I left. I had a huge pile of documents that I had intended to sort out once I’d settled into the new job.”

By the time Hilary realised that she needed to transfer her old pension into her new employer’s scheme, she had missed the deadline.

“It all got so complicated and I was getting different accounts from both pension schemes, which were arguing with each other about equalisation related to changes in pension ages for men and women.

Documents were getting mislaid at both ends and I was trying to sort it out on and off for two years. In the end, I gave up.

“I think it is so important that people pay attention to their pension from the moment they start working. But instead, we get caught up in more immediate financial worries like paying rent, mortgages, insurance and general monthly bills. Pensions feel like a long way off, so it’s easy to ignore them.

“I effectively have two pensions now: one that just sits there doing nothing and one that is active with my university job. What is even more galling is that the sharesave scheme, which I also put to one side, became completely worthless when my previous employer recently declared bankruptcy. I kick myself for not sorting it all out sooner.”

Further information

The Pensions Advisory Service Pensionsadvisoryservice.org.uk — 0800 011 3797

Financial Services register Register.fca.org.uk

Unbiased (for independent financial advisers in your area) Unbiased.co.uk— 0800 023 6868

LILY CANTER is a personal finance writer who writes for publications incuding The Daily Telegraph, The Guardian and The TImes

This article was originally published in our sister magazine Moneywise, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.